CLP not being reasonable in its view about reasonable returns

Call me lazy if you must for presenting the same chart twice within one month, but it shows you what constitutes reasonable returns in the electricity market and CLP Holdings needs to face the facts here.

Call me lazy if you must for presenting the same chart twice within one month, but it shows you what constitutes reasonable returns in the electricity market and CLP Holdings needs to face the facts here.

Its profits are regulated through a scheme of control that fixes its permitted return to a percentage of its investment in fixed assets. From 1964 to 2008 this figure was set at 13.5 per cent. It was then reduced to 9.9 per cent, and the government is now talking of reducing it further.

{kind=link}

Let us put some context into the word "reasonable". For most people a reasonable return would be what others make on similar investments with some adjustment for whether the particular investment under consideration is more or less risky than others.

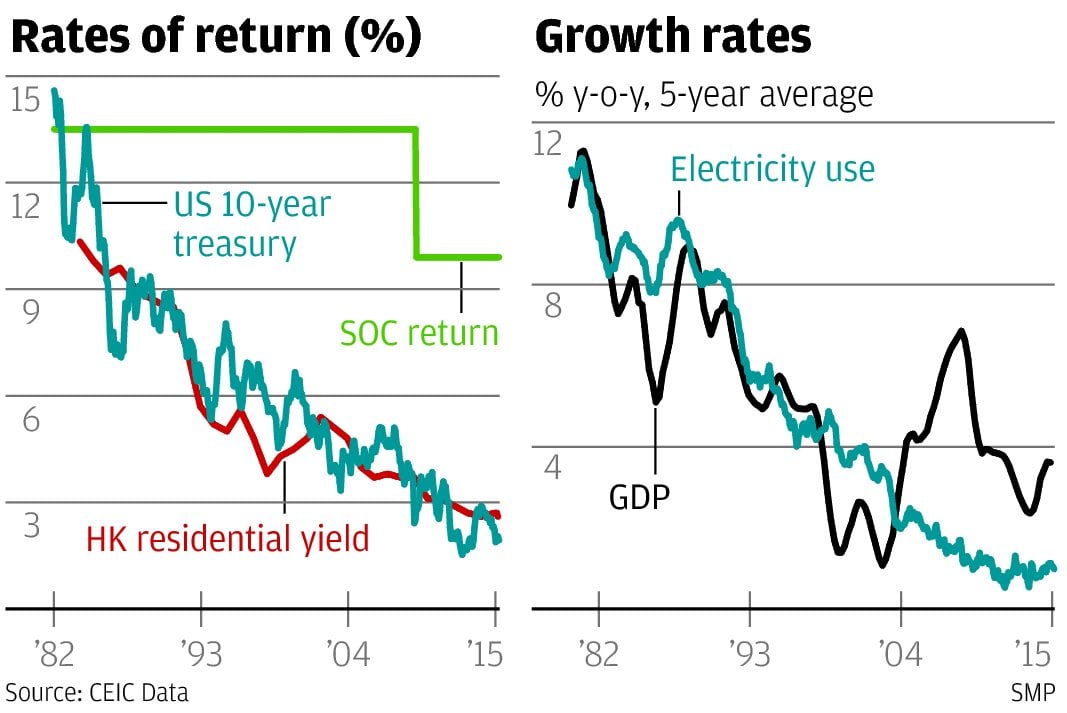

A return rate of 13.5 per cent was about right at the beginning of the 1980s when the benchmark US 10-year treasury showed even higher yields briefly and when yields on investment property in Hong Kong were over 10 per cent.

This is not today's world. As the first chart shows, the 10-year treasury yield runs at about 2 per cent at present and residential property yields in Hong Kong are under 3 per cent. CLP Holdings' permitted return of 9.9 per cent now looks very rich in this context.

Bear in mind also that electricity demand in Hong Kong has historically been about the most risk-free investment that anyone anywhere could make. On that basis the 9.9 per cent looks even richer.

Yes, perhaps, says the CLP brass, but things could turn around tomorrow, you know, and where would we be then?

Where you would be, fellows, is in today's world where you simply do not find such things as fixed percentage returns for multidecade periods. You have an argument here for a floating rate of return, not for putting your hands over your eyes and saying, "Abracadabra, I wish I was back in 1964."

And it won't do to argue that unusually heavy investment should be rewarded with unusually high returns. As the second chart shows, the long-term five-year trend shows electricity consumption growth at barely one per cent a year now, far down from those heady growth rates of 10 per cent plus at the beginning of the 1980s.

Electricity consumption is now growing more slowly than the overall economy. The investment requirements have thus eased. We are getting so efficient in electricity consumption that we could almost paint this town green.

So let us have done with this debate about whether the rate of return should come down. Yes, it should and will come down. This is what you call reasonable.

But if CLP chairman Michael Kadoorie is determined to propose the futile, then I recommend that he tell the sun to rise in the west instead of the east. He has about as much chance.