MacroscopeWeaker China March trade surplus a blip in long-term trend

The prevailing wisdom is that China’s economic growth is no longer supported by trade.

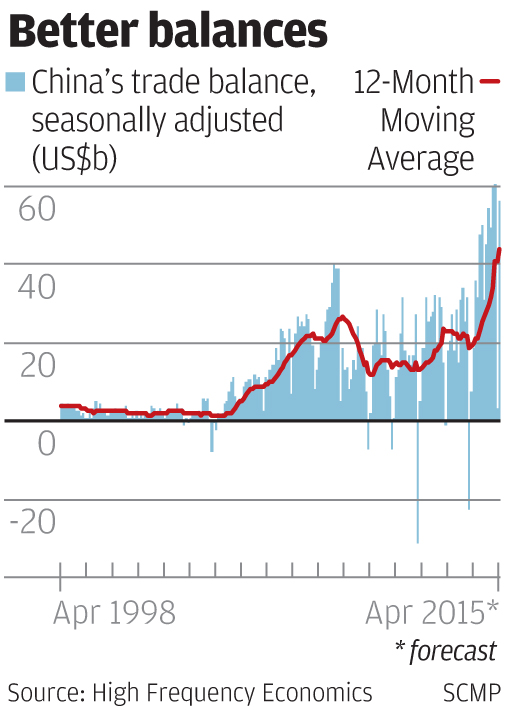

Taking a look at long term charts to see if the contribution of trade to GDP has gone down is the only sensible way to assess this, especially when analysing an emerging economy. The picture is rarely evident in month-to-month changes.

This approach means you can ignore the itsy-bitsy-teeny-weeny trade surplus booked in March - a mere US$3.1 billion (HK$24.2 billion) - as a crazy deviation from a very strong trend. It is pretty certain that the trend is unbroken by this one-off report.

If there was reason to get excited because the trade surplus in March was US$37 billion below its 12-month moving average, shouldn’t there also have been excitement when the February surplus was US$19.6 billion above trend, or when the January surplus was US$26 billion above, or when the December surplus was US$17.9 billion above?

When looking at China’s trade trends, the smallest increment of time that matters is a full calendar quarter. The trade surplus in Q1 was US$123.7 billion, the third biggest ever. The biggest ever trade surplus was in Q4 last year, at US$149.5 billion. And the second biggest ever was in Q3 last year, at US$128.1 billion.

Indeed the trade surplus has been growing faster than GDP. In yuan terms, the trade surplus has increased 16-fold since 2000, while GDP has increased just 3-1/2 times. Since the 2008-09 global economic crisis, the trade surplus has increased 2-1/2 times while GDP has grown barely by half. The trade surplus is increasing as a share of GDP. Therefore trade is adding to GDP growth.