Opinion: Fixing power utility returns for 15 years is so nineteenth century

Hong Kong has become steadily more efficient in power usage over the last 12 years

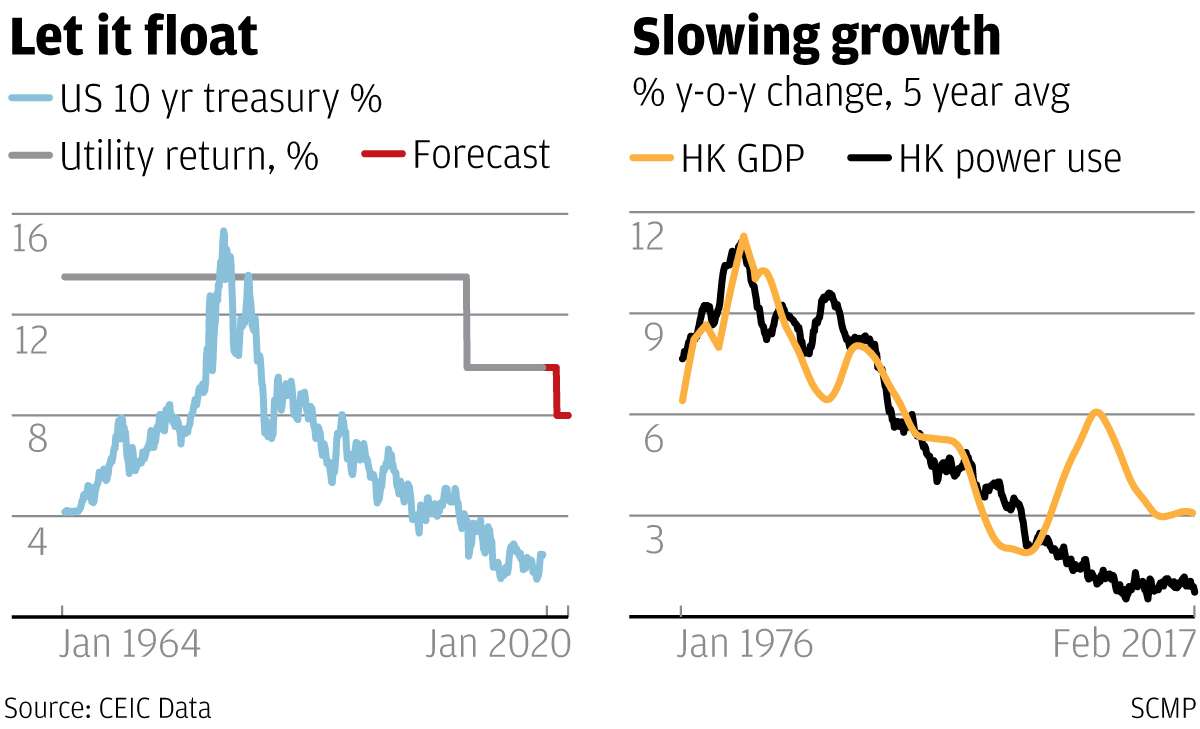

The amount the two [electricity] suppliers are allowed to earn will be slashed from 9.99 per cent to 8 per cent of their net fixed assets after a new 15-year regulatory agreement with the government, known as the scheme of control, replaces the existing one next year.

SCMP, April 26

Have you ever looked at one of those 19th century railway bond certificates with which many banks decorate the walls of their conference rooms?

What you routinely see is a drawing of an old steam engine with a formal script underneath telling you that the company promises to repay etc. Underneath this are 70 or so small detachable coupons for the annual interest payments.

Of course it is rarely the full 70. You have to assume that the railway company paid up for a few years but the reason there are any coupons left is that no-one could collect on them. At some point the railway went bust.

A question always strikes me when I look at one of those bonds: How could the issuer so blithely assume that an initial coupon rate of, let’s say, 3 per cent would still have any meaning 70 years later? How could anyone guess what prevailing interest rates would be in 70 years?

The answer, of course, is that back then you could. The British Treasury’s Consolidate Fund bonds, for instance, first offered in 1751, paid a coupon that varied only between 2.5 per cent and 3.5 per cent for all of their history until they were fully redeemed in 2015.

For almost 200 years consols were a bedrock of wealth. Read up on Jane Austen if you don’t believe me. Yields on financial investments didn’t go way up and down back then.

But they can do so now. Just look at that track in the first chart of 10-year US treasury yields over the last 60 years, and don’t tell me that the US Federal Reserve Board can keep interest rates on the zero bound forever and ever, life without end, amen.

There was a period in the early 1980s when the basic permissible return of 13.5 per cent on fixed assets did not really look all that good. In fact, an 8 per cent return in the present yield environment looks better than 13.5 per cent in the 1980s environment.

I think 8 per cent today is a perfectly good return figure. What is wrong is fixing it for 15 years. Whatever the best way of regulating power utility profits, a floating return rate based on something like the US 10-year treasury yield must surely be part of it these days.

I draw your attention also to what the second chart shows. Power supply was a high growth business in the 1980s but it barely registers 1 per cent growth now, less than the trend rate of gross domestic product. Hong Kong has become steadily more efficient in power usage over the last 12 years.

Pat yourself on the back. Congratulate our power utilities, too.