HSBC’s new compliance rules require clients to provide more account information

Increased information disclosure is part of bank’s rigorous compliance plan to meet enhanced anti-money-laundering requirements in the US and Europe

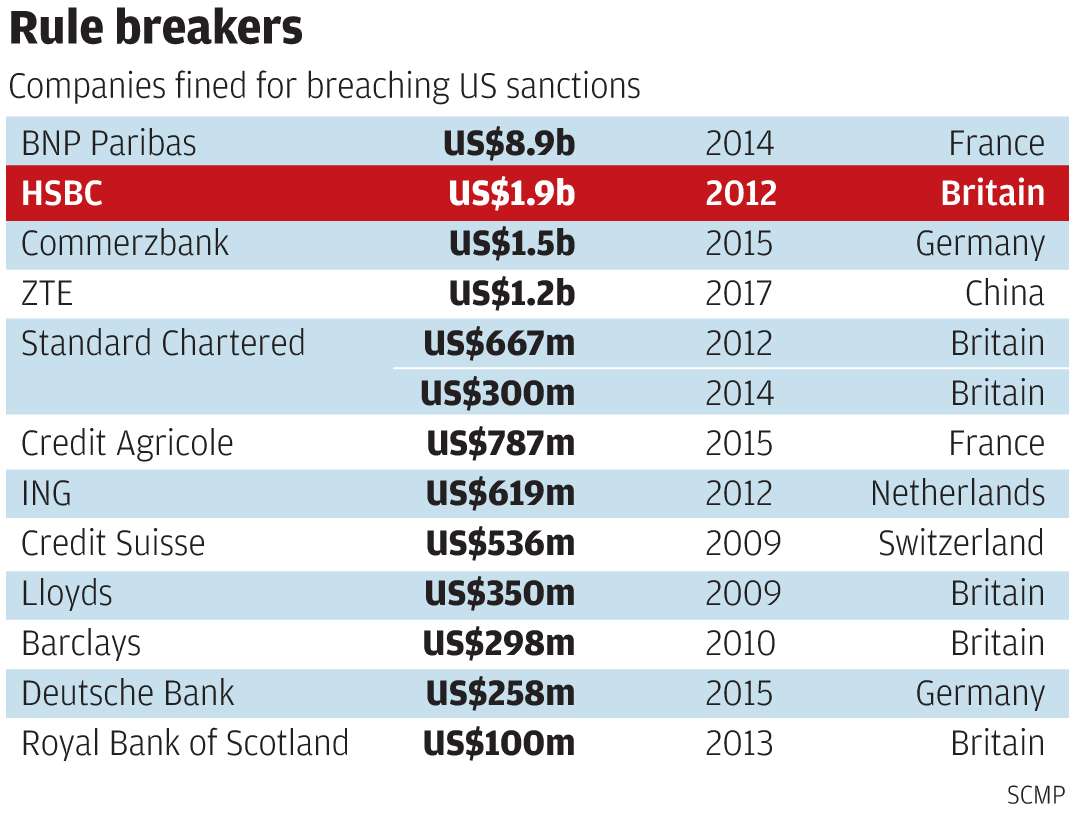

HSBC Holdings is stepping up its compliance procedures this year to meet higher global standards as part of the deferred prosecution agreement with the US Department of Justice following the bank’s US$1.9 billion penalty in 2012 for breaching American money-laundering rules.

Effective immediately, retail customers must disclose how their accounts are used, in addition to providing their address, contact details, employment and income history, to qualify for an HSBC account. Corporate clients must provide information with supporting documents on the nature of their business, ownership data, the jurisdiction of their operations, source of funding and the purpose of the account, said the bank’s Hong Kong chief executive Diana Cesar.

“It’s going to be a frustrating exercise,” Cesar said. “We understand how frustrating the requests for information from banks can be, particularly for longstanding customers, and we sincerely apologise for the inconvenience they cause, but this information is essential to enabling us to detect those who are trying to abuse the financial system.”

Global banks from HSBC to Standard Chartered have been stepping up their financial controls to comply with US and European regulations to prevent money laundering and terrorist financing and enforce financial sanctions against rogue nations.

“Criminals involved in drug trafficking and terrorism use the banking system to transfer about US$800 billion to US$2 trillion every year globally,” Cesar said. “We need to have up-to-date client information to crack down on these money-laundering activities.”