Jake van der Kamp is a native of the Netherlands, a Canadian citizen, and a longtime Hong Kong resident.

Beijing is expected to maintain a tight grip on capital outflows despite foreign exchange reserves rising for a fifth straight month in June, analysts said.

SCMP, July 11

Advertisement

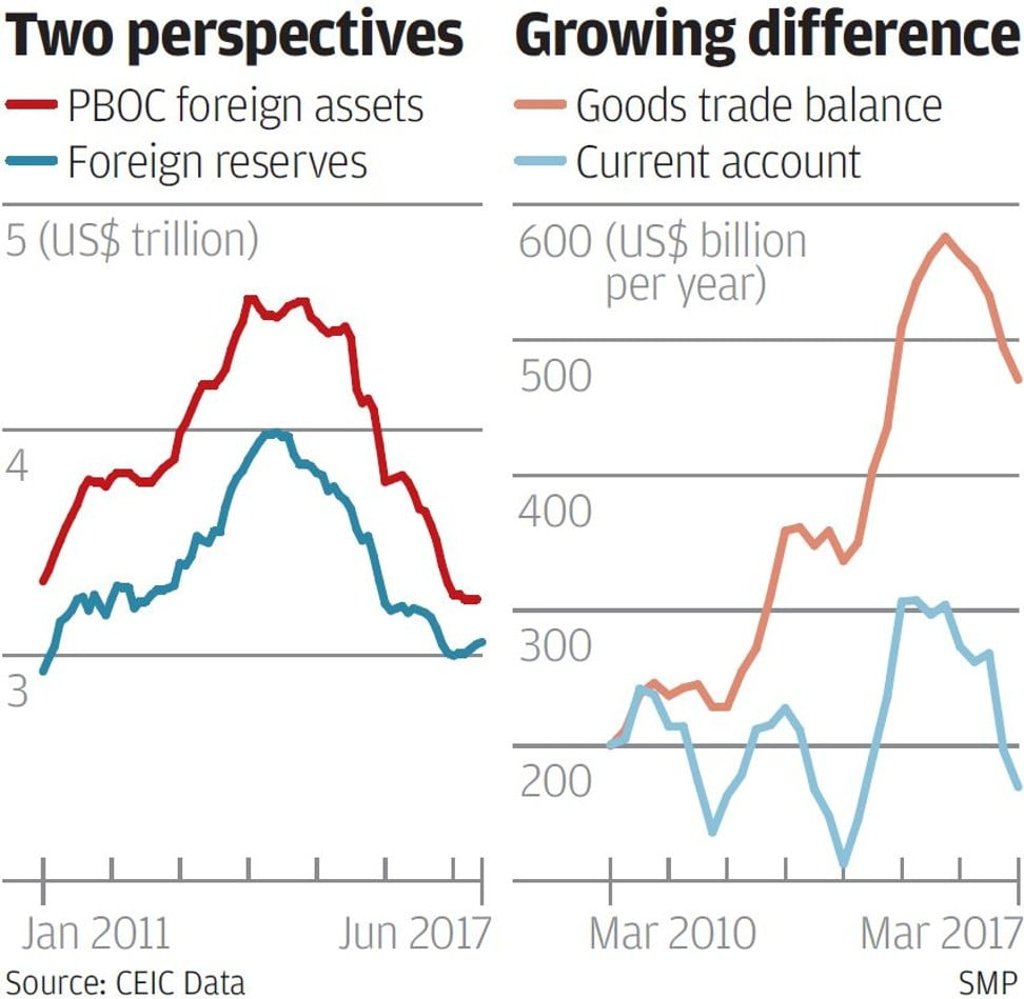

Here is a little secret about how the People’s Bank of China treats foreign reserves at home in its own books.

It calls them foreign assets, it expresses them only in yuan and not in US dollar terms as it does the separate foreign reserves entry and, most of all, it shows them at the original cost of acquisition, not at current market values as it does for foreign reserves.

Advertisement

If it had shown them at current market value, then at the height of their build-up in mid-2015, the PBOC would also have shown an unrealised currency translation loss of about US$760 billion, or about 200 times its own capital.