Closures of China's iron ore mines won't offset global supply increases

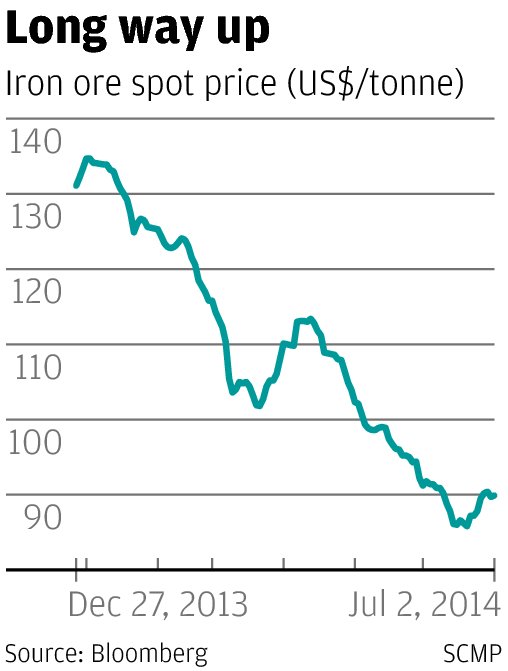

Iron ore prices increased the most in 10 months last week, but hopes that this marks the start of a new bullish phase are likely to be dashed.

Iron ore prices increased the most in 10 months last week, but hopes that this marks the start of a new bullish phase are likely to be dashed.

Spot Asian iron ore ended last week up 3 per cent from the prior week, with prices bolstered by an improvement in China's manufacturing outlook after the June HSBC flash Purchasing Managers' Index, which showed expansion for the first time in six months.

Iron ore prices are still down 30 per cent from the end of last year, but they have recovered since briefly dropping to a 21-month low last month.

This view is bolstered by the improving outlook for steel demand on the back of faster investment in railway and other infrastructure spending as the authorities undertake what has been characterised by several analysts as a "mini-stimulus".

Domestic output accounted for about 30 per cent of last year's iron ore demand in the world's largest consumer of the steel-making ingredient, equivalent to about 350 million tonnes of 62 per cent iron ore, the global benchmark. According to a Morgan Stanley research report on June 12, about 46 per cent of this is produced at state-owned mines and the rest at private operations.

State-owned mines are likely to continue producing even as prices fall, given that they are more focused on jobs than profits and many are integrated with steel mills, the report said.

However, private mines will idle some output, with Morgan Stanley estimating 64 million tonnes of 62 per cent iron ore equivalent could leave the market this year. But this still will not be enough to offset increases in supply, with the report saying an extra 111 million tonnes will be added this year to seaborne supplies by the big four global miners - Vale, Rio Tinto, BHP Billiton and Fortescue Metals.

Also, since private mines on the mainland have a weighted average cost of about US$101 a tonne, they will return to full production if the price rises significantly above that level. This implies that the spot price should remained anchored around this level for the medium term, as a fall below knocks out some Chinese output but a rise above brings it back.