Why US-China supply chain decoupling will be more of a whimper than a bang

- While China managed to keep export volumes stable by diversifying to other trading partners, the US’ overall trade balance has deteriorated

- Some degree of economic decoupling is under way, but it’s unlikely that a large number of American firms will cut China out of their supply chains

In a recent interview, Trump railed against “stupid supply chains that are all over the world”, further threatening to “cut off the whole relationship” with China and rejecting the notion that undoing the extensive links between the two largest economies comes with any trade-offs.

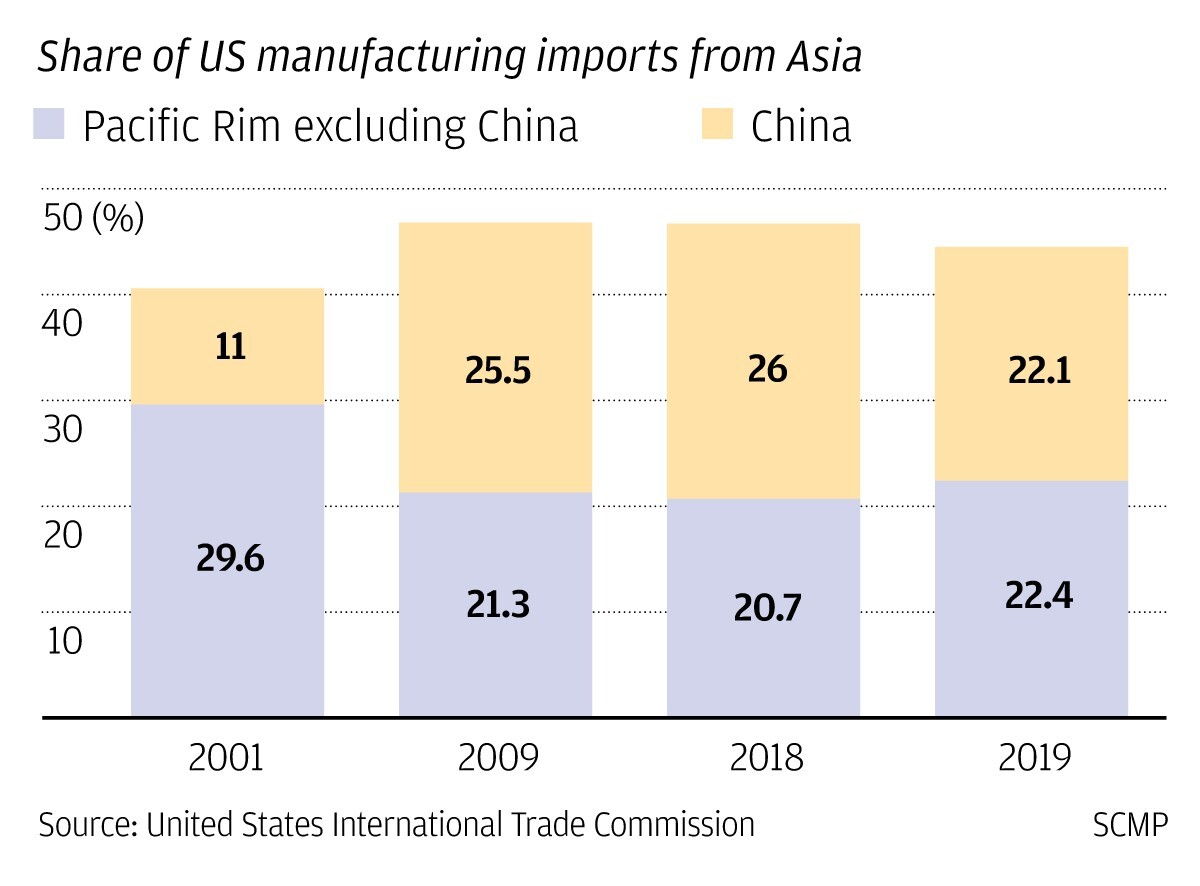

Over the past two decades, US manufacturing imports from the Pacific Rim region – East Asia, Association of Southeast Asian Nations, Australia, New Zealand and Papua New Guinea – consistently hovered at around 40 to 45 per cent of the total. However, the composition of trade partners within the region has shifted dramatically along with the rise of China.

In 2001, having just joined the World Trade Organisation and having recently emerged from the Asian financial crisis relatively unscathed, China’s processing trade took off. At this inflection point, China accounted for only a quarter of US manufacturing imports from Asia, with three-quarters coming from the rest of Asia, and Japan as the major source.

By 2009, amid the global financial crisis, China became firmly established as the assembly plant of the world and accounted for most of Asia’s manufacturing exports to the United States. That pattern largely held for the following decade through to 2018.

Is Donald Trump’s trade war making China change?

But the US was unable to make up the entirety of the decline in China’s share, resulting in a US$39 billion drop in overall manufacturing imports last year.

01:41

A year of the US-China trade war

Elsewhere, we have analysed the impact of the protective tariffs on US and Chinese trade balances and their global partners.

In contrast, America’s underlying overall trade balance and manufacturing prowess paradoxically deteriorated.

While the extent of future decoupling is the subject of much speculation, there are reasons to believe that bolder predictions may be overdone.

First, transshipment and tariff-dodging adjustments to the location of assembly processes result in misleading accounting of the US-China trade data. These practices can cause China-origin merchandise to be recorded as arriving from intermediary partners such as Vietnam, thereby exaggerating the degree of decoupling.

Don’t hold your breath for a dramatic Asean pushback against China

Second, and more fundamental, supply-chain restructuring mandated by politics and security runs contrary to the powerful economic forces of cost pressures and comparative advantage, and businesses will resist these moves.

03:05

Inside China’s ‘shoe capital’: the Jinjiang brands running toward global markets

Third, any significant restructuring of trade networks will take years, not months, regardless of whether it is brought about by politics or market forces.

The predicted mass exodus of US multinationals from China is not yet reflected in the data: an American Chamber of Commerce survey conducted in May found that, in the midst of the pandemic, just 2 per cent of respondents are considering leaving the Chinese market in the next three to five years, and a mere 4 per cent are considering relocating some or all manufacturing out of China.

Much will depend on the persistence of a US protectionist strategy following the upcoming November elections.

Between Trump and Biden, China is likely to prefer the devil it knows

Foreign firms seeking to expand exports to markets outside China, however, will be more open to investing elsewhere to minimise geopolitical risks or for cost advantages. This is true even for Chinese firms, one example being Hisense’s decision to invest in Mexico to serve North American markets.

Though the winds of change are surely blowing, a great deal of inertia exists to maintain something resembling the status quo in US-China trade relations, which ought to temper fears over the more apocalyptic scenarios.

Yukon Huang is a senior fellow at the Carnegie Endowment for International Peace. He is author of Cracking the China Conundrum: Why Conventional Economic Wisdom Is Wrong.

Jeremy Smith is a junior fellow at the Carnegie Endowment for International Peace