Stock rally not likely to last

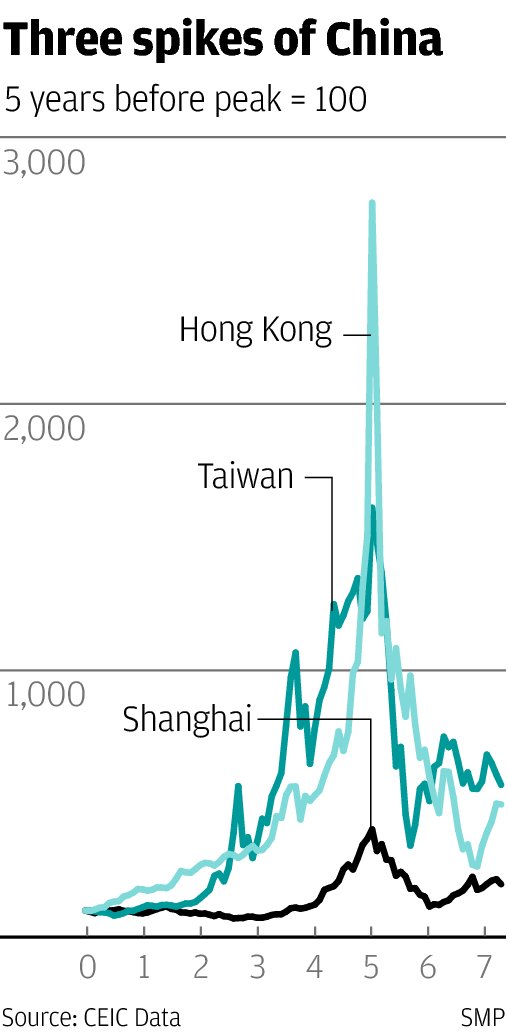

Gather round now, folks, for the story of the three spikes of China. This is a story of two Chinese stock markets that spiked in mad frenzy and a third that would like to but hasn't really got the oomph to do it.

Gather round now, folks, for the story of the three spikes of China. This is a story of two Chinese stock markets that spiked in mad frenzy and a third that would like to but hasn't really got the oomph to do it.

We start with the Hong Kong market in early 1968 with the Hang Seng Index at a value of 63.1 and investors of the opinion that things were actually looking quite good and perhaps a bit of a rally was in order.

Five years later, in February 1973, the Hang Seng Index peaked at 1,775. This was only months before the Yom Kippur war and the start of an energy crisis, which may explain the market's subsequent thundering crash.

A photo taken at the time - I wish I could find it again - showed one long queue of hopefuls, cheques in hand, lined up at a new issue drop box at the Queen's Road entrance of the old Hongkong Bank building. The tail of that queue met the tail of another lined up from a similar drop box near the entrance of St John's Cathedral. The caption underneath read: "O come all ye faithful."

Seventeen years later the Taiwan stock market spiked in much the same way. Over the space of five years the Taiex index rose from the 630 mark to a value of 12,682 in January 1990 and then crashed.

It was not as spectacular a climb as the earlier one in Hong Kong, but it lasted longer and more money went into it.

That bull market was largely fuelled by financial liberalisation and simply ran out of steam when speculators took it too high. It has never since regained the 1990 peak. Taiwan has been made something of a yesterday's story by China's industrial success.

But I can still recall the frenzy in a big Taiwanese brokerage office that I visited one morning in 1990.

The punters were thronged, waiting to hear the tip for the day, and then rushed to the counters with their order slips in hand, almost bowling me over.

Seventeen years later again it was the turn of the Shanghai market to emulate these first two spikes of China.

So now we have talk of Shanghai trying it again with a sudden catch-up run in Hong Kong last week as the Shanghai punters finally recognised that Shanghai listed stocks are much cheaper in Hong Kong than at home.

It certainly took them long enough to see it.

But I take a different view here from Christopher Cheung.

I do not think this rally has the legs to run much further. For one thing, the Shanghai index has never properly represented the mainland's industrial strength and certainly not reflected the more than tenfold rise in gross domestic product over the last 20 years.

Meanwhile, the mainland economy is slowing down; its rust belt industries are in trouble, and liquidity is drying up with money supply growth at near record lows.

No, this is not a bubble.

I think it's more like a last gasp.