Exclusive | Is the Hang Seng Index’s blue dye a blessing or a curse?

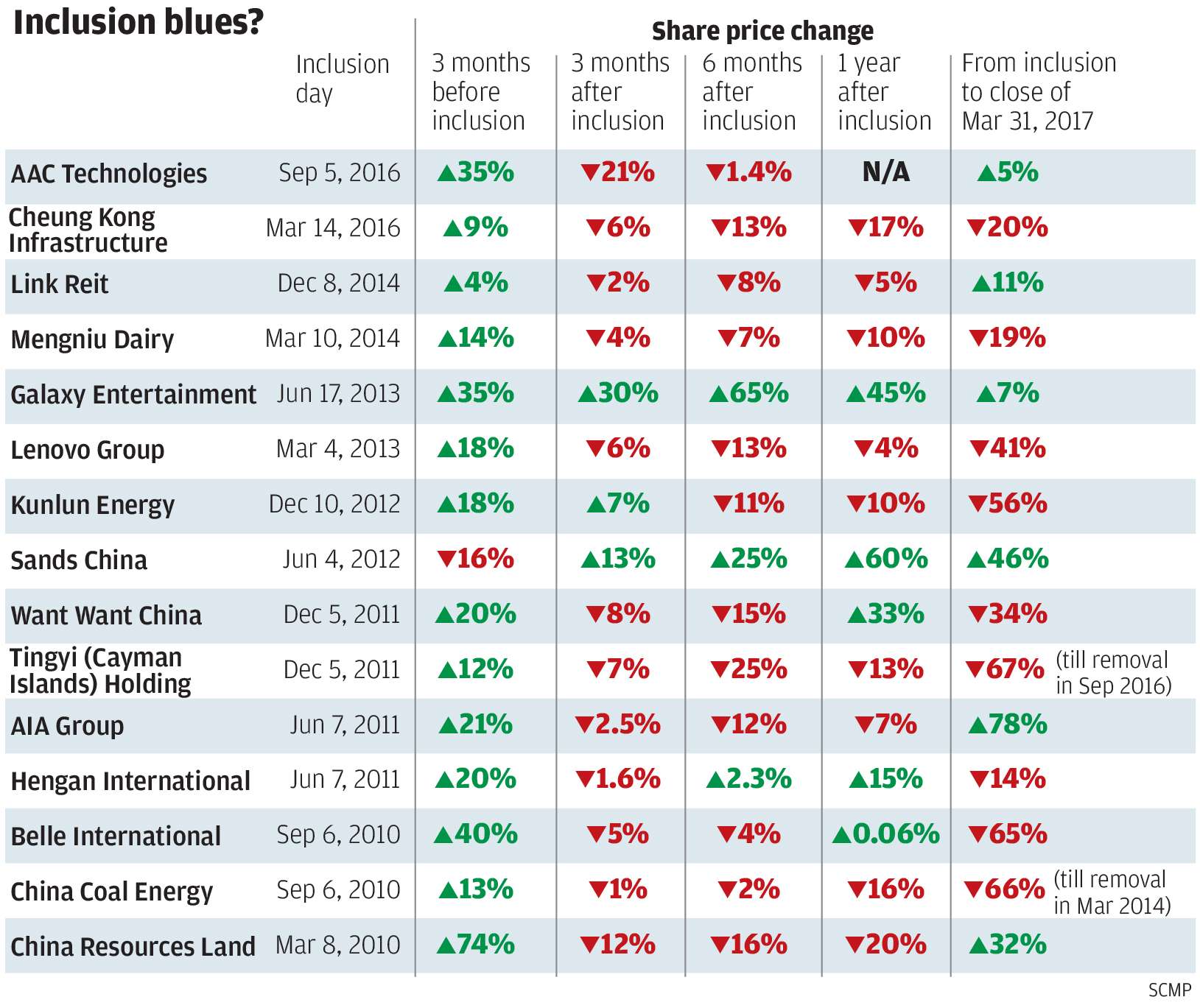

Research by the Post shows that 12 of the 15 stocks that were added to the Hang Seng Index fell in the three months after their inclusion, and 60 per cent of them have not recovered.

Being chosen as a Hang Seng Index (HSI) component stock, or being “dyed blue” as the local saying goes, might reasonably be considered a blessing for the share price of the chosen one, because passively managed funds that track the blue chip index have to add the stock to their holdings.

The data shows quite the opposite. An analysis of stock performance over the past seven years shows that 12 of the 15 “dyed blue” stocks declined three months after joining the Hang Seng index, while 60 per cent still haven’t recovered to this day.

“Many blue chips soared to excessively high levels before joining the index as speculators bought the stocks with the hope of quickly selling them to index-tracking funds,” said Ben Kwong Man-bun, head of research and executive director at KGI Securities.

Realignment of the weightings, or “rebalancing” by index funds, usually takes place one day prior to the implementation of an index reshuffle.

When the speculative bubble eventually bursts, it usually takes a long time for the stock to recover.

“The excessively high share prices have discounted all the existing good news about the company. So after the bubble bursts, stocks may pull back sharply or ‘go asleep’ for a long time, until investors find new reasons to speculate,” Kwong said.

Ken Wong, Asia equity portfolio specialist at Eastspring Investments, said inclusion in the blue chip index might seem like a great accomplishment. “[But] the biggest problem is that index inclusion just creates a temporary positive sentiment for stocks.

“Some investors tend to speculate on these index inclusion stocks for short term gains,” he said. “People usually buy on rumours and sell on fact.”

Looking at the 15 blue chips that joined the HSI from 2010 to 2016, nearly all were on a strong upward momentum and had risen for several months or even years before the announcement of the index reshuffle.

Between the index reshuffle and the implementation day – usually three to four weeks – 13 out of the 15 stocks gained. However, one year after inclusion, only five stocks were above the levels traded on inclusion day.

As of the market close last Friday, there are still nine stocks whose prices are lower than their levels when joining the index.

“Many stocks may appear more volatile after they join the HSI as the liquidity has increased,” said Kwong.

“It doesn’t mean these stocks are not good companies,” he said. “They usually have solid financial performance and are in the prime time of the industry life cycle. But share prices are driven more by liquidity, not necessarily by fundamentals.”

Blue chip candidates are already “hot stocks” in the market before being noticed by the index, trading on relatively high turnover.

But whenthe Hang Seng Indexes Company reviews the index on a quarterly basis and selects new constituents based on their turnover, market value, industry type and financial performance, the stocks become even “hotter” in the eyes of many investors.

“I don’t think it’s a curse,” said Alex Wong, director of asset management at Ample Financial Group.

“The shares are just overbought before the index addition. But the surge is difficult to sustain. It’s reasonable to have a correction afterwards. After all, being included in the HSI is just a one-time thing,” he said. “It’s a one-time story.”

“These stocks have continued to provide reasons for investors to buy in,” Wong said. “They have a story to tell, such as their booming industry.”

Apple closed at a fresh record high last Wednesday, pushing its market cap to above US$771 billion.

AAC Technologies also touched an all-time high of HK$98 late last month.

However, Kwong is concerned that index stocks may become more speculative as market liquidity increases on the back of strong money inflows from mainland China.

“This is the trend,” he said. “We are seeing an increasing number of momentum investors.”