Shanghai and Shenzhen stock markets are shaping up as viable rivals to Hong Kong in the race for the biotech IPO crown

- Sixteen pre-profit biotech firms have raised a combined US$4.5 billion in Hong Kong since April 2018, compared with two listings on Nasdaq that raised US$264 million in the same period

- Last year, Shanghai’s regulators allowed drug developers that have yet to earn a revenue or profit to raise funds on the Star market, followed recently by a similar green light on the ChiNext market in Shenzhen

Shanghai and Shenzhen are shaping up as viable destinations for biotech researchers to raise capital, after they drafted or enacted new rules that match Hong Kong’s overture to pre-revenue pharmaceutical and health care start-ups, bankers said.

Last year, Shanghai’s financial regulators allowed drug developers that have yet to earn a revenue or profit to raise funds via initial public offerings (IPOs) on the Science and Technology Innovation Market (Star), followed recently by a similar green light on the ChiNext stock market in Shenzhen. The changes on the two bourses match Hong Kong’s April 2018 listing rule reform, which propelled the local stock exchange to become the world’s second-largest market for biotech IPOs after New York.

“Hong Kong is still positioned as the number one IPO destination for leading Chinese biotech companies, especially those seeking overseas listings, thanks to its mature and stable legal system and abundant international capital,” said Tang Jing, who helps Chinese biotech companies raise capital and pick IPO venues as vice-president of the health care and life science investment banking team at China Renaissance. “However, we saw a change in the dynamics last year, which is speeding up this year due to rapid policy moves.”

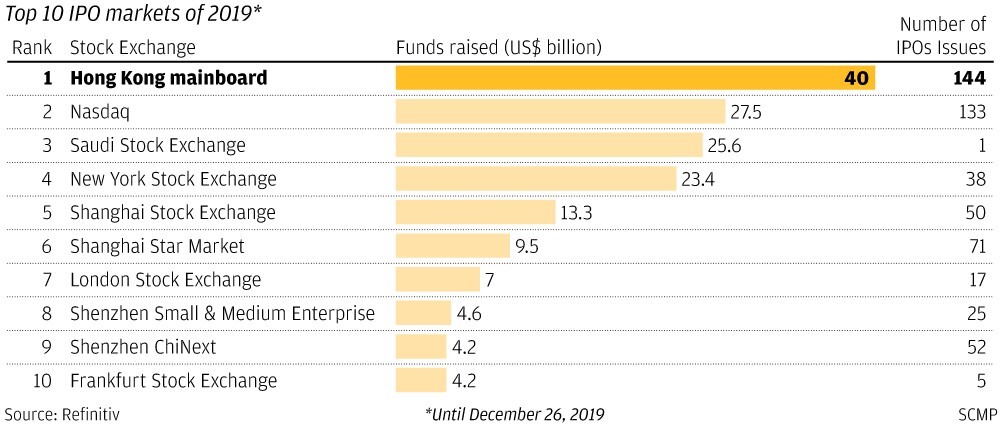

The changes afoot reflect the competition between the three stock exchanges – Hong Kong, Shanghai and Shenzhen – to claim the crown as the go-to destination for Chinese companies. Hong Kong, with US$4.99 trillion in capitalisation as of May 15, is the biggest stand-alone stock market of the three, based on Bloomberg data, surpassing Shanghai’s US$4.94 trillion and Shenzhen’s US$1.07 trillion.

A raft of regulatory differences divide the three markets, not least China’s capital control that constrain IPOs in Shanghai and Shenzhen to raising capital denominated in renminbi. On top of the currency limitation, China’s financial regulators typically require IPO applicants to show several years of profit, while the process of approving stock sales are often subject to capricious policy shifts that may leave companies in the queue for years.