Thank the Cypriot parliament for averting euro-catastrophe

Proposal forcing residents to accept a tax on insured deposits would have triggered a chain reaction of bank runs across southern Europe

It can have surprised no one that members of the Cypriot parliament voted unanimously against plans to slap a tax on the islanders' bank deposits.

Members of parliament usually want to get re-elected. That means they don't want to find themselves in the position where they have to admit to voters "You know that 6.75 per cent tax you had to pay on the bank deposit you thought was guaranteed by our deposit insurance scheme? Yes, well, I'm afraid I voted for that tax."

{kind=link}

However, the plan's rejection now leaves the Cypriot government and the European authorities in a fiendishly difficult position entirely of their own making.

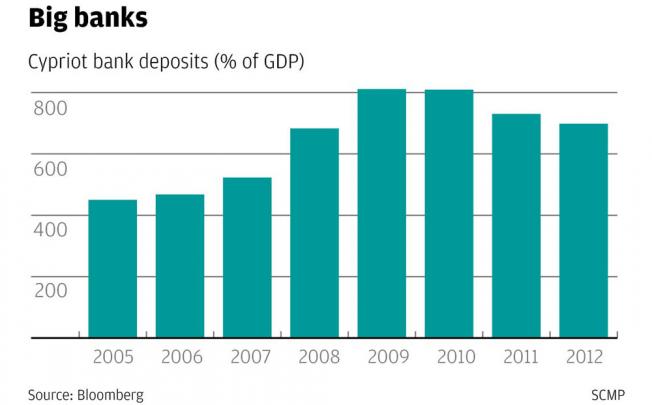

The problem for Cyprus is that its banks are enormous relative to its overall economy. As the chart shows, over the last few years the island has grown rapidly as an offshore banking sector, thanks largely to an influx of Russian money. As a result, at the end of last year, deposits in Cypriot banks stood at 700 per cent of the island's gross domestic product.

Unfortunately, the bankers of Cyprus took rather too much of that money and invested it in Greek government bonds. When Greece restructured its debt last year as part of its bailout deal, those bonds lost 70 per cent of their value, leaving Cyprus's banking sector insolvent. Rescuing the Cypriot economy in its turn will now cost around €17 billion (HK$170.6 billion), or 100 per cent of the local GDP.

However, ahead of their general election in September, German politicians are extremely anxious to avoid any accusations that German taxpayers are being forced to bail out Russian tax-dodgers. As a result, they are insisting that the euro zone's authorities should contribute no more than €10 billion to a rescue package.

The rest will have to come from a combination of austerity measures and the proposed €5.8 billion tax on bank deposits.

In theory, deposits worth less than €100,000 are insured. But raising the required €5.8 million solely from deposits of more than €100,000 would mean taxing them at a rate of more than 15 per cent.

That would incense the Russians and destroy Cyprus's offshore banking business, hence the government's ill-conceived plan also to tax the insured deposits of the local population.

That proposal has rightly been voted down. Now, however, assuming everyone wants Cyprus to remain in the euro zone, both the Cypriot government and the European authorities face a nasty dilemma.

Cyprus can hope to negotiate a bailout from the Russian government, perhaps in return for favoured access to gas deposits believed to lie off the Cypriot coast or other concessions.

But giving Russia's president Vladimir Putin such heavy leverage over a corner of the euro zone, especially one as geopolitically important as Cyprus, may well be more than European governments can easily swallow.

On the other hand, it would be politically damaging at home for Northern Europe's governments to extend Cyprus a more generous rescue package after already ruling one out.

Finally the Cypriot government could try and force a larger haircut on to big depositors. That could fatally injure its offshore banking sector, but with the banks now closed for the best part of a week, it is likely the damage has already been done anyway.

None of the choices are attractive. But hopefully, the one thing everyone now realises cannot be done is to force losses on the account-holders of insured deposits.

That would have triggered a devastating chain reaction of bank runs across the debt-laden economies of southern Europe as depositors lost all remaining faith in their local banking systems.

Happily, we have the electorally minded members of the Cypriot parliament for averting that catastrophe.