Perennially low interest rates a by-product of our modern age

Some blame the central banks, but most point to the fundamentals of modern times, and the impact of ageing demographics

There are many upsides to having been born in modern times. We live longer, get to drive cars and are less likely to end up burnt at the stake, or swallowed by a whale. Moreover, if we fall ill, the doctor won’t arrive at our bedsides and order a “bleeding.”

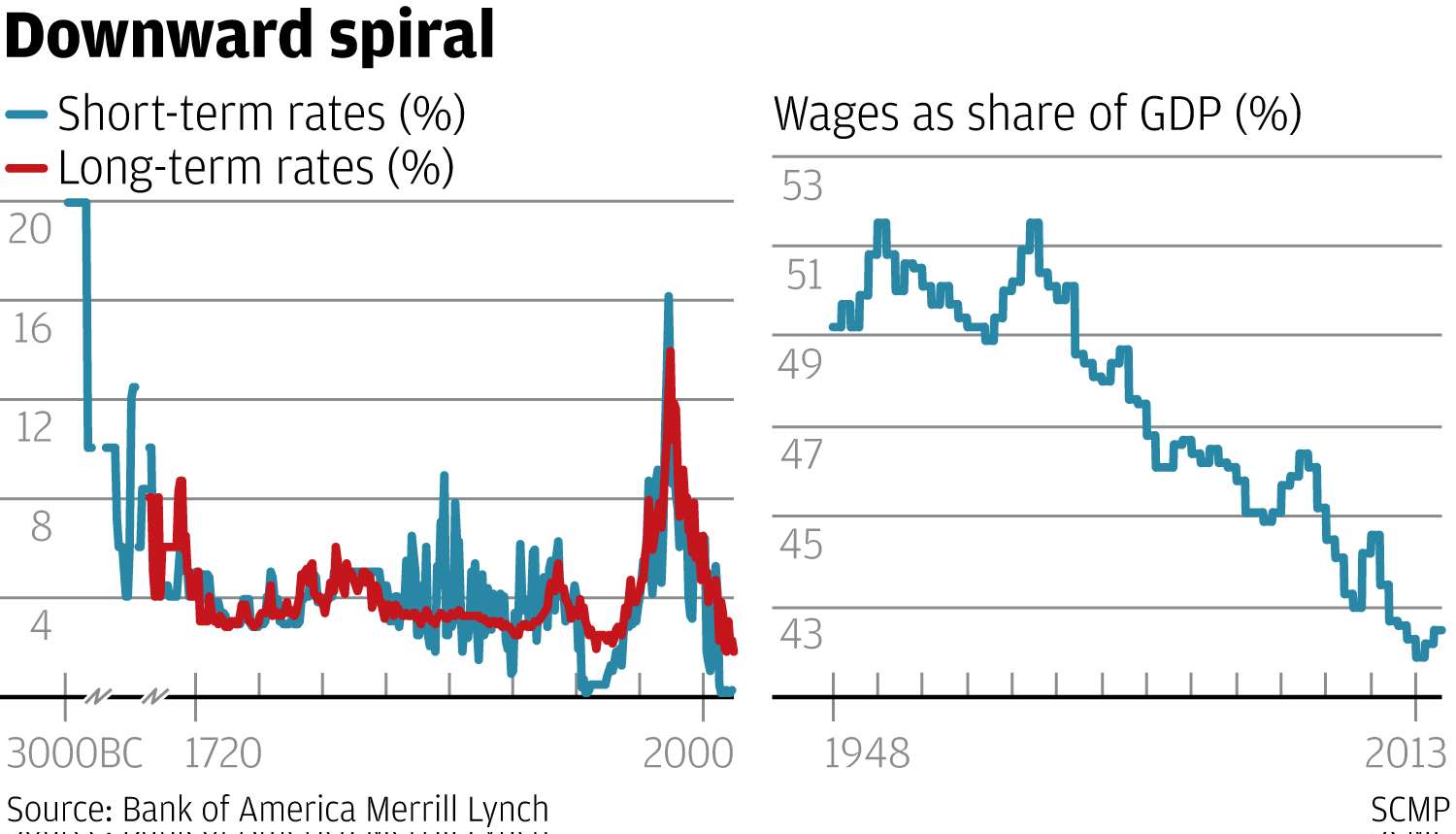

Then there is this: interest rates are the lowest they’ve been in five millennia, as pointed out in a recent Bank of America Merrill Lynch global investment report.

It is an “astonishing history investors are living through today: lowest interest rates in 5,000 years; lowest UK base rate since 1705; a negative Japanese bond yield for the first time since 1870,” BoA Merrill Lynch’s chief investment strategist, Michael Hartnett, wrote in the report.

It is astonishing to think about, but what does it mean? Is this an end-of-history event, or will interest rates revert to historical averages? This is the big question of our times, investment wise.

Unfortunately, it’s only because nobody wants to borrow money that interest rates are at their lowest in 5,000 years (based on estimates derived from ancient IOUs and Homer). Low rates are a reflection of global deflationary dynamics, and central banks are losing that battle.

Since the Lehman Brothers bankruptcy in 2008, there have been 654 policy rate cuts, by Hartnett’s count. Central banks have expanded their collective balance sheets to US$23.4 trillion and directly purchased US$12.3 trillion of bonds and other financial assets.

{kind=link}

Still, consumer prices are not rising much, if at all, and if prices aren’t rising there is no good reason to borrow money to invest. Some blame the central banks, but most point to the fundamentals of modern times.

For starters, technology tends to be disruptive and deflationary. Everything from robots to just-in-time software to online retail has increased the efficiency of making and delivering goods, thus lowering their prices.

Then there is ageing demographics. The size of the working population is a key component of economic growth but in some countries, like Japan, the population is shrinking. Plus the young tend to spend, and the old save. The final opponent in the war on deflation is high debt levels, which makes it dangerous to borrow more. This helps explain Europe’s stagnation, but China’s deleveraging is the biggest worry, because that country’s debt-fuelled rapid economic growth has been a major wind at the back of the world economy for the past 20 years.

These three Ds – demographics, deleveraging and disruption – would indicate that interest rates would hover near zero for quite a while. This in turn boosts the amount of money investors are willing to put into certain stocks – thus Wall Street’s second longest bull market in its history. Meanwhile, an estimated US$9.9 trillion worth of bonds are yielding less than zero.

If central bankers cannot win the ‘War on Deflation,’ there is something else that could potentially change the picture: and that is voters

If central bankers cannot win the “War on Deflation,” there is something else that could potentially change the picture: and that is voters.

“Wall Street has boomed; but Main Street has not,” says Hartnett. The wealthy are the biggest gainers in cheap-money-fuelled asset inflation, and meanwhile wages continue to fall as a percentage of gross domestic product.

As a result, voters are “unsurprisingly” pushing for policies to address wage deflation, from big hikes in minimum wages to blocks on imports or bars on immigration.

Wary of increasing redistribution or protectionism, some countries may respond to the political pressure with the “helicopter money” option – in which central banks print even more money, but instead of buying bonds as per usual, they directly transfer these funds to everyday citizens.

The last great “inflection point” on bond yields was in 1981 – in this case they began to fall after a prolonged period of high inflation. The consequential adjustments in asset prices was monumental.

At this stage, few investors are betting on the defeat of deflation. But Hartnett recommends watching electoral and political developments, because radical policy change is not outside the realm of possibility.

Typical “inflation” plays such as commodities, emerging market equities, inflation-protection bonds like TIPS and bank stocks could soar in such an event. Contrarians should go long these assets while shorting “deflation” plays – i.e. bonds but also US stocks, the world’s bubbliest.

Cathy Holcombe is a Hong Kong-based financial writer