What’s the future of sustainability in Asia?

A rising pool of money is chasing better ESG practices. Governments are driving the transition to low-carbon economies.

[Sponsored Article]

In Asia, attitudes toward sustainable investing have changed radically in just a few years. Much of this shift started as top- down driven. Now a ground-up narrative is fast developing as private and institutional money chases better ESG disclosures and practices.

Top-down drive gaining traction

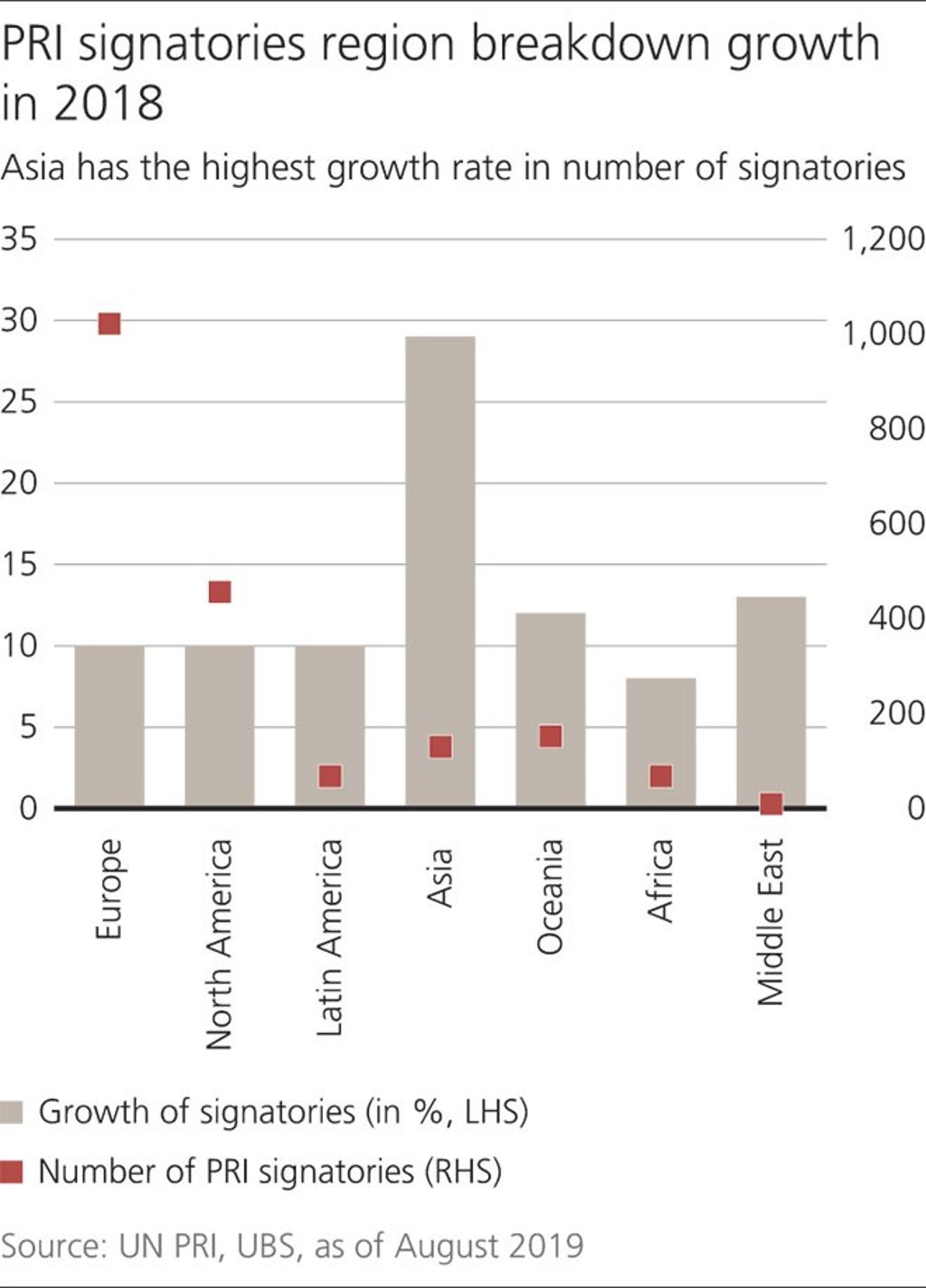

Sustainable investing (SI) has been growing across Asia, with over USD 10trn worth of assets under management signed up to the UN Principles for Responsible Investing in the past three years (2016–2019). The rise of SI in the region has been driven top-down by state asset owners and regulators. A key reason is that Asian governments now view SI as compatible with their policies to address the growth risks from climate change, the transition to a low-carbon world, inadequate infrastructure, shrinking labor forces and growing resource shortages. Asia also now has eight stock exchanges with mandatory ESG reporting, more than any other region in the world, and China, the Philippines and Indonesia plan to join the list next year.

Financing Asia’s sustainability challenges

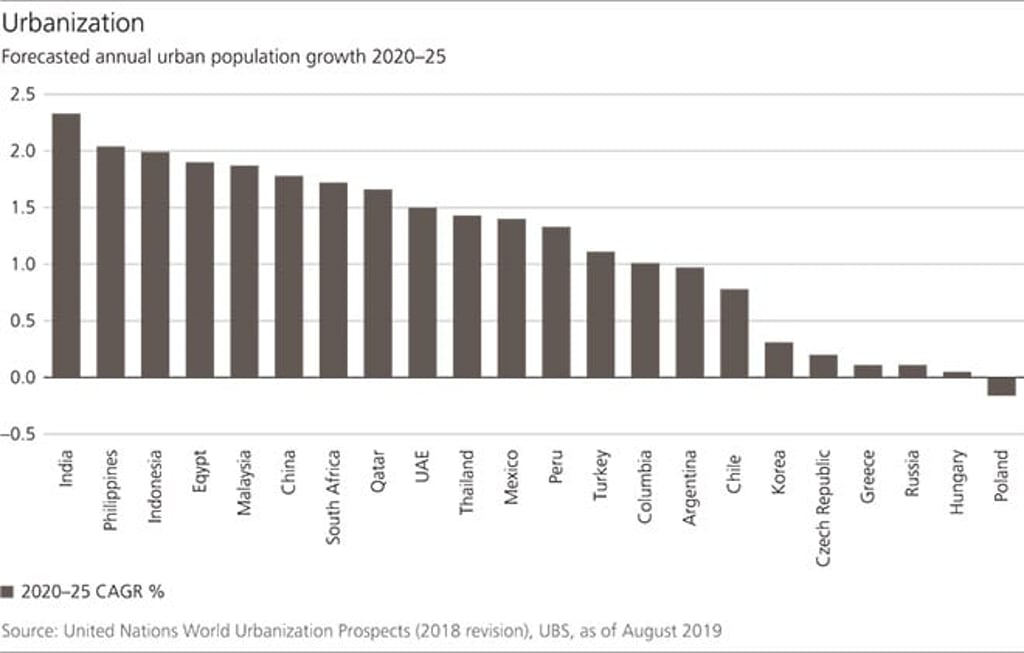

Cities in China and India are forecast by the UN to receive 181m and 113m urban migrants, respectively, from 2015 to 2025. Asia is currently home to 22 of the 33 global megacities (cities above 10m) and will add nine more by 2030. Rapid urbanization and income growth depletes key resources, absorbs agricultural land and expands carbon footprints.

The issue of how to sustain a growing, urbanizing population without further harming the ecosystem is intensifying sharply. Climate change is an acute risk for Asia as most of its economic activity and megacities are on the coast or lie along river deltas. Inadequate attention to climate change risk could cost the region at least USD 2.8trn, based on an estimated 9% hit to regional GDP as a result of rising sea levels under the RCP 8.5 climate scenario.

The Chinese government has sought to achieve greater efficiencies in resource consumption, particularly energy. It has spurred the creation of smart cities, smart grids and other smart technologies, and the roll-out of 5G networks in several Asian countries in the next couple of years, should catalyze these developments. China is also leading the world in developing low-emission sectors like green energy and electric vehicles. Funding the growth of these sectors has produced the world’s second largest green bond market and has accelerated the development of green finance hubs in Hong Kong and Singapore.

In Japan, aging demographics, a shrinking labor force and low capital returns have necessitated a new corporate culture that encourages efficiencies. This has prompted a government-led drive to improve corporate stewardship and governance, and has also led to a boom in SI initially driven by Japan’s JPY 160trn Government Pension Investment Fund.

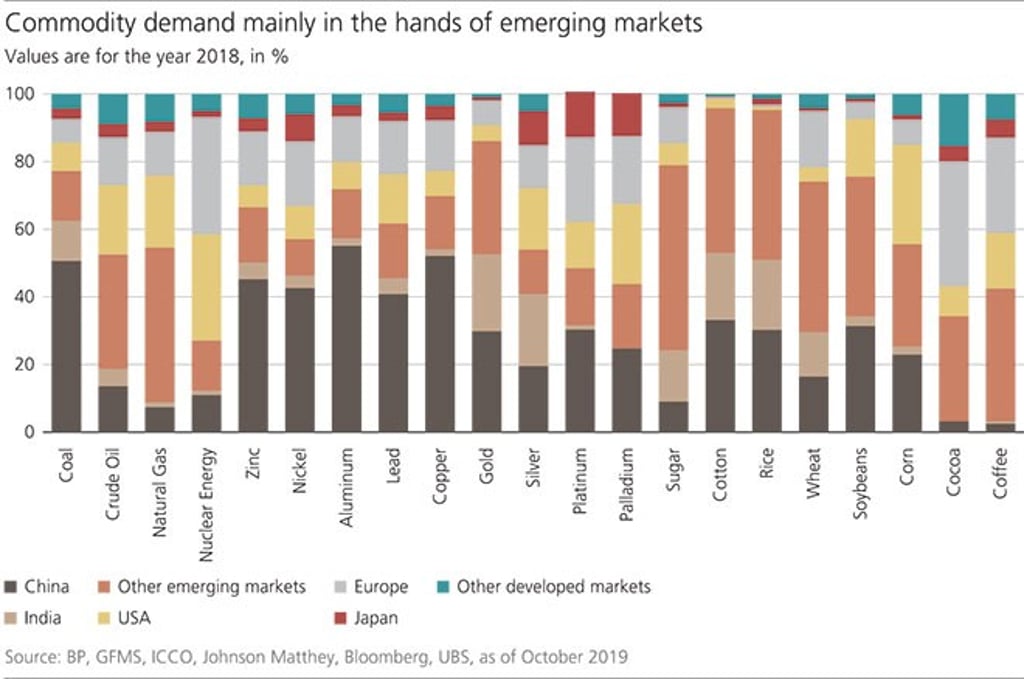

The focus on SI will also train the spotlight on the carbon and environmental footprint of the commodity sector, a key contributor of both GDP and greenhouse gas emissions in the region. ESG concerns are combining with major technological advances to disrupt commodity markets, especially in coal and crude palm oil. This poses significant risk to those impacted, making it critical that Asia jumpstarts its plans to diversify its economies and build business models that are resilient in the transition to a low-carbon world.

From laggard to global leader

These developments are resulting in the rapid growth of sustainable investing in Asia from a low base, and with it the scope and scale of local SI products is improving. UBS advises engaging in SI through individual asset classes and/or by adopting a multi-asset portfolio approach. Investors can also consider sustainability linked themes such as the UBS Long Term Investment series, green bonds, Asia ex-Japan/ Japan ESG leaders, Asian smart cities, smart mobility or select 5G themes. Impact investing also offers a clear link between investment and having a measurable social and/or environmental impact through private equity or direct investment.