The trade war did not trigger stock market volatility, anxiety over peaking corporate earnings did

- Kerry Craig says the cause of the jitters in global equity markets is not easy to pinpoint, but fears of an easing in corporate earnings growth is a big factor

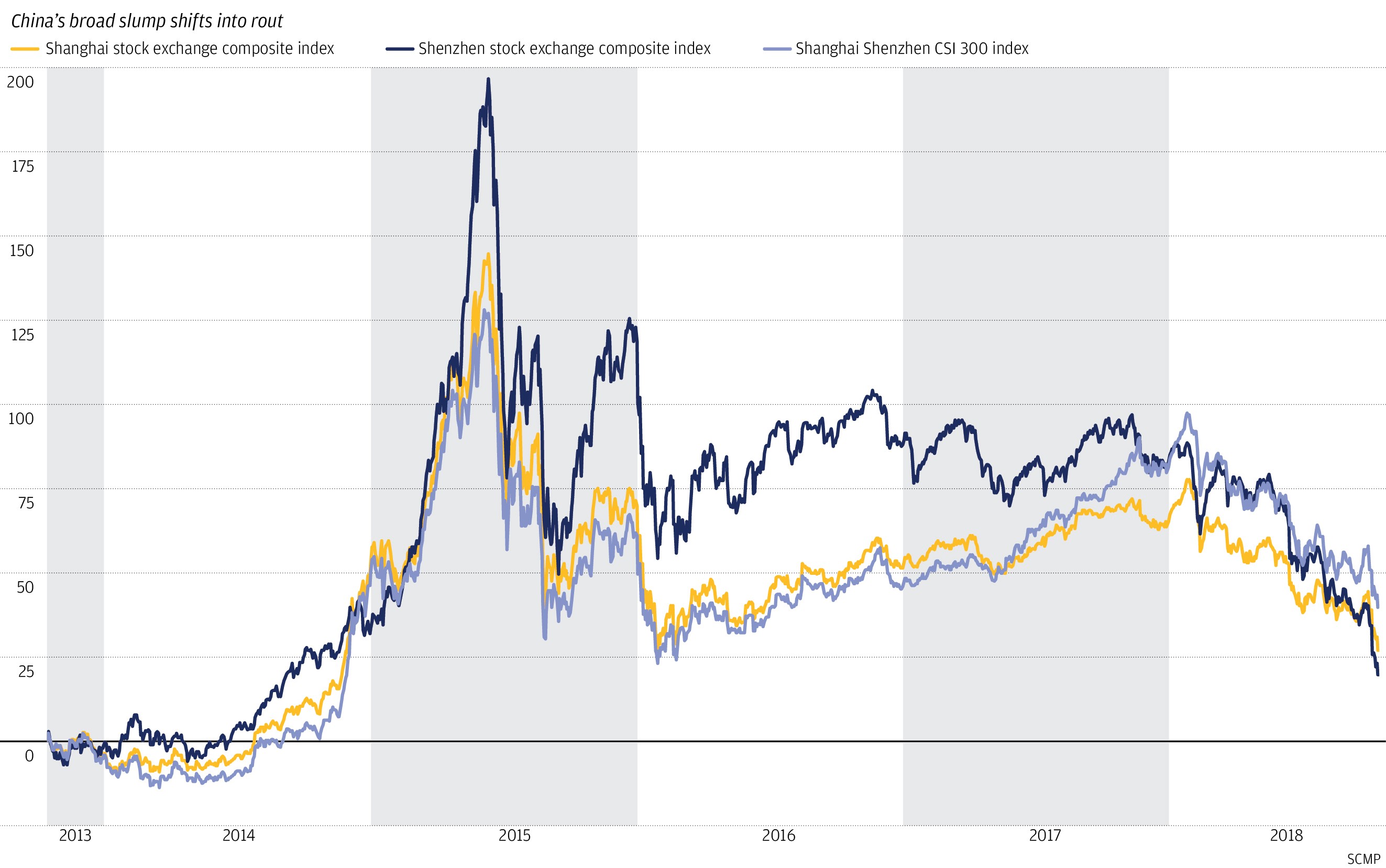

- The sell-off in Asian equities is an opportunity for long-term investors

The brutal sell-off has tested investors’ resolve, challenging the durability of the nine-year-old bull market. Is this correction the beginning of something more sinister – a bear market? Or can equities recover from the overload of anxiety and macroeconomic risks to rally?

The spike in equity market volatility during October is troubling because it’s been difficult to identify a specific cause. The situation is much like a television medical drama in which the patient presents a multitude of seemingly unrelated symptoms, leaving doctors searching for the right diagnosis.

Watch: The origins and impact of the US-China trade war

So why are markets suddenly more concerned with these factors? The answer is earnings. Against the overhang of increasingly worrying macro headwinds, US corporate earnings strength has proven to be an effective windbreak. Investors may have felt they could deal with all the risks as long as corporate America was still delivering on the promise of earnings. Even here the current US earnings season doesn’t appear to be a big disappointment, on paper at least.

At the time of writing, 58 per cent of US companies by market cap have reported their third-quarter results and 79 per cent are beating analysts’ expectations for earnings growth. Only 46 per cent have beaten revenue expectations, but even this in line with the average level of expectation beatings since 2012.

The anxiety stems not from the results themselves, but whether they are the peak.

Market corrections happen frequently and should be expected. There have been two this year in the S&P 500 – a 6 per cent drop in early February and the more recent 9 per cent drop from the September peak. But not every 5 or 10 per cent tumble leads to the market falling flat on its face.

Bear markets are the result of a much more serious illness, such as a recession. Recessions have been a factor in eight of the 10 bear markets since the S&P 500 began back in 1926.

This isn’t the beginning of the end for equity markets, but it is a timely reminder about rebalancing and understanding risk. Many events are likely to weigh on markets for the rest of this year and into the next, and it will be impossible to avoid volatility in the future. Although it requires vigilance, volatility can create opportunity. This year’s sell-off in Asian equities has created more value in developed markets and therefore more potential upside.

Historically buying at today’s valuation has led to an average of 20 per cent returns over the subsequent 12 months. Although every cycle is different, market turbulence often offers attractive opportunities to long-term investors.

Kerry Craig is a global market strategist at JP Morgan Asset Management