Forget the statements, China’s capital outflow is still enormous

The State Administration of Foreign Exchange says China’s capital outflow has ‘moderated a lot’, but calculating it the technical way shows a far different story

A statement from the State Administration of Foreign Exchange (SAFE) blamed seasonal factors for the larger than expected fall [in foreign reserves], including forex purchases for overseas travel and bond repayments.

“China’s capital outflow has moderated a lot and it will move towards a balance in the future,” it said. “The current reserves are adequate.”

SCMP, February 8

I shall accept that bit about the reserves being adequate but it doesn’t really mean much any longer. Adequacy of foreign reserves is an outdated concept from the days of the gold standard when countries worried themselves about how many months of imports they could pay for with their reserves if their export earnings collapsed.

The remedy these days is floating exchange rates and foreign borrowings. This is one of those rare instances in which human thinking has actually progressed. To put it in perspective, the United States, with a US$19 trillion economy, has foreign reserves of only US$117 billion while China, with a US$11 trillion economy has reserves of almost US$3 trillion, about 45 times as much relative to economic size and by far the world’s largest reserve hoard.

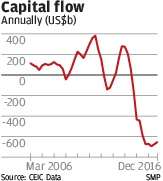

Yet it is China that obsesses about the adequacy of foreign reserves. You never hear of it in the US. But what is not true in the SAFE statement, is that China’s capital outflow has moderated. The chart sets out the facts. Capital outflow at the end of 2016 was still running at US$653 billion a year, only slightly less than a running figure of US$673 billion at the end of September.