Taking a punt on the number of Fed rate increases this year

Columnist Jake van der Kamp estimates there will be no more than two rises, meaning the effect on Hong Kong’s housing market will not be great

Buying momentum and prices have continued to rise despite the property stamp duty, an upward interest rate cycle and the government’s determination to boost home supply.

SCMP, April 1

I have a standing bet with our business editor. I say that the United States Federal Reserve Board will raise interest rates at most only twice this year. He says it will be three times or more. Loser owes the winner a bottle of grand cru.

What is more, I say that this is a bet on the crux of our housing problem. Our high home prices are the direct result of low interest rates, not of a housing shortage or of speculators who can be chased away by stamp duties.

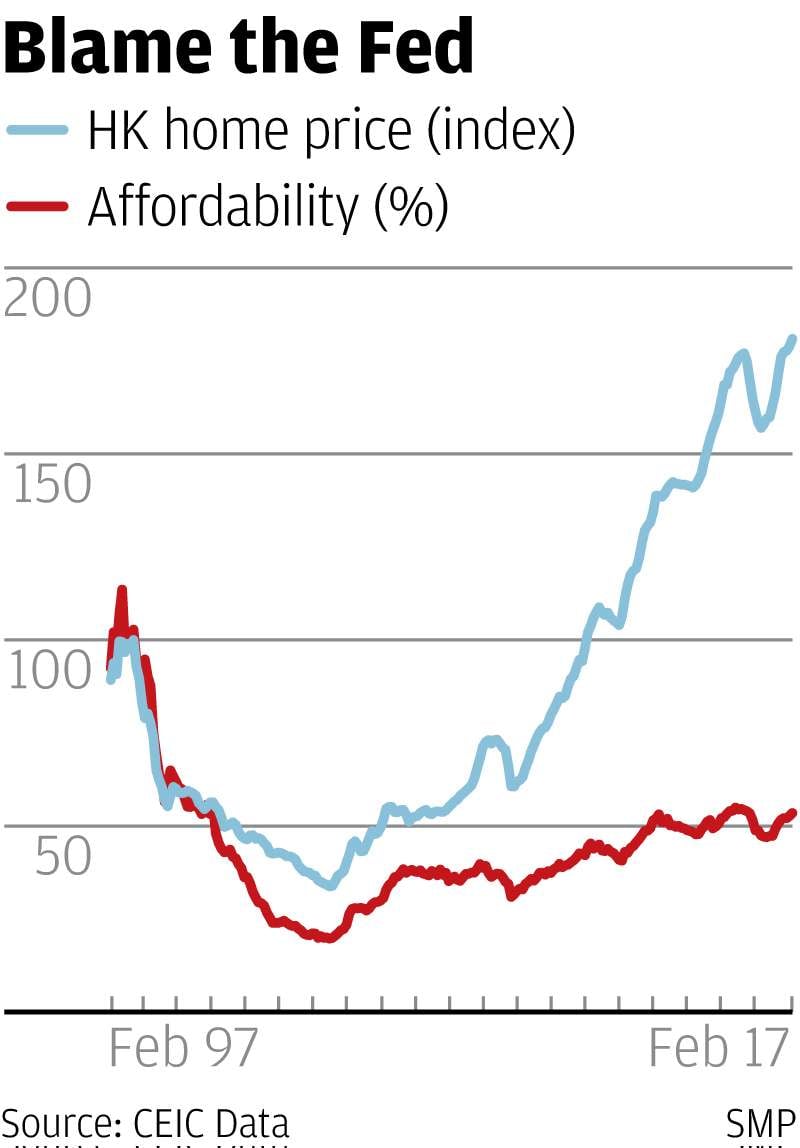

The chart tells the story. Start by reading the scale on the left side as a price index where a value of 100 represents the price of an average small to medium flat in October 1997.

Now look at the blue line. The price of that flat is now 80 per cent higher than at the peak in 1997, more than five times as high as at the bottom in 2003, a frothily boiling property market indeed.

But look at it in a different way. The price of a flat to the vast majority of buyers is not the headline price but the monthly mortgage payment required to own it. The big question is how much of a bite this will take out of the average household income.

We call this measure an affordability ratio and several things go into calculating it, including headline price, down payment, mortgage term, household income and, most critically, the mortgage interest rate. Now read the scale on the chart as being this affordability ratio and what the red line tells you is that the Centaline Property Agency, a big estate agent, says the ratio is now only about 53 per cent, down from more than 100 per cent in 1997. Prices are overstretched, yes, but not yet gone crazy as in 1997.

The difference is all down to mortgage interest rates. They are by far the biggest determinant of mortgage affordability, and ours have been hammered to artificially low levels by our peg to the US dollar and the US Fed’s irresponsible tinkering with the price of the money.

It’s not about a shortage of housing. We don’t have one. With few exceptions, all holders of permanent Hong Kong identity cards live in secure permanent homes with full service facilities.

Those awful subdivided flats are mostly occupied by recent immigrants. I’m sorry for them but our government is not obligated to house everyone who takes a fancy to coming here.

Our difficulty is that our homes are generally small and we want better. But this is a matter of housing aspirations, not of shortages. Convert the Disney park and our fast declining port into housing and we could be well on our way to meeting those aspirations. Our problem is a misuse of land.

The pernicious new stamp duties only make things worse. They have not checked prices and they do not deter foreign speculators.

All the heat is in the small flat segment where foreigners do not play. The stamp duties only ensure that Hong Kong people will be badly hurt when prices go down again.

But it will not happen soon. The Fed runs scared of Wall Street and will keep interest rates down. I still think I will get my bottle of grand cru.