Canada faces a currency conundrum

Canada's central bank may want to kick-start its tightening cycle to fine-tune growth and inflation, but a stronger dollar could upset its plans

Canada's recovery is picking up steam and inflation is creeping higher. In reality, the country should be steeling itself for higher interest rates ahead.

That is not what the Bank of Canada has in mind. Interest rates are sitting squarely in a neutral position for the foreseeable future. The central bank is perched on the fence and it wants the market to think a rise in rates is just as likely as a cut.

The bank wants faster growth. Keeping interest rates at super-accommodative levels since 2008 has been the centrepiece of its strategy. It has helped to shore up the housing market, boosted consumer demand and saved the country from deeper recession since the financial crash.

Now the bank is looking to the Canadian dollar (known affectionately in the market as the "loonie") to help take the recovery to a higher level through faster export-led growth. This means keeping the loonie competitive in the foreign exchange markets.

{kind=link}

The bank switching to higher interest rates in the near term would be a bad idea. Raising interest rates would be like waving a red flag to Canadian dollar bulls.

Under former governor Mark Carney, now head of the British central bank, the Bank of Canada cut rates to record lows, down to 0.25 per cent, to beat the financial crash. It also pumped in unprecedented amounts of liquidity into the financial system to stabilise the banking system.

Boosted by its massive energy and mineral resources and spurred on by the super-charged monetary policy, Canada subsequently only suffered a short and shallow recession. It was spared the deeper downturn that blighted its Group of Seven partners.

Now there is a risk that the strategy could backfire. Super-easy money policy, combined with a soft currency approach, could stoke up latent demand pressures and provoke a bigger inflation backlash in the process.

The bank wants faster growth. But there is a good chance that Canada's recovery will come through quicker than the bank is bargaining for, thanks to a faster turnaround in the United States economy.

Higher interest rates in the near term would be ... like waving a red flag to Canadian dollar bulls

US Federal Reserve chairman Janet Yellen is keeping her foot pressed down hard on the monetary accelerator. She would rather risk higher inflation than risk falling short on delivering sustainable recovery. The Fed is reluctant to see five years of zero interest rates and extreme money creation to go to waste.

Despite the winter slowdown - affecting both the US and Canada - the signs are the US economy is springing back hard. Employment conditions are improving dramatically. Recent payrolls data showed 273,000 jobs added in the past month alone. The unemployment rate sank to 6.3 per cent, the lowest rate since September 2008.

With Canada's economy so closely aligned to economic fortunes in the US, Canada's growth rate could easily be pumped above 3 per cent by next year - triggering higher demand-pull and cost-push inflation pressures in the process.

The Bank of Canada's anxieties about the risk of disinflation are misplaced. Headline inflation at 1.5 per cent is below its 2 per cent preferred target but the trend is pointing higher. Energy and raw material prices are picking up, a precursor to pipeline cost pressures ahead. Faster growth in the economy will see wage demands increasing at the same time.

Keeping a lid on future inflation risks, while trying to fine-tune export-led recovery with a competitive currency, are mutually exclusive objectives. Stronger growth, rising inflation and tougher rate policy will be seen by the markets as a forerunner to a stronger loonie.

The bank has already had two abortive attempts to tighten policy in the past few years. In 2010, it was the first G7 nation to tighten policy, raising the overnight rate from 0.25 per cent to 1 per cent as growth surged to 3.5 per cent as the economy bounced back from recession. The bank was stopped in its tracks by the surging loonie.

In October last year, governor Stephen Poloz shifted the bank's policy stance back into neutral after 18 months of signalling that rate increases were on the horizon. Keeping the currency competitive was the motive. The loonie started the year as many traders' favourite short trade as the central bank was expected to stay dovish.

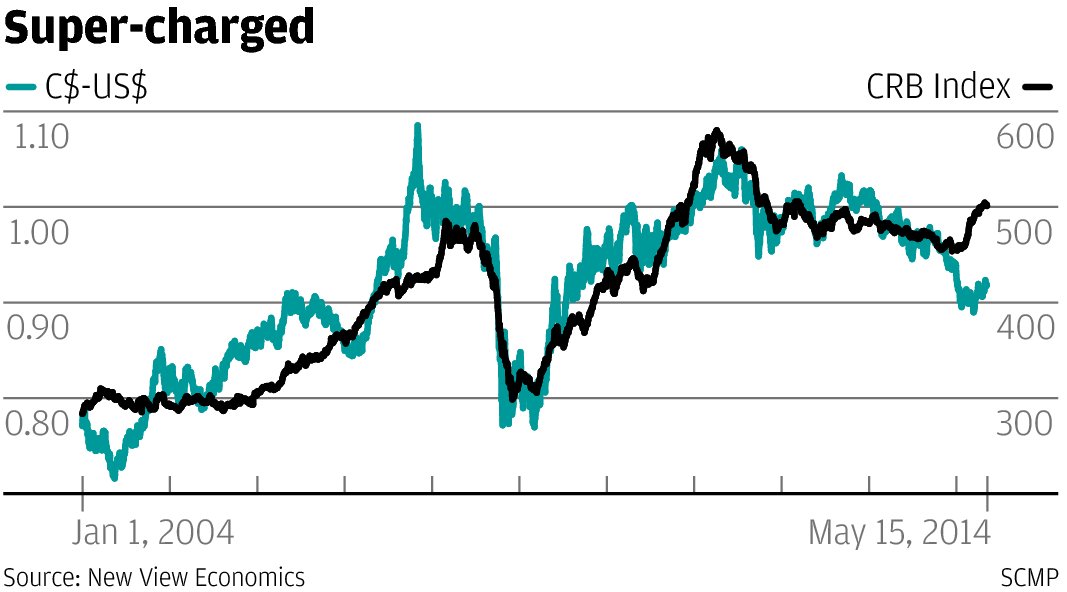

This is now being turned on its head. With the markets taking a more constructive view about US and global growth prospects, world commodity prices are perking up. Given the perception of the Canadian dollar as a commodity-based currency, demand for the loonie is bound to recover.

The bank could find itself between a rock and a hard place very soon. It might want to kick-start its tightening cycle to fine-tune growth and inflation pressures, but a stronger loonie could block the way. Once US rates begin to rise, it may be too late. Canadian rates will be left stuck in the starting blocks.