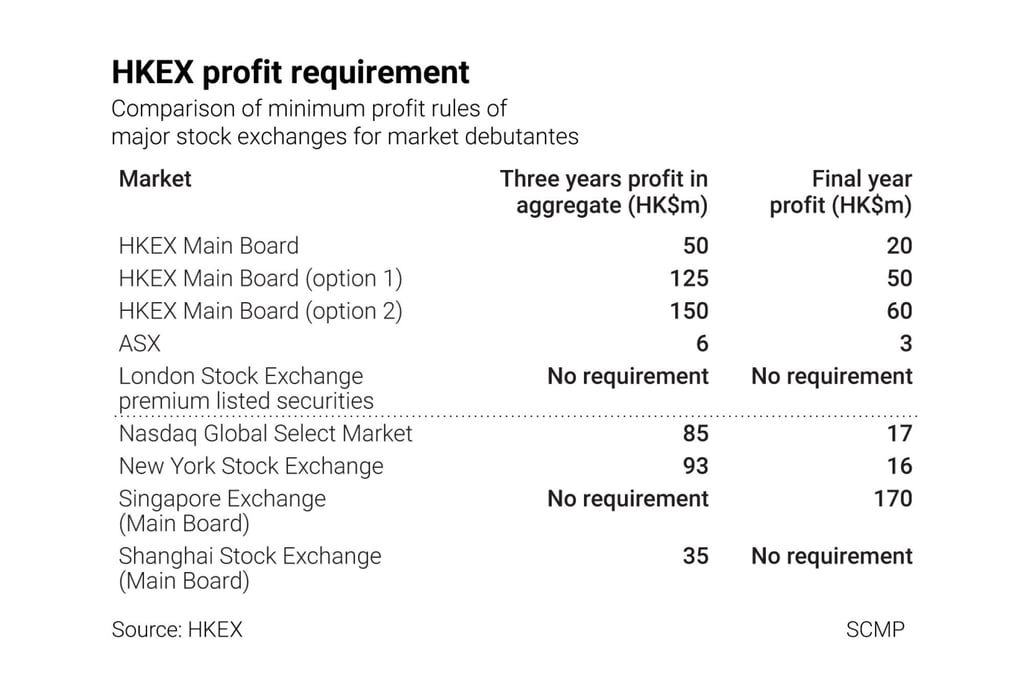

Why Hong Kong’s stock exchange should not raise the profit requirement for listing on its main board

- Neither the high P/E ratio of listing applicants nor the existence of ‘shell’ companies justifies a move that could shut out many small-cap firms from a fundraising platform

- Instead, to support these companies, the exchange should consider lowering or even removing the profit requirement

The exchange may be exaggerating the importance of historical P/E ratios. A historical P/E ratio derived from the historical profit figure is only one factor among many in investment decision-making. An issuer’s prospects are more important to the investment decision than historical P/E ratios. Therefore, drawing an arbitrary line on historical profit is of limited use, and raising the level of this arbitrary line is not an improvement.

Many small-cap, potential issuers would have wanted to list at a lower P/E ratio. If they had been successful, and with more of these small-cap issuers listed under a lower market capitalisation requirement, we would not have seen what HKEX notes is “an increase in listing applications from small-cap issuers that marginally met the profit requirement but had relatively high historical P/E ratios”. In some cases, companies have been forced into this position by the regulatory change of 2018.