Crude clings to US$40s, eyeing Fed lift-off, Opec let-down

International Energy Agency expects global consumption growth to slow next year

November might as well have not happened for the oil markets.

Aside from NYMEX crude briefly slipping below the US$40/barrel mark on burgeoning US stockpiles, and some upticks towards the end of the month amid rising geopolitical tensions from the war against Islamic State, Brent and WTI were mostly locked in languid sideways movements through November.

Continuing oversupply and fears of eroding demand growth in the coming year kept a firm lid on prices, also limiting the geopolitical premium.

All eyes were turned toward a few major events in December: expectations of an interest rate hike at the US Federal Reserve meeting from December 15 to 16; Opec ministers meeting in Vienna on December 4 to agree to do nothing about the global supply glut; and the climate change talks in Paris from November 30 to December 11, which could have longer term implications for fossil fuels.

Venezuela, striving again to have its voice heard ahead of the Opec meeting, warned of oil dropping to the low US$20s/barrel if the producers’ group didn’t act. Oil minister Eulogio del Pino suggested Opec aim for US$88/barrel “equilibrium price”, which would imply a hefty – and equally unlikely – production cut.

Iranian oil minister Bijan Zanganeh reiterated his country’s determination to raise exports

Saudi oil minister and Opec kingpin Ali Naimi responded with platitudes about the kingdom’s willingness to “cooperate” with producers to “maintain market and price stability”, which failed to dent consensus expectations for Opec to stay the course.

What was decidedly changing through the weeks was the US dollar’s strength, as the market priced in a US rate increase, which lent further downward pressure to oil prices. The US dollar index was flirting with 100 as November drew to a close, targeting peaks last seen in March.

Meanwhile, rising oil stocks in the United States and elsewhere in the OECD countries continued serving as a reminder of the twin themes of persistent supply glut and weakening global demand growth.

The International Energy Agency’s figure of a record high 3 billion barrels in OECD inventories as of September end was bandied about a fair bit, and will no doubt be seen as a comfortable cushion against any major geopolitical shocks. The figure is up 10 per cent or 279 million barrels from a year ago.

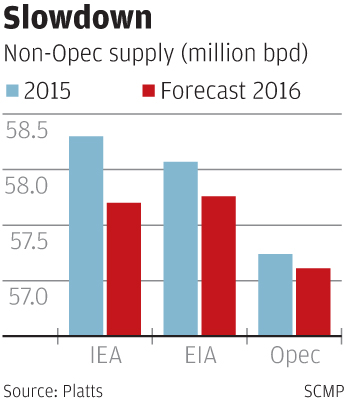

The stockbuild is expected to slow down next year, with non-Opec supply projected to shrink by more than 600,000 b/d. The US Energy Information Administration expects domestic crude production to average 8.77 million b/d in 2016, down from 9.29 million b/d this year. The question is whether the drop will be enough in the face of ever rising Opec supplies, especially as Iran reaches its full potential post-sanctions.

{kind=link}

Iranian oil minister Bijan Zanganeh reiterated his country’s determination to raise exports by 500,000 b/d at the earliest possible opportunity even if fellow Opec members did not make space for the new barrels.

On the demand side of the equation, IEA as of November expected global consumption growth to slow down to 1.2 million b/d in 2016 after hitting a five-year high of 1.82 million b/d this year.

Easing demand growth as more emerging market economies face headwinds seems to be a given, though there are dissenters. Forecasters are underestimating demand growth, which could hit 2 million b/d next year, thanks to price elasticity, Barclays asserted in a white paper published on November 18. The bank expects stocks to draw down next year and crude to average US$60/barrel.

Sixty dollars a barrel is where a lot of US producers would have liked to hedge their 2016 production. But with lingering depression in oil prices and the forward curve not rising to US$50 until 2017, some companies are said to have decided to jump in to add to their protection after their third-quarter updates.

The oil markets are taking it all in, from the imminent ponderable of incremental Iranian supplies, to the longer-term imponderable of the impact of a likely new global climate deal in Paris. That agreement, while not moving markets in itself, is expected to lead to a gradual decline in the use of fossil fuels either because of carbon pricing policies or direct regulation of emissions, creating “stranded assets” under the round – hydrocarbons that companies may never be able to tap.

But the oil markets will think about that tomorrow.

Entering the final month of a turbulent 2015, the focus was more on pricing in geopolitics than decarbonisation, as the US-led coalition launched “Operation Tidal Wave II”, a campaign of air-strikes against oil fields and associated infrastructure in Syria in a bid to cripple Islamic State’s main source of revenue.

Syria is not a major crude producer; its output is said to have dropped below 50,000 b/d since Islamic State advanced into the country. The risk oil needs to price in from escalating tensions around Islamic State, marked by events such as the terrorist attacks in Paris and the downing of a Russian military plane by Turkey, is the outbreak of a wider conflict in the region.

It looks like we will end the year weighing the fear premium of Tidal Wave II against the discount of an oncoming “Oil Flood II”.

Vandana Hari is Asia editorial director at Platts