New | Roller coaster ride exposes Hong Kong GEM’s weaknesses

With four issuers on the Growth Enterprises Market board shot down by regulators, should one expect Hong Kong’s farmers of corporate shells and price fixers to be in mourning?

Not at all. It’s business as usual. They say wherever there’s a rule, there’s a way. The name of the new way is Patience.

The story of version 2.0 is best told through the IPOs of two GEM-listed stocks within a week of each other last month.

The duo are typical of the second board, exhibiting various red flags of a listed shell as defined by the Hong Kong Stock Exchange - small fund raising, minimal market capitalisation and deteriorating profit.

Both launched their share sales within days of a January statement by the Securities & Futures Commission and the Hong Kong Stock Exchange threatening to block stock listings in the case of bogus share allocations.

Let’s start with Dadi’s IPO debut two days after Valentine’s Day.

It was the first company to abandon full placement, selling 10 per cent via public offering to more than 4,400 shareholders.

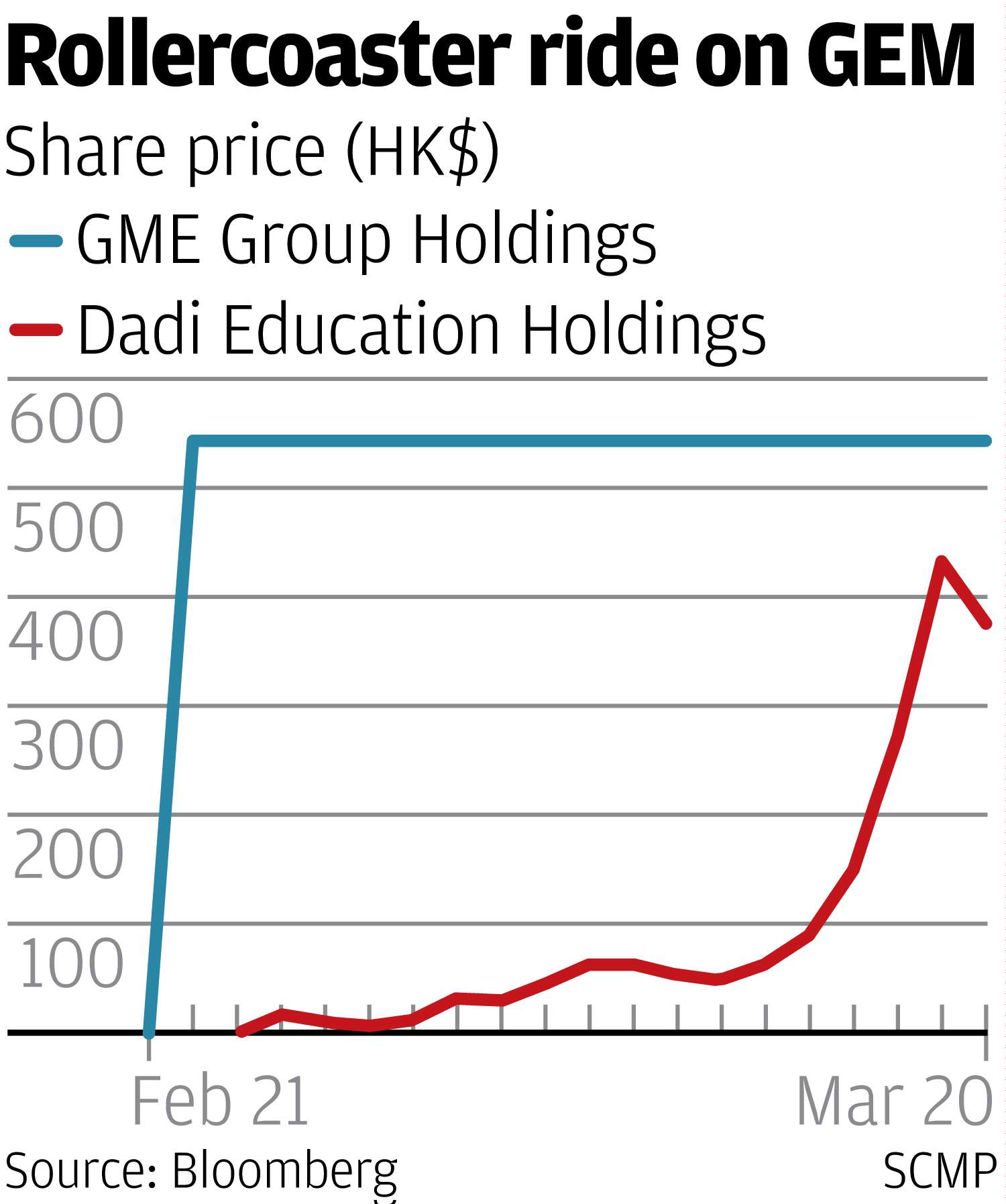

During its February 16 IPO debut, the stock price fell as much as 5.9 per cent when shares traded for the first time, dropping below the IPO price and breaking the long-held tradition among GEM companies of bumper first days.

Meanwhile, at GME, the story began with a manipulated free flow of stocks via the so-called full share placement. Three shareholders control 67.5 per cent of the company’s stock.

They sold shares by placements to 167 placees, a token gesture over the minimum 100 required by regulators.

If that wasn’t enough to teach GME a lesson, the company’s share performance did. The stock price surged fivefold within the first hours of trading on February 22, and got itself subsequently suspended.

GME’s three controlling shareholders recently promised to upload 5 per cent of their holdings to another 150 independent investors to broaden the float. The regulators are yet to budge to allow the stock to resume trading.

The SFC was happy enough to point out last week that the average first-day rallies had been slashed to 4.2 per cent since its January ultimatum, compared with the 656 per cent surge in 2016.

That almost made Dadi the poster boy for the newfound discipline amid the regulators’ crackdown.

Except, it isn’t quite. If one zooms out from the first trading day to a month, the emerging picture would rain on the regulators’ parade.

Dadi’s shares hovered around its IPO price of HK$0.34 for almost a month, before staging a three-day rally last week, surging to HK$1.70 on Friday, and then dropping 31 per cent to HK$1.17 two days later. Deja vu.

Whether or not it was orchestrated, the February 17 dive in Dadi’s stock price -- as much as 19 per cent off its IPO price -- would have scared minority investors into dumping whatever they have received via the public offer.

In between, Head & Shoulders’ holding increased from 14.45 per cent to over 21 per cent, leaving fewer than 4 per cent with other brokers, according to records by the Hong Kong Securities Clearing Co.

If the stocks have been cornered by a few, the subsequent price surge would hardly be a surprise. Whoever smart or lucky enough to bottom fish last month would be sitting on a profit of over HK$100 million.

Money Matters asked Dadi’s financial controller and company secretary Hedley Tam if the company was aware of any reason behind its stellar performance and whether they suspected anyone cornering its stock.

“The company is not in a position to comment on both of your enquiries,” Tam said .