Analysis | What’s really driving Evergrande’s ever-surging share price?

Analysis: Chairman Hui Ka-yan holds 77.79pc of its stock, but who’s after the rest, and what’s the company’s genuine worth?

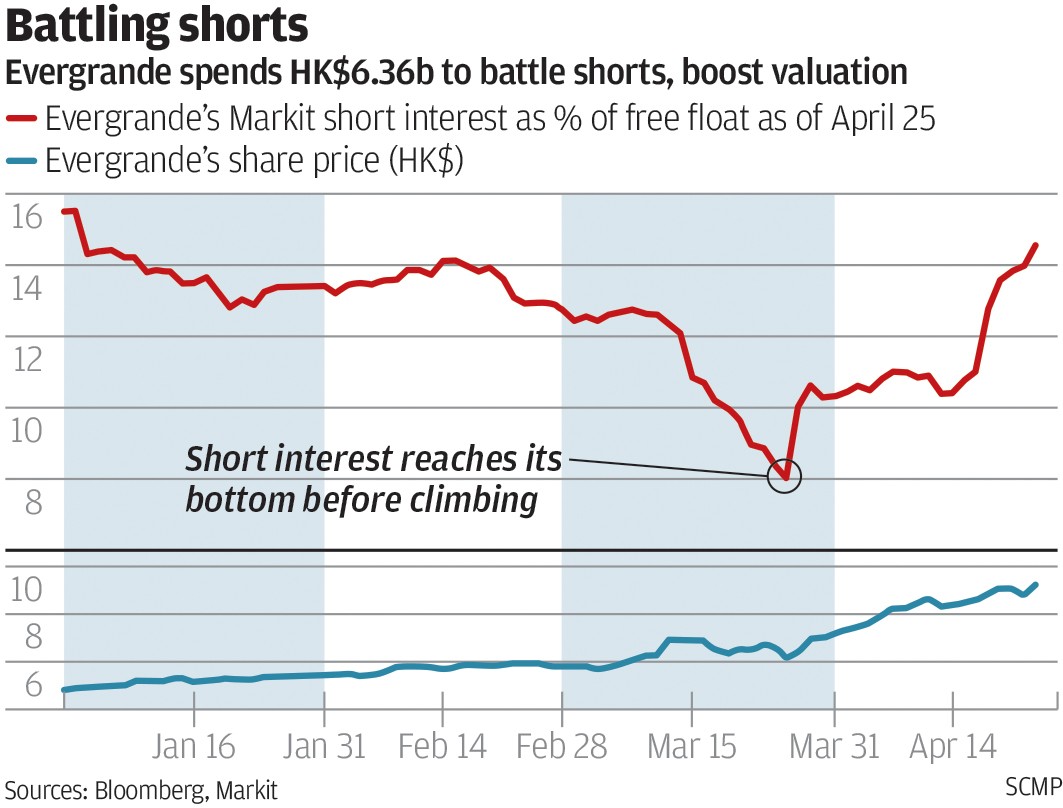

China’s most indebted property developer has given its bearish investors a strong slap in the face.

The surge can be attributed to multiple factors, but chairman Hui Ka-yan’s ambition to defeat short-sellers, tapping his Hong Kong tycoon friends to pave the way for its planned listing on the mainland, is undoubtedly the key driver behind the dramatic rises.

On Monday, the developer’s shares shot up an astonishing 23 per cent, even after rallying the previous eight consecutive trading days.

By the close of play on May 29, its market value had reached almost HK$200 billion (US$25.66 billion), trading at a record 36 times historical earnings to become the most expensive property stock on the Hong Kong market.

[Evergrande chairman] Hui and some of his friends are just trying to fry up the share price, and push for a better valuation before an IPO

“Hui and some of his friends are just trying to fry up the share price, and push for a better valuation before an IPO,” said Philip Tse, property analyst at Bocom International.

In April, Evergrande splashed out HK$6.3 billion on 5.3 per cent of its shares, a move which has since sent its price up 50 per cent in under a month.

The chairman now controls 77.79 per cent of the company shares, and Evergrande’s public float has dropped to 22.21 per cent, right on its minimum limit.

“Hui has 300 billion yuan cash on hand, [although he can’t repurchase more shares], he can find other ways to boost Evergrande’s price, ” said Toni Ho, a property analyst at RHB-OSK Securities.

Analysts believe the remaining shares are partly controlled by some of Hui’s closest Hong Kong-based circle of wealthy friends, and the real public float could be far less than the number on the book, which means when short sellers are forced to liquidate their positions, stock prices could see a significant rise in a short term, because of a lack of liquidity.

Most notably, Chinese Estates, a company controlled by Hong Kong billionaire Joseph Lau Luen-hung’s wife Chan Hoi-wan, has been actively trading in Evergrande since mid-May, through its Fair Eagle Securities.

Lau, the Hong Kong billionaire is well-known for his close relationship with Hui and also a debtor of Evergrande.

On May 26 alone, it bought another 26 million shares, building its stake in Evergrande to 0.22 per cent from 0.02 per cent, according to the disclosure from the Hong Kong stock exchange.

Despite its standing now as China’s largest homebuilder, it hasn’t always been smooth sailing for Evergrande, however.

Its shares have long been traded at as low as 3 to 5 times P/E ratio in Hong Kong after debuting in 2009 as investors worried over its heavy debt burden, making it a prime target for short sellers.

Its total borrowings surged 80 per cent by the end of 2016 on year to 535 billion yuan.

The real turning point came in March after Hui vowed to start deleveraging, and he has since repaid half of its outstanding high-interest perpetual bonds.

A number of top investment banks, including Morgan Stanley and Citi, subsequently raised their target price for the stock this month.

A fortnight ago, S&P surprised many by upgraded its long-term corporate credit rating on Evergrande to B from B-, citing its improved liquidity and strong sales.

“Evergrande’s balance sheet is improving, as well as its profit forecast,” said Liu Feifan, a property analyst at Guotai Junan International.

Its share price, say analysts, has also been driven up by investors speculating on the price gap between Evergrande’s Hong Kong shares and the expected valuation of its Shenzhen listing, and opinion is still divided on the company’s accurate current valuation.

“Definitely like the Goldin or Hanergy bubble, its valuation is not sustainable,” Tse said.

A 30 billion yuan first-round of pre-IPO financing in January gave Evergrande’s property assets a market value of nearly 230 billion yuan – double its valuation in Hong Kong at the time.