Overseas real estate and soccer clubs in crosshairs as China ramps up investment clampdown

Hong Kong property could take a hit as State Council slaps restrictions on dealmakers

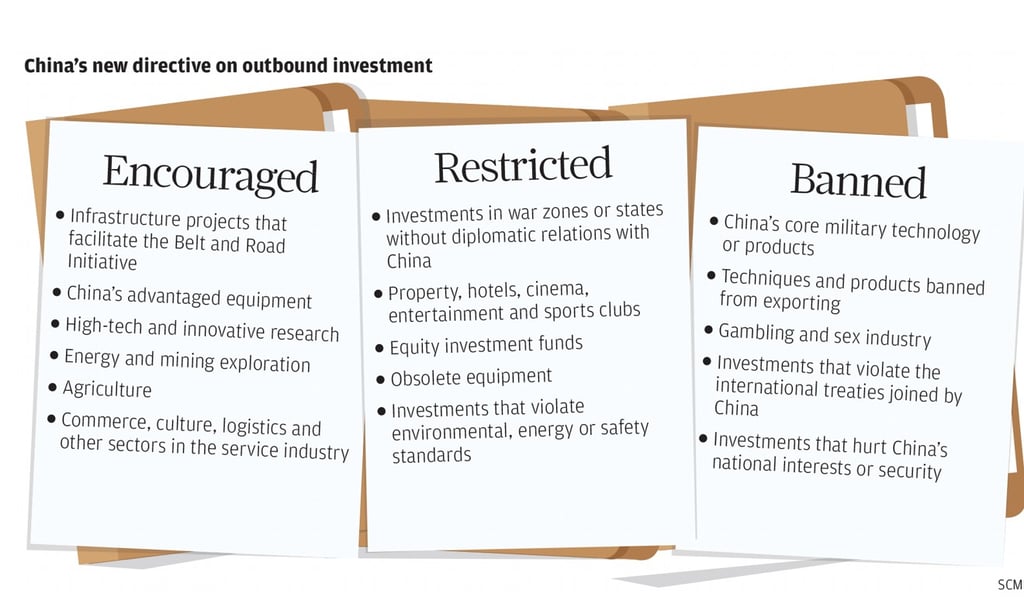

Chinese investors will have to get special approval from Beijing to put their money in overseas property and sports clubs under tough new restrictions released on Friday.

Amid fears of broader financial insecurity, the State Council said companies would also need regulatory approval for outbound investments in hotels, the film industry and other forms of entertainment on its new formal restricted list.

Similar restrictions apply for companies setting up overseas equity funds or investment vehicles not tied to specific projects.

China has launched a campaign to curb “irrational overseas investment” and aggressive dealmakers such as Anbang Insurance Group, Fosun International, Dalian Wanda Group and HNA Group Co have been under pressure. The list issued on Friday formally set the boundary for Chinese outbound investment.

Tao Jingzhou, managing partner of a law firm Dechert, said the rules marked a major retreat from the overseas investment push promoted over the last few years.