Doubts rise over Li & Fung future

Loss of another US deal sends jitters through market over sourcing role

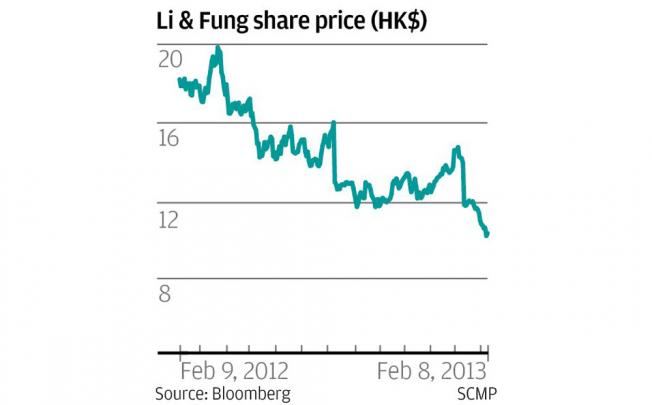

Shares in Li & Fung plunged to a new low of HK$9.93 yesterday after the company lost another contract from a US client, renewing fears that the biggest distribution and trading company in Hong Kong is losing its middleman role in global trade.

But the stock later rebounded to close 1.38 per cent higher at HK$10.26 after the firm said Fifth & Pacific did not renew the contract because of domestic warehousing and the financial implications would be small.

{kind=link}

A spokeswoman stressed that its sourcing contract with the New York-listed company, which owns brands such as Kate Spade and Juicy Couture, would remain.

Analysts are concerned about the company's short-term prospects though, as some expect it to lose more sourcing business while its budding designing and distribution operations have yet to become profitable.

One analyst said Li & Fung, which hit HK$52 in 2011, could fall further to HK$8.15.

"Li & Fung's operating margin is likely to remain squeezed as costs and prices continue to climb on the mainland, which makes up more than half of the company's supply," said Gabriel Chan from Credit Suisse. "While the company is still a solid business, they will do more for less."

Two major Li & Fung clients, US children's clothing retailer Carter's and Wal-Mart, reduced their reliance on the firm last year as they started to develop their own sourcing divisions.

But Charles Yan, an analyst at Standard Chartered Bank, said this year might mark the turnaround for Li & Fung. "We believe most of the negatives have already been priced in, given the significant share price pull-back since the profit warning," he wrote in a report, adding that the market had oversimplified the negatives.

The stock has slumped 27 per cent since the firm warned shareholders of a 40 per cent drop in core operating profit on January 11. But Yan said most of the losses came from the expenses to restructure its brands and business model, which he said was a good decision as many of the brands offered low profit margins and made little contribution to revenue.

Standard Chartered expects the company's net profit to more than double to US$781 million this year.

But Yan was among the few optimistic analysts. Only four of the 18 brokerage firms that tracked the company recommended buying the stock, and even if they did, they all slashed the target price.

Li & Fung has acquired a number of brands such as TVMania and Crimzon Rose in the past two years to bolster distribution, but many of these brands were considered by the market as trivial.