Remember what's at stake in China's reform debate

To achieve sustainable growth, Beijing needs to rein in investment and encourage consumption despite resistance from corporates and banks

In recent weeks, the volume of commentary about the mainland's economic reform has reached a fevered pitch.

Given the lack of clinching proof either way, the debate can get a little theoretical. Sometimes, it is so blinkered it is almost reminiscent of medieval European philosophers arguing about how many angels can dance on the head of a pin.

So in the interests of perspective, it is worth taking a step back and reminding ourselves just why economic and financial reform is regarded as so important and what is at stake any way.

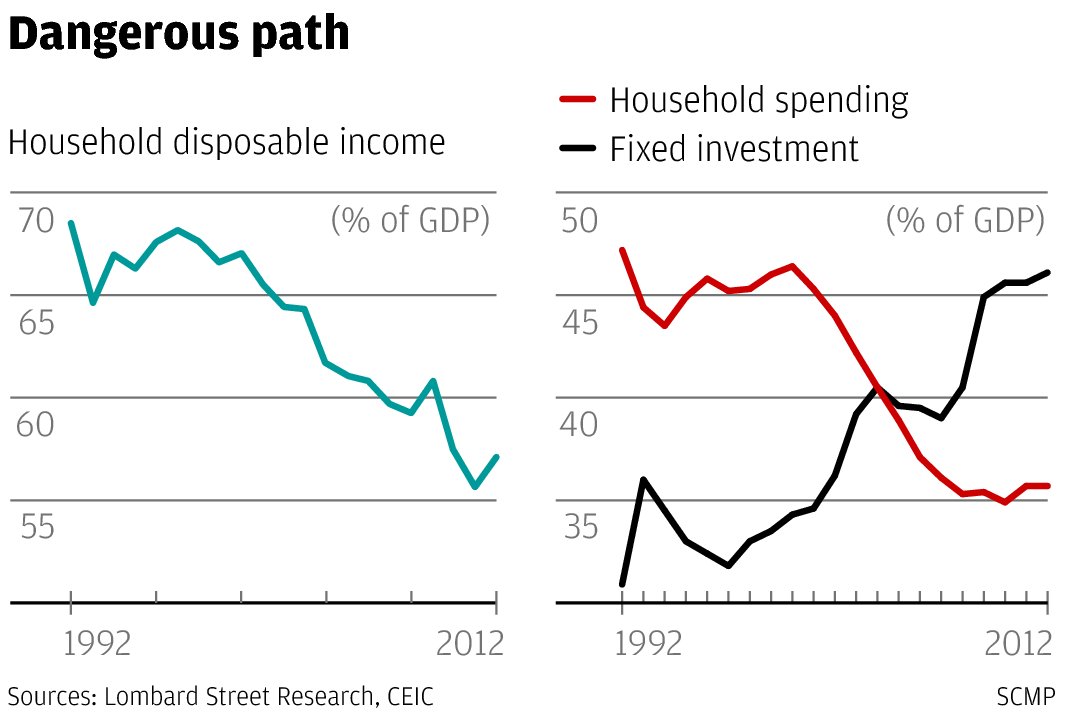

Over the past couple of decades, the economic path the mainland has followed has been broadly the same as Japan's during its high-growth phase of the 1960s.

The government has relied on high domestic savings rates to fund an investment-led model, retaining control of the domestic financial system to keep interest rates low and direct cheap capital to favoured sectors of the economy.