PBOC's reserve requirement move a way of manipulating yuan exchange rate

TThe purpose of this move, we are told, was to release an estimated 600 billion yuan (HK$754 billion) of liquidity into the economy so as to get things moving again at a time of slowdown.

TThe purpose of this move, we are told, was to release an estimated 600 billion yuan (HK$754 billion) of liquidity into the economy so as to get things moving again at a time of slowdown.

In order for this to happen, however, this 600 billion yuan would first have to be kept out of the economy, locked away cold in central-bank vaults. Only then could putting it back into the economy actually increase the stock of money in the economy.

But if, instead, let's say, the PBOC had all along used the required reserves it extracts from the banks to buy the US dollars flooding in as a result of a big trade surplus, then the money would not be sitting cold in its vaults at all. It would already be out at work in the economy.

In that case this stimulus measure would have little if any effect. Instead of taking yuan from the banks to pay US dollar sellers who would then deposit the yuan back with banks, the PBOC would not take the yuan from the banks in the first place. Result: No net increase in the stock of yuan and no real stimulus.

And guess what? It is this second scenario that describes the state of play in the mainland.

The simple fact of the matter is that the PBOC uses the required reserve ratio not as a tool for controlling the stock of yuan in the monetary system but as a way of manipulating the yuan's foreign-exchange rate.

{kind=link}

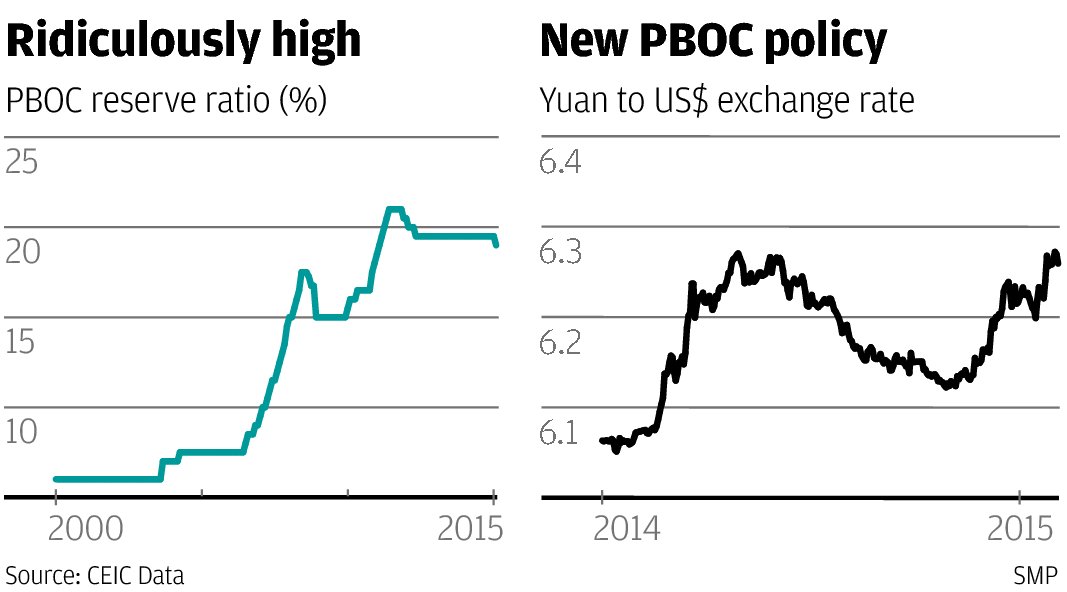

As the first chart shows, this has meant that the PBOC has raised the reserve ratio all the way from 6 per cent in 2000 to as high as 21 per cent four years ago to soak up continuous big inflows of foreign exchange and, in the process, build up foreign reserves from US$156 billion to a recent peak of US$3,993 billion.

The figure has now come down a little. The PBOC diversified a portion of these assets into other currencies and the US dollar then took off against these currencies. Smart move. It happens to people who think they are cleverer than the market.

But the PBOC has tired of the game for other reasons, including that it has long been the loser on the income and capital-gain side of this equation while few other monetary authorities use reserve requirements any longer and none maintain them at such ridiculously high levels.

Thus it now wishes to constrain capital inflows and even reverse them into capital outflows in order to balance out the record inflow of foreign-currency trade receipts coming across the borders.

And one good way of doing this is to make the yuan less attractive to investors, which is what I think lies behind the recent yuan weakness. Expect more of it for a while.