Micro loans are Asia’s hottest fintech products as Gen Z and millennial online shoppers prefer to buy now, pay later

- Buy now, pay later (BNPL) services may double their share of Asia’s e-commerce payments market from 0.6 per cent to 1.3 per cent, according to forecasts

- Chinese fintech firms have invested in Southeast Asia’s BNPL services: Ant Group owns 6.3 per cent of India’s Paytm and 39 per cent of South Korea’s Kakao Pay

For Marcus Khoo, perfumes and oil diffusers were never high on his shopping list. They would have sat idling in his online shopping cart, were it not for a hire-purchase instalment payment option that tipped the balance in his decision.

“I like it because you pay less for the item at the start and there is no interest, unlike a credit card,” said Khoo, a 26-year-old social media executive who has used the option three times this year. “You still pay the full price, except it is split across different time periods. The pain of your money departing from your wallet is delayed, compared to paying it off in one shot.”

consumer credit to shoppers on June 6, 2021. Photo: Bloomberg")

It is the fastest-growing online payment method in countries including Australia, Japan, Malaysia and Singapore, according to the report, at the expense of credit cards, bank transfers, cash on delivery and prepaid cards, all of which will lose share through 2024.

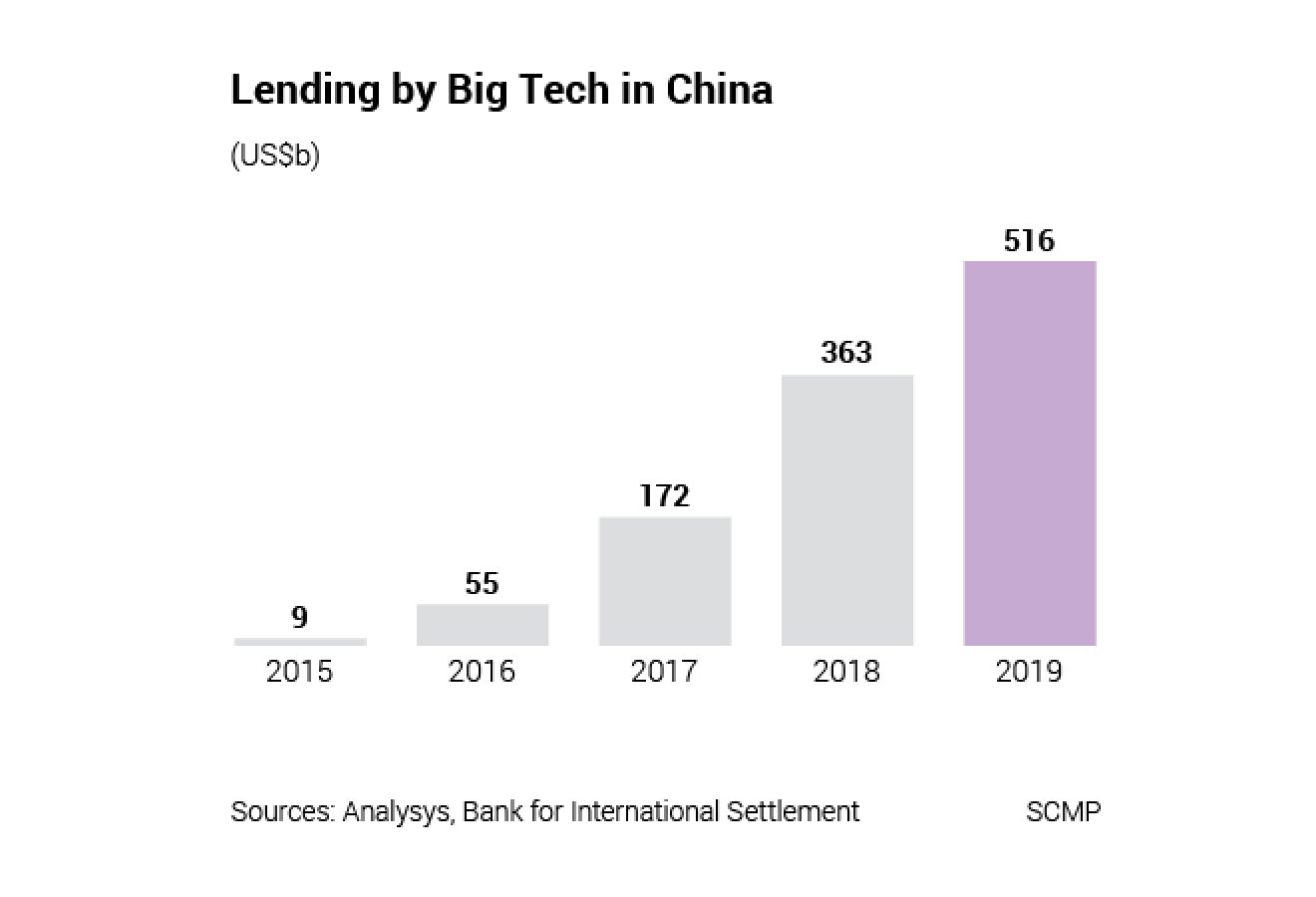

“The buy now, pay later industry in China has developed rapidly in the past few years, although people usually see it as online microlending,” said Han Feng, a partner at McKinsey in Shanghai. “But it is an area getting regulated now, so the industry has gone through dramatic changes and growth has slowed.”

Which are the dominant e-payment methods in the Asia-Pacific region?

| 2020 (%) | 2024 (%) | |

|---|---|---|

| Digital/mobile wallet | 60.2 | 65.4 |

| Credit card | 19.1 | 18.1 |

| Bank transfer | 6.5 | 4.1 |

| Debit card | 5.8 | 7.1 |

| Cash on Delivery | 4.1 | 2.0 |

| Prepaid Card | 1.1 | 0.4 |

| Postpay | 1.0 | 0.5 |

| Charge and deferred debit card | 0.8 | 0.4 |

| Buy now, pay later | 0.6 | 1.3 |

| Direct debit | 0.3 | 0.3 |

| Other | 0.3 | 0.3 |

| Prepay | 0.2 | 0.1 |

To be sure, China’s online microlending products differ from the BNPL services seen in the West. Huabei, which means “just spend it”, works more like a virtual credit card that provides borrowers up to 40 days of interest-free loans.

Most BNPL plans draw their revenue from the increased spending at merchants, leaving shoppers to enjoy their interest-free credit.

Some of these services – like LexinFintech’s Maiya and Happay – are offering interest-free BNPL loans. Hong Kong, Singapore and the rest of Asia are also warming up to BNPL.

“The online microlending trend has been slowing down in China, but for some Southeast Asian markets, there is still a good chance of growth, particularly for Thailand and India [where there is] a lack of credit cards,” said Han. “This region is now like the early stage of China’s marketplace.”

BNPL loans are popular in Asia as they fill a sweet spot for both consumers and merchants. Shoppers are attracted to the payment niche as it stretches their dollar, while merchants welcome higher sales volume.

“Despite the high adoption of digital payments globally, what was missing for consumers was paying in multiple periods,” said Warren Hayashi, Asia Pacific president of the Dutch payments processor Adyen, which handles online and in-store payments through a single platform for merchants.

“You sometimes see instalment payments for higher-ticket items. These are legacy solutions owned by banks; consumers have little choice on how to pay over a period of time.”

BNPL services received a boost during the global Covid-19 pandemic, as social distancing rules channelled cash usage towards contactless online payments, while job displacements increased the need for short-term credit.

Millennials and so-called Generation Z – those born between the late 1990s and the early 2010s – are the biggest adopters of BNPL services, said Arvin Singh, co-founder of the BNPL service Hoolah, in Singapore.

Launched in 2018, Hoolah offers BNPL services in Hong Kong, Malaysia and Singapore through stores like Zalora, Klipsch and GNC. It declined to reveal its number of users but cited a 400 per cent growth in users in the last year.

“These shoppers – aged 25 to 35 – are savvy, they value payment flexibility and better cash flow,” Singh said. “It also serves the underbanked – those without access to credit cards – and gig economy workers. We also notice [younger consumers] prefer using debit over credit.”

Unlike traditional hire-purchase, BNPL services are products of the mobile internet, offering interest-free loans for small sums, typically from a minimum of about HK$100 on average.

They get the product upfront, after making the first instalment payment. In stores, consumers pay by scanning QR codes. Online BNPL services are built into the payment options, a trend that is increasingly being embraced by merchants, said Hayashi. Sweden’s Klarna Bank and Australia’s Afterpay are two of the big fintech names that Adyen has added to its platform.

For merchants, BNPL typically costs more than credit cards. But providers say merchants enjoy larger baskets and more paying customers in return. Often, the provider takes on the credit risk, pays merchants in full upfront and handles users’ repayment.

Atome, a Singapore BNPL provider operating in nine Asian markets, charges merchants fees that are higher than 1 to 3 per cent of transactions, the rate that credit card companies impose.

“We take on the risk of customers not paying,” said Atome Hong Kong’s general manager Eric Yu. “Built into that fee are costs like marketing, vouchers, and credit card costs that we bear.”

Founded in 2019, Atome serves over 20 million registered users in Asia. It is a subsidiary of fintech company Advance Intelligence Group.

“In return for paying for this service, it has been proven that merchants enjoy higher sales and transaction sizes of up to 30 per cent, while enjoying lower customer acquisition costs compared to traditional channels,” said Yu.

The BNPL craze has attracted traditional banks into the fray too, as they aim to cash in a market that may grow 43 per cent annually over the next three years, according to FIS-Worldpay’s forecast.

Users can split their bills into instalments from three to 36 months, leveraged on a MasterCard debit account. They pay a monthly handling fee of about 0.20 to 0.80 per cent of the transaction, depending on their credit assessment result. About 42,000 users have signed up for their product as of date and the average tenure is 12 months.

application in front of a Zara store in Singapore on 5 June 2021. Photo: Bloomberg.")

As the sector matures, the trend is drawing regulators’ attention too, criticised for weak credit checks or encouraging overspending. The Hong Kong Monetary Authority (HKMA) said customers should be aware that some providers of buy now, pay later services might not be regulated, typically non-bank institutions, in an emailed response to the Post.

For banks, buy now, pay later plans fall under personal credit products and are subject to regulations, such as a “double reminder” for users – emphasising the product features and key details including interest rates and repayment arrangements, HKMA said.

Livi, as a licensed bank in Hong Kong, runs credit checks with its own risk models built on data from various sources, including the Credit Bureau and from its shareholders. Most applications do not require income proof from users.

Non-bank institutions have comparably softer credit checks. Atome assesses users with its credit profiling technology in two minutes, requiring the user’s personal details, identity documents and an active debit or credit card linked to their account.

BNPL products will go mainstream and experience high growth, Hung said.

“Hongkongers have been using instalment plans for a long time,” she said. “Buy now, pay later is just a different way of doing it and some might not know yet what the term means. But they are practical and smart. Once they see such plans as something that adds value or help with cash flow, they will jump in.”