Price gap narrows between Shenzhen and Hong Kong stocks ahead of connect plan

The average price gap in 89 stocks that are dual-listed on the mainland and Hong Kong has narrowed to 21 per cent from as much as 46 per cent

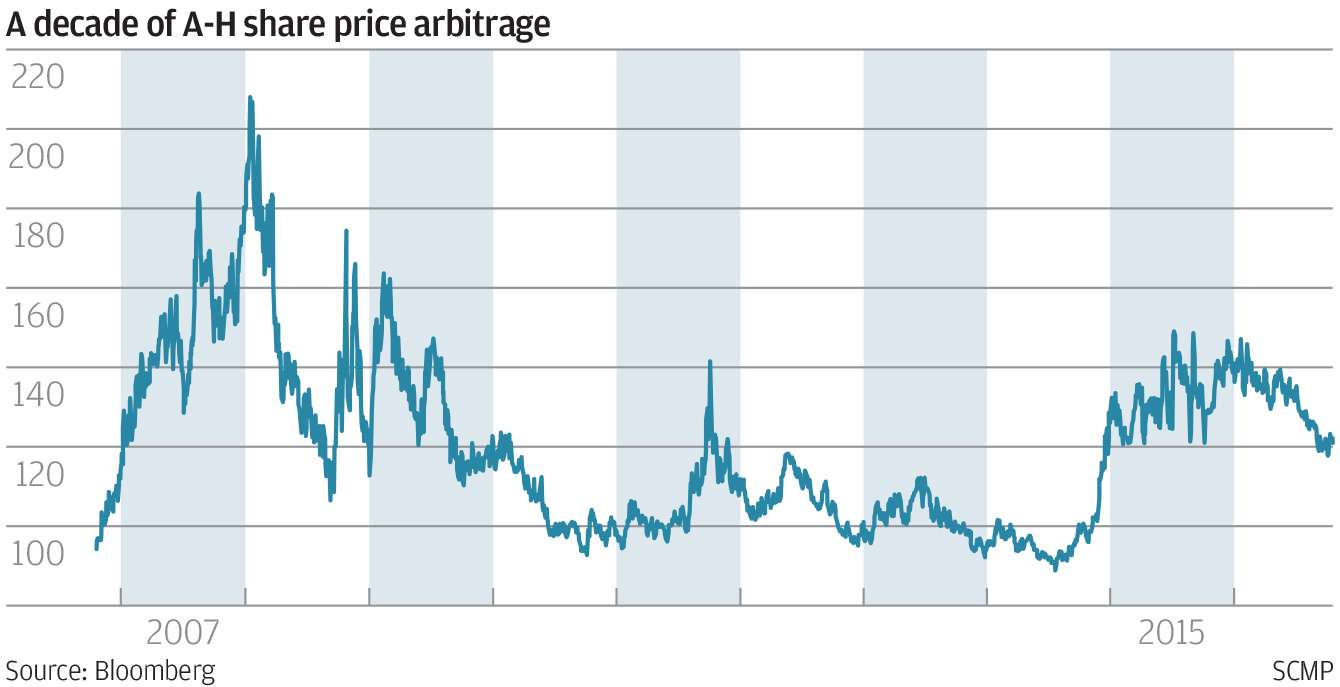

The price arbitrage between shares listed in Shenzhen and Hong Kong have narrowed ahead of the imminent launch of the so-called stock connect programme, most likely in late November.

There are 89 companies with shares listed both on mainland China’s stock exchanges and in Hong Kong. The prices of these mainland-listed A shares trade 21 per cent higher on average than their H-share counterparts in Hong Kong in recent trading.

The price gap has narrowed from as high as 46 per cent in February, according to Bloomberg data.

Shares of Shenji Group Kunming Machine Tool, a designer and manufacturer of machine tools, rose to 8.30 yuan (US$1.22) in Shanghai while its H shares closed Wednesday at HK$2.67 (34 US cents) in Hong Kong.

Mainland-listed shares have been trading at a premium to their H-share counterparts since May 2006 as the country’s admittance into the World Trade Organisation five years earlier heralded a new age of economic growth, which spilled over to investments in the country’s equity market.

In August 2007, the mainland authorities considered creating a so-called through-train scheme that would allow its investors to trade Hong Kong shares and vice versa.

A new economic zone in Binghai in the port city of Tianjin was set aside as the testing ground for the plan.

Following the announcement of the scheme, a buying frenzy of A shares caused the price premium to surge to a record 108 per cent in January 2008.

Some speculators even resorted to carrying cash through underground banks to load up on Hong Kong stocks in the hope that they could cash in when prices on the two markets converge.

However, the through train never made it off the drawing board as the country’s currency regulator, concerned that rampant capital flight could stymy the local market, put a stop to it.

That caused the mainland stock market to crash. For a while between 2010 and 2014, at least for the 89 companies with shares traded in both mainland China and Hong Kong, their mainland listings were cheaper than their H shares.

In 2014, mainland regulators brought back the idea of liberalising the country’s equity market to allow its investors to trade abroad and for foreign investors to own mainland stocks.

A new name was chosen, the stock connect, and the Shanghai bourse was the favoured testing ground.

That spurred renewed interest in Shanghai shares, which make up 71 of those 89 companies with dual mainland and Hong Kong listings. The average price premium rose in October 2015 to as much as 46 per cent.

The A-H premium is especially pronounced for smaller companies with low market capitalisation because they are favoured by the mainland’s mom-and-pop investors, who make up 80 per cent of trading, whereas professional funds and investors tend to buy Hong Kong’s blue-chip stocks based on valuation, according to a report by China International Capital Corp.

“A-share investors will continue to favour small-cap stocks because they firmly believe volatility arising from the stocks could create more opportunities to make profits,” said Shen Ye, a Shanghai-based hedge fund manager. “Valuation of small-cap stocks on the mainland will remain relatively high.”

Analysts said the stock connect schemes would not help close the A-H price gap because northbound funds from Hong Kong would never blindly chase small-cap companies whose fundamentals cannot support prices.

“You can’t expect mainland retail investors to be as rational as international institutions,” said Shenwan Hongyuan Securities analyst Qian Qimin. “When the mainland stock market is swamped by cash, a strong liquidity could drive shares up to an elevated level with investors ignoring the fundamentals.”

This article has been amended to correct the percentage increase in the A-H price premium in January 2008 and the year when the average premium rose to as much as 46 per cent