Government life support is the only thing stopping the economy from sliding into another Great Depression

‘The rising spectre of protectionism and the outside risk of outright trade warfare is a deep-rooted threat to the future’

Nobody likes uncertainty, least of all financial markets, so any kernel of optimism must be a welcome treat for global investors, especially when they have an abundance of ready cash to put to work. So the latest prognosis by the International Monetary Fund noting consistently better economic news and a brightening global outlook should be music to investors’ ears.

Except that the IMF’s latest World Economic Outlook (April 2017) seems to ring a discordant note, especially in its title “Gaining Momentum?” The inclusion of the question mark is a big giveaway. It seems the IMF hardly believes its own contention that things are potentially getting better.

To be fair, the IMF has a duty to sound more upbeat as global authorities have tried “every which way and loose” to get the world economy back on its feet again in the past eight years since the global financial crash first hit, using all sorts of monetary creation and fiscal wizardry.

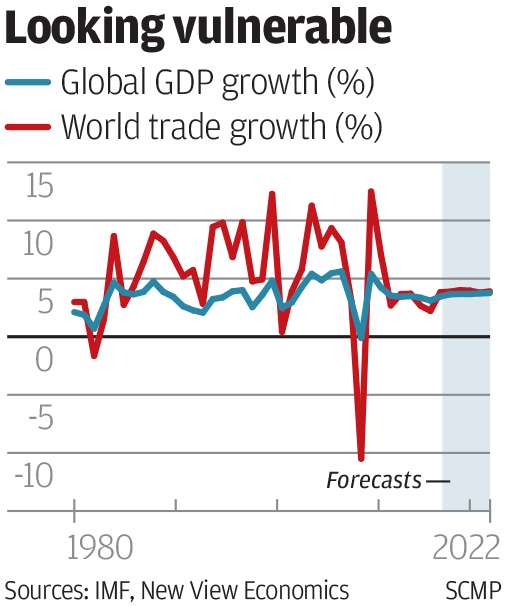

The problem boils down to whether consumers, businesses, investors and governments actually believe the hype and are prepared to invest and spend in a bigger way. The IMF is hoping for a brave new world of global gross domestic product growth picking up to 3.5 per cent this year and 3.6 per cent in 2018 as long as economic confidence continues to build.

In truth, global economic recovery still remains on life support and in a near vegetative state

But it is a “big ask” believing it, especially as the IMF reels out its list of reasons why recovery prospects remain so weak and muted right now. Critically, the IMF points out “significant downside risks continue to cloud the medium term outlook” and these may be intensifying.