Are we about to see the endgame of the super-stimulus cycle?

Investors should brace for a big shock if central banks hit the monetary brakes, interrupting markets that have become reliant on cheap and easy cash

There’s a definite hint of hesitation in the air and it is bad news for markets bulled up on the belief that the central banks’ super-stimulus will be an everlasting free-for-all. For global investors accustomed to a non-stop flow of cheap and easy cash there is a big shock waiting round the corner. This monetary manna could soon be drying to a trickle, leaving financial market confidence high and dry.

Markets like certainty and a clear vision of what the future holds. The problem is there is too much monetary murk out there right now. The US Federal Reserve has been on the cusp of tougher monetary policy for ages and it is still unclear whether it has the nerve to move again later this month when its interest rate-setting committee next meets. The vacillation is weighing on investors’ minds and boosting market volatility.

This monetary manna could soon be drying to a trickle, leaving financial market confidence high and dry

It is not just the Fed. The Bank of Japan seem to be casting doubts about the prospect of further easing, while the Bank of England is being roundly criticised for over-reaction after its post-Brexit stimulus measures. Perhaps the biggest worry of all is the European Central Bank may be getting cold feet at the prospect of additional easing measures after its quantitive easing bond buying programme expires in March 2017.

This could become a major problem for markets. The ECB were late into the easing game after the 2008 crash and have been expected to pick up the baton for super stimulus once the Fed’s monetary contribution to global growth begins to fade. Last week’s ECB policy meeting clearly disappointed investors hoping for some clues that future easing plans will remain open-ended beyond the ECB’s current 1.74 trillion euro QE programme.

{kind=link}

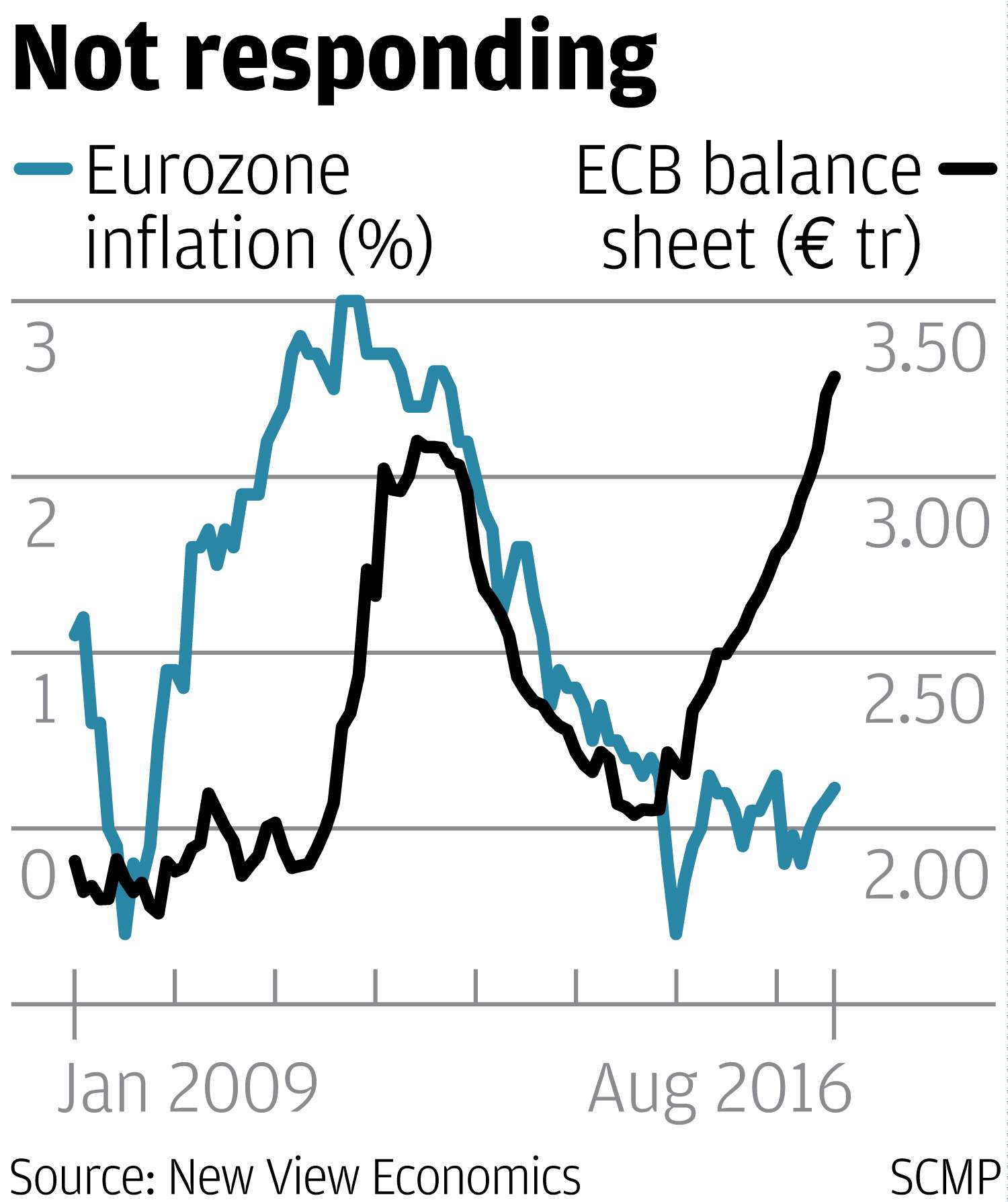

To date, the ECB has bought over 1 trillion euros of bonds but there seems little to show for it. Euro zone economic growth and inflation remain just as anaemic with little prospect of picking up over the foreseeable future. If anything, downside risks to growth seem to be picking up, not diminishing, despite the wall of ECB money thrown at the economy, currently equivalent to about 10 per cent of euro zone GDP.

Euro zone growth potential remains extremely soggy. Weak global demand, faltering consumer and business confidence and signs that Germany’s economy, the euro area’s main workhorse, is starting to stall, are not helping matters. July’s sharp 2.6 per cent contraction in German exports, the steepest monthly drop in a year, is adding to growth concerns and raising the spectre of a crash landing at some stage soon.

The chances of the euro zone hitting official GDP growth forecasts of around 1.5 per cent over the next two years look very slender. Despite negative interest rates and the flood of QE money, all the ECB have achieved is “pop-up” growth, worth no more than 0.3 per cent over the last quarter. The euro zone economy has been so badly compromised by high unemployment, deep austerity and dire debt deflation that super-stimulus is having little effect.

{kind=link}

The ECB is fast running out of options. Without negative interest rates and QE, the euro zone would quickly revert to recession and the risk of a deeper financial crash. But stronger policy initiatives are desperately needed to beef up the recovery momentum. The trouble is that Germany’s inflation-phobic Bundesbank would dearly love to turn the stimulus taps off sooner rather than later to block future price pressures breaking out.

With the Bundesbank standing in the way, it looks like the ECB will be limited to tinkering at the monetary margins. The ECB clearly needs to dilute its asset purchase rules given the available pool of euro zone government bonds is drying up fast, but the economic impact is only likely to be marginal. Europe needs a much bigger policy blockbuster to jump-start faster recovery.

The market is well aware the clock is ticking. When the ECB’s current QE programme runs out next March it will be High Noon for global markets. At the very least the ECB needs to get its skates on and provide the markets some hope that the QE money-go-round will keep turning until sustainable growth is in the bag.

There is a lot at stake. World financial markets can ill afford to lose another QE net benefactor. With global stock and bond valuations already looking well over-extended, this time there will be nowhere to run and hide when the central banks’ cash machine finally runs out.

David Brown is chief executive of New View Economics