Weaker China March trade surplus a blip in long-term trend

The prevailing wisdom is that China’s economic growth is no longer supported by trade.

Taking a look at long term charts to see if the contribution of trade to GDP has gone down is the only sensible way to assess this, especially when analysing an emerging economy. The picture is rarely evident in month-to-month changes.

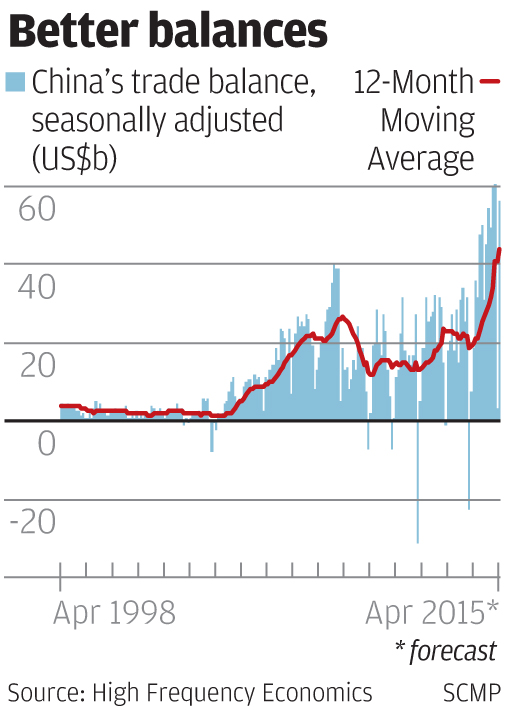

This approach means you can ignore the itsy-bitsy-teeny-weeny trade surplus booked in March - a mere US$3.1 billion (HK$24.2 billion) - as a crazy deviation from a very strong trend. It is pretty certain that the trend is unbroken by this one-off report.

If there was reason to get excited because the trade surplus in March was US$37 billion below its 12-month moving average, shouldn’t there also have been excitement when the February surplus was US$19.6 billion above trend, or when the January surplus was US$26 billion above, or when the December surplus was US$17.9 billion above?

When looking at China’s trade trends, the smallest increment of time that matters is a full calendar quarter. The trade surplus in Q1 was US$123.7 billion, the third biggest ever. The biggest ever trade surplus was in Q4 last year, at US$149.5 billion. And the second biggest ever was in Q3 last year, at US$128.1 billion.

Indeed the trade surplus has been growing faster than GDP. In yuan terms, the trade surplus has increased 16-fold since 2000, while GDP has increased just 3-1/2 times. Since the 2008-09 global economic crisis, the trade surplus has increased 2-1/2 times while GDP has grown barely by half. The trade surplus is increasing as a share of GDP. Therefore trade is adding to GDP growth.

Some people wonder if gross export growth is dragging down GDP. It is true - gross export growth is not what it used to be a decade ago. Of course import for assembly and re-export has become a much smaller part of China’s economy and that explains a lot of the drop in gross trade. In any case, gross exports through March - including the big year-over-year drop in March - were just under 9 per cent higher than a year ago on trend. How can that be holding back an economy growing 7 per cent year-on-year?

So what happened in March? Well the pattern over the last dozen years - at least - has been that exports in February always turn out further below the recent trend than any other month of the year.

This year exports did not dip in February. It seems to have happened in March instead. It is not clear why this happened. It is perplexing, but it is still just a blip.

There is no reason yet to make adjustments to forecasts for trade or to the view that trade is ripping along quite briskly and is supporting GDP growth. Our estimate for the April trade surplus is 349 billion yuan (HK$435.7 billion). That is roughly triple the April surplus last year and in 2013. If that forecast is right, it will be the biggest April trade surplus ever and the third biggest trade surplus in any month ever after January and February’s back-to-back record results.

And prospects for trade boosting China’s economy can only rise. China’s project to build trade routes linking its 1.4 billion consumers with the euro zone’s 335 million high income individuals, by way of Central Asia, will link the economies by land - rail and truck - by air and also by sea via a separate maritime route from Fuzhou to Piraeus.

The sea route touches Indonesia, East Africa and the Persian Gulf. Altogether, the Silk Road will connect roughly four billion emerging market consumers to China and Europe. The whole thing will be built with capital goods and technology exported by China.

History has shown that control of trade routes is the key to economic and geopolitical power. China’s Silk Road initiative can give it dominant influence over the part of the world where economies will grow the most over the next century, while the decline of the present G7 economies relative to the rest of the world continues unabated.

Carl Weinberg is chief economist at High Frequency Economics