Hong Kong virtual banks’ profitability hinges on their ability to harness payroll accounts, says KPMG

- Hong Kong’s eight virtual banks, expected to launch operations in the first quarter of 2020, are likely garner up to three per cent of the city’s deposit base, says KPMG

- Scramble for payroll accounts could intensify after 2020, as virtual banks compete for low-cost funding source

The success of Hong Kong’s virtual banks depends on their ability to convince customers to switch their payroll accounts from traditional banks, which would give them access to a low-cost and stable funding source, helping them to grow their loan books profitably, according to KPMG.

Virtual banks are expected to corner only two to three per cent of the city’s deposit base in the first year because they will be able to attract only a few thousand customers each, said Paul McSheaffrey, head of banking and capital markets for Hong Kong at KPMG China, during the release of the accounting firm’s 2020 Hong Kong banking outlook, on Wednesday.

KPMG expects 2020 to be a challenging year for the city’s banking sector because of unrelenting pressure on banks’ net interest margins and revenue growth.

“When customers start to switch their payroll accounts to virtual banks, it will have a more tangible impact on the profitability of virtual banks,” said McSheaffrey, adding that it would not happen “after 2020”.

However, the virtual lenders are unlikely to initially create a big dent in the loan books of the 164 traditional banks that operate in Hong Kong, he added.

Local currency deposits at Hong Kong’s banks and authorised institutions stood at HK$6.9 trillion (US$881.3 billion) as of October, according to data from the Hong Kong Monetary Authority

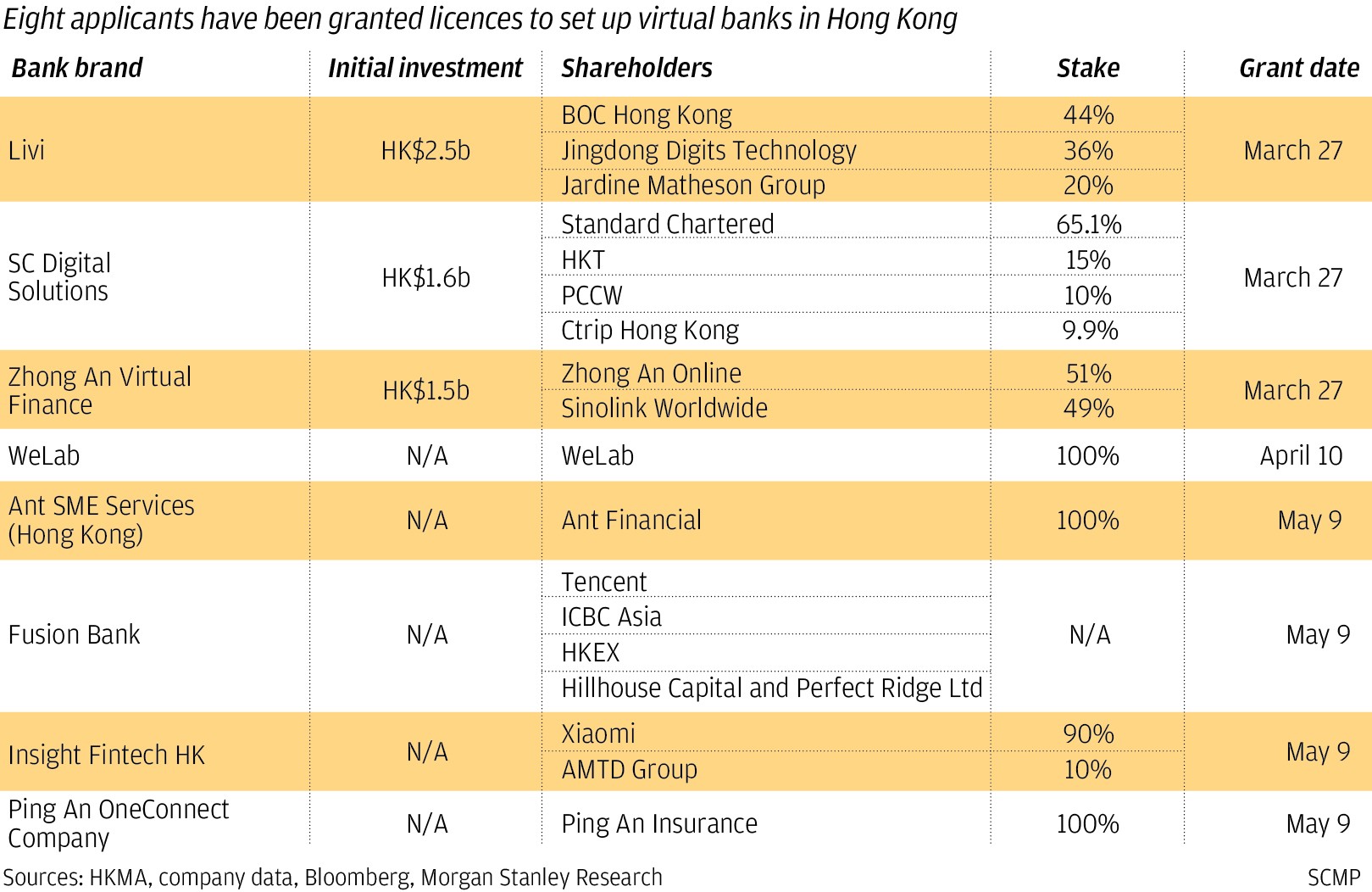

HKMA, the city’s de facto central bank, has issued eight virtual licences to companies including Standard Chartered Bank, Bank of China (Hong Kong) and Ping An OneConnect Bank.

As banks pay no interest to payroll account holders, there is hardly any incentive for customers to switch banks to those which their employers pay their salaries into. Hence, such a cheap funding base would enable virtual banks to steadily interest income on their loans with more certainty.

McSheaffrey expects virtual banks to stick to retail business initially, focusing on providing loans through their retail partners and gradually move into longer term lending, such as mortgages.

What to expect as launch of Hong Kong virtual banks nears

For the past year, WeLend, a subsidiary of WeLab which is one of the eight licensees, has been offering instant cash loans to customers at outlets of 3 Hong Kong, the telecom and internet services arm of conglomerate CK Hutchison, using real-time credit assessment technology.

KPMG expects virtual banks that focus on servicing small and medium enterprises to have a bigger impact on traditional banks during the first three to six months of their launch.

As SMEs have traditionally been underserved by banks, these small companies are more likely to be more tempted to use virtual banks, or switch over to one, and seek credit from these new players, it said.