Private equity-backed M&A in China stalls as investors put off deals amid trade war

Bankers and deal advisers see US-China trade war put a drag on deals’ completion and purchase price multiples

Mergers and acquisitions in China are likely to slow further in the second half as private equity investors put transactions on hold amid the escalating US-China trade war.

Industry players also say private equity buyers and business owners are beginning to discuss the impact from the US trade tariffs ranging between 10 per cent to 25 per cent on Chinese companies’ gross margins, and their negotiations are increasingly touching on how to split the additional tariff cost in their purchase price multiple discussion.

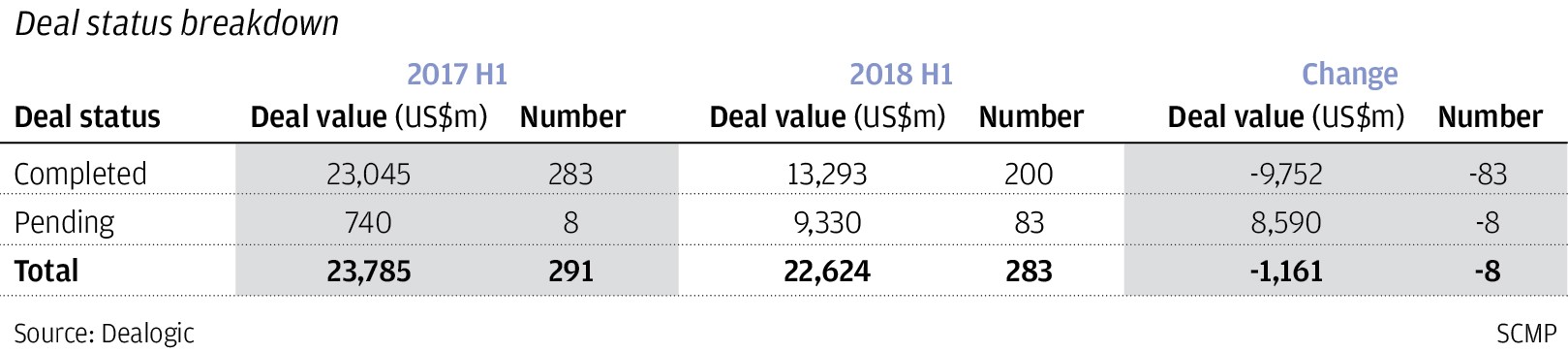

Inbound deal value into China dropped 20 per cent for the first half of 2018 from the second half of 2017, to US$4.91 billion across 206 deals. That figure includes M&A activity from both corporate buyers and private equity and venture capital sponsors, data from Dealogic shows.

Jeffrey Wang, managing director and co-head of BDA Partners’ Shanghai office, which advises on cross-border M&A deals, said in the first half the then escalating trade friction between China and the US had not affected the pace of private equity M&A activity in China, but if the trade war worsens considerably, more deals will get suspended as supply chains get disrupted.

“If trade tensions worsen considerably to the extent that imports affect domestic demand, then it’s conceivable that more deals will get suspended,” said Wang.

Completed China-inbound deals dropped by 29 per cent in the first half of 2018 from a year ago while pending deals rose 10 times, Dealogic data showed.