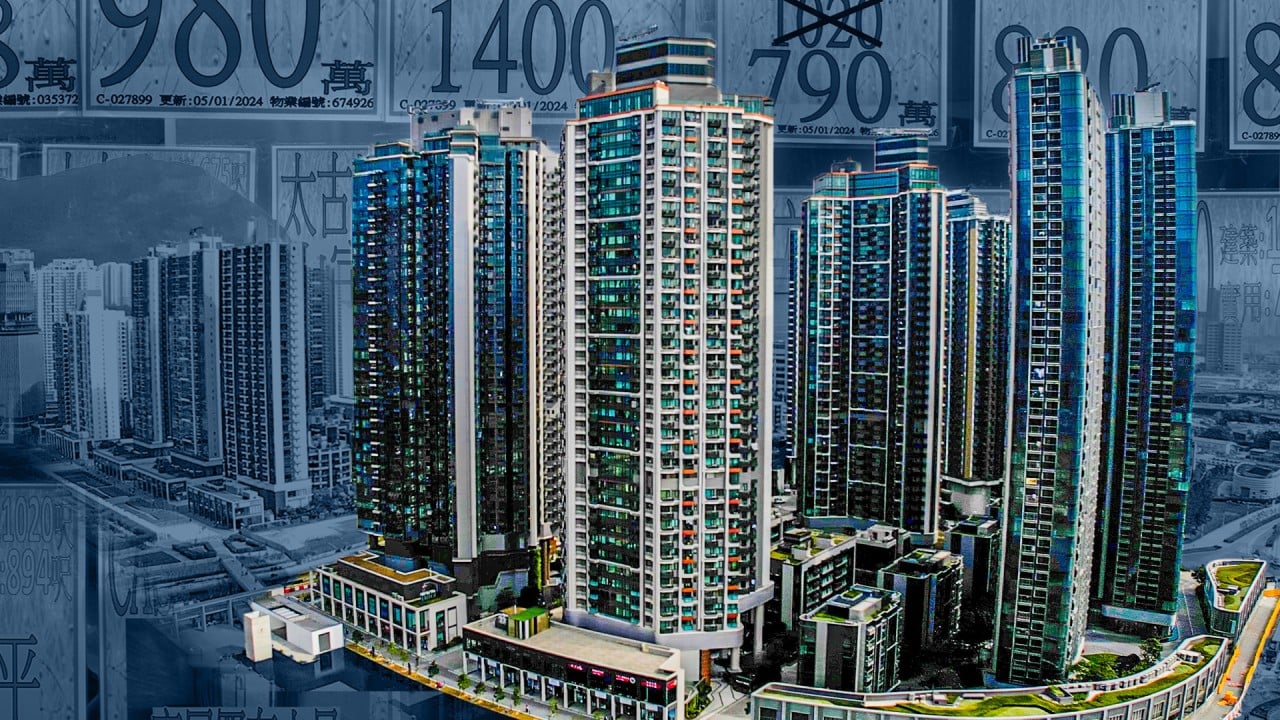

A man looks at property prices displayed in the shop window of an agency in Wan Chai on February 27, a day before the financial secretary scrapped all property market cooling measures. Photo: Jelly Tse

Opinion

Regina Ip

Regina Ip

Hong Kong financial secretary’s hands were tied – but he got at least one thing right

With many negative factors weighing on the economy, Financial Secretary Paul Chan had little wiggle room

The scrapping of property market cooling measures was a good move given the knock-on effect on the economy of falling home prices and the sector’s importance to the economy

Financial Secretary Paul Mo-po Chan had few palatable options before him when he drew up the 2024-25 budget.

The government has been running a fiscal deficit almost every financial year since 2019, and the forecast deficit for 2023-24 would have widened to HK$173 billion (US$22.1 million) but for a bond issue of HK$72.5 billion. Measures to balance the budget, whether cutting back on welfare expenditure or raising taxes, are sure to generate a substantial backlash from a public accustomed to low taxation and generous handouts.

To raise revenue, the government had toyed with the idea of introducing new taxes, but backed off given the adverse market reaction. Even after Chan ruled out introducing a capital gains tax on January 17, the Hang Seng Index still experienced a steep decline that day as his clarification was seen as being not categorical enough.

Raising government fees and charges on a “user-pays” basis had also been floated. Water and sewage charges, and more, are indeed long overdue for an increase. But any such increase is bound to hit the grass roots hardest, and raise business costs at a time when the economic recovery is fragile.

Chan trod extremely carefully and he confined tax increases to limited items – a modest increase in business registration fees by HK$200, a 1 per cent increase in salary tax for an estimated 12,000 taxpayers whose net income exceeds HK$5 million, a progressive rating system for domestic premises from the fourth quarter of 2024-25, and resumed collection of the hotel accommodation tax, at a rate of 3 per cent, effective next year.

Altogether they are estimated to generate no more than HK$3.16 billion in the coming year, a pittance compared to the forecast deficit of HK$143 billion before bond issuance. Chan cannot be faulted for reckless tax hikes that could rock the boat.

Chan’s hands are tied when it comes to boosting the economy, given that most of the negative factors weighing on the economy – high interest rates, the strong US dollar, ongoing geopolitical tensions – are out of his control. Despite these constraints, Chan got one key policy right: the scrapping of all “demand management” property transaction stamp duties that had been introduced since 2010 to rein in skyrocketing home prices.

The debate over these stamp duties – Special Stamp Duty to curb speculation, Buyer’s Stamp Duty to dampen external demand, and the New Residential Stamp Duty to counter market exuberance – tells a poignant story about how the government battled rising angst about runaway home prices through fiscal intervention. The stamp duties brought the government a windfall of land revenue, and the buoyant property market led many to believe that the sun would never set on the property sector.

To address deep-rooted discontent about the concentration of wealth among homeowners and young people’s inability to own their own homes, the government doubled down on its efforts to step up land and housing supply.

As the result of the government’s determined efforts, Chan was able to announce in the budget that it had identified land for meeting the supply target of 308,000 public housing units in the next decade, and would be able to achieve completion of 19,000 private residential units in the next five years, a 15 per cent increase over the annual average of the past five years.

The unexpected economic downturn resulting from the pandemic, the rapid ratcheting up of interest rates and abundant supply coming on stream sent the property market into a nosedive. Louis Chan Wing-kit, vice-chairman of Centaline, one of Hong Kong’s largest property agencies, said last month that compared to the market peak in September 2021, second-hand home prices had plunged nearly 24 per cent in less than two-and-a-half years. Chan estimated that the value of Hong Kong’s property market had dropped below HK$10 trillion, representing an evaporation of wealth equivalent to HK$2.6 trillion.

The negative wealth effect of such a sharp fall in property values sent ripples across the economy, depressing consumption and investment, creating drags on the economy that the financial secretary had to address. With the property sector having been a key driver of Hong Kong’s growth for decades, the government had no choice but to eliminate the stamp duties. Otherwise, continuing pessimism could have led to a collapse of confidence.

Soon after the announcement, there were reports of homeowners asking for higher prices, and brisker transactions returned. With weak growth, it is unlikely that there will be a surge in demand in the near future, but the abolition of the stamp duties will ensure property prices don’t end up in a free fall.

13:00

How Hong Kong's housing market became among the world’s most unaffordable

How Hong Kong's housing market became among the world’s most unaffordable

The government is determined to broaden Hong Kong’s economic structure by making a belated move to promote “high-quality growth” through scientific innovation and technology. In recent years, the government has poured billions into building the infrastructure for technological development, making land available for tech parks and funds for tech investment.

Substantially enlarged science parks in the planned Northern Metropolis at the border with Shenzhen are intended to be flagship developments that will jump-start Hong Kong’s tech-based industries. Hong Kong started late, and it will be a while before investments generate the desired returns.

In the absence of near-term gains from its tech investments, the property sector and tourism remain Hong Kong’s chief engines of growth. It is to Chan’s credit that he managed to steer clear of controversies that would raise the political decibel levels at a time when the government’s top priority is to ensure the passing of national security legislation in accordance with Hong Kong’s constitutional obligation under Article 23 of the Basic Law. There is no promise of immediate economic turnaround, but Chan’s cautious navigation should ensure a soft landing.

Regina Ip Lau Suk-yee is convenor of the Executive Council, a lawmaker and chairwoman of the New People’s Party