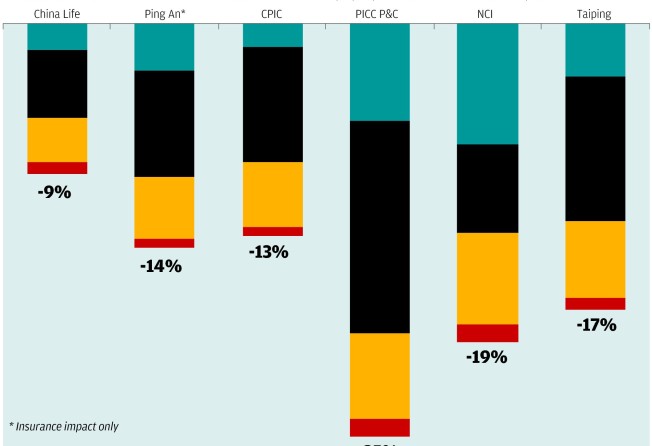

Fears of rising mainland default risks have set investors scrutinising the exposure of insurers to "non-standard" and growth-levered assets - those potentially most susceptible to losses if the credit bubble bursts. But analysis by Macquarie Bank pinpoints traditional assets as the real danger for insurer enterprise values in the event of widespread defaults, not their more exotic holdings. Almost all of the 9 per cent to 25 per cent decline in enterprise values that a bursting bubble might trigger would come from stocks, property and bond holdings. "We consider China Life to have the safest book," Macquarie analysts wrote in a note to clients. "At the other end of our risk spectrum are Taiping and Ping An."