When Fit-Out Costs Bite, Location Strategy Matters More Than Ever — West Kowloon Shows Why

By Tom Gaffney, Head of Leasing, Asia Pacific, CBRE; Ada Fung, Chief Operating Officer, Advisory Services, Hong Kong, CBRE; and Ada Choi, Head of Research, Asia Pacific, CBRE

[The content of this article has been produced by our advertising partner.]

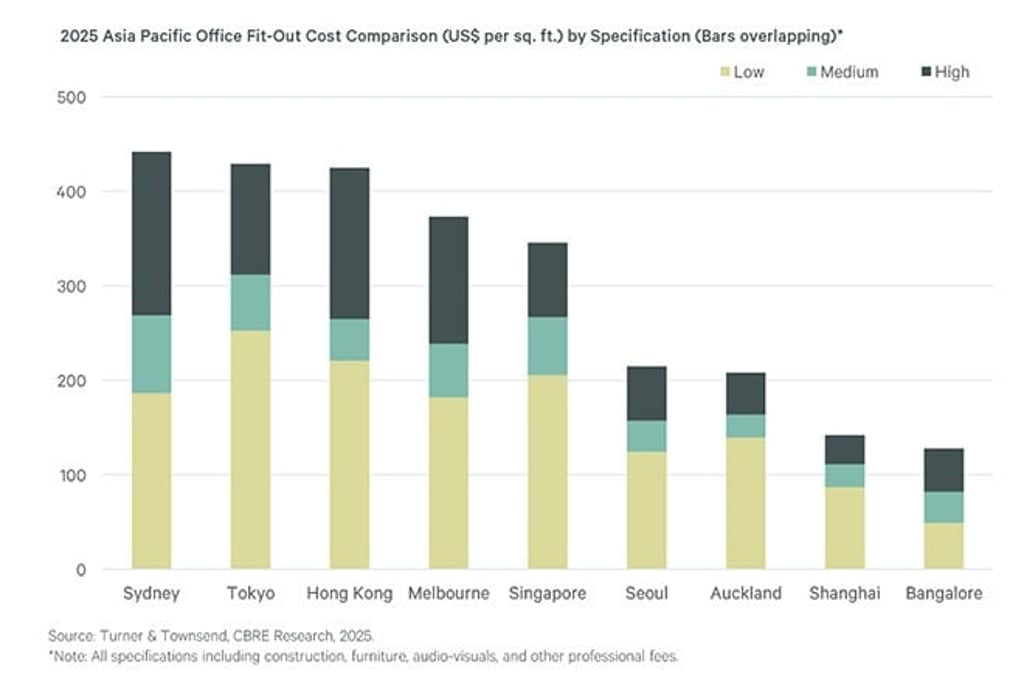

Across the Asia Pacific region, the economics of office occupancy have changed materially. Fit-out costs in Sydney, Tokyo, Hong Kong, and Singapore have surged past US$270 per square foot at mid-specification. Grade A rents are rising in most markets outside mainland China as quality supply tightens. Meanwhile, competition for skilled talent is at its most intense since 2019, with regional unemployment at just 4.7%. The decisions occupiers make about where to locate — and on what terms — now carry consequences that extend well beyond the balance sheet.

Given this backdrop, it is no wonder that West Kowloon has emerged as one of the addresses of choice for institutions expanding or consolidating their Hong Kong presence. Across wealth management, investment banking, and professional services, new long-term leasing commitments are reshaping the district's identity from an ambitious development project into a functioning financial hub.

Rising material costs, persistent labour shortages, and geopolitical-driven commodity volatility have pushed construction cost inflation to structurally elevated levels across the region's mature markets. Capital expenditure management has become a board-level priority given these macroeconomic factors, as occupiers now face a tightening gap between budget flexibility and the expectation of delivering high-quality, tech-enabled, sustainable workplaces.

For occupiers in Sydney, Singapore, Tokyo, and Hong Kong, this is not a temporary spike to be waited out. One increasingly compelling mitigation is leasing brand-new Grade A stock where landlords offer fit-out contributions or turnkey solutions, where a single contractor manages design, procurement and construction. This reduces upfront outlay, compresses delivery timelines, and avoids cost overruns. West Kowloon's new development pipeline fits this bill perfectly.

As regional unemployment reaches its lowest level since 2019, competition for office-based talent is expected to intensify further through 2030. Finance occupiers across Hong Kong and Singapore are responding by doubling down on location as a talent attraction and retention tool, concentrating in core, amenity-rich environments.

The data is unambiguous: 88% of companies prefer CBD or CBD-fringe locations specifically because they make the commute easy via mass transit. This is not merely a convenience preference — it is a strategic constraint. In Tokyo, where CBD vacancy has fallen below 1%, pre-commitment to new buildings is now a necessity, not an option. In Singapore, a shortage of new supply through 2028 is pushing occupiers toward shorter-term renewals while they await the next wave of quality stock.

West Kowloon's answer to the commute imperative is exceptional by any regional standard. The district hosts Hong Kong's only High-Speed Rail station and connects to the Airport Express, directly accessing 110 mainland China destinations and reaching over 520 million people in the region, including 80 million in the Greater Bay Area (GBA). This geographical proximity is not only compelling for talent to consider, for wealth managers and private banks whose client relationships straddle Shenzhen, Guangzhou, and other international financial centres, this connectivity is also a business model advantage built into the postcode.

Locking In Quality Before the Window Closes

New quality supply across Asia Pacific is set to tighten over the medium term, as developers struggle to justify new projects in the face of elevated construction costs. The gap between core CBD vacancy and decentralised submarkets is widening across the region, with tenants displaying a clear preference for prime locations. In Hong Kong, tenants are increasingly willing to consider West Kowloon, where high-quality new projects are available at a fraction of the rents on offer in Central.

The regional comparison makes the timing sharper still. Mumbai's Grade A rents in Bandra Kurla Complex are projected to grow by an additional 40% over the next three years. Singapore faces accelerating rental growth with limited new supply expected through 2028. Tokyo CBD vacancy — already below 1% — leaves almost no room for last-minute decisions. Against this backdrop, Hong Kong's current pricing, particularly in West Kowloon, stands out as exceptional value in a region where quality is increasingly scarce.

Managed Solutions as a Turnkey Alternative for MNCs with Tighter Budget

With office fit out and construction costs continuing to rise across the region, occupiers are finding it increasingly challenging to manage real estate capital expenditure (CapEx). Recent geopolitical developments in the Middle East have added an additional layer of uncertainty, prompting occupiers to remain vigilant and carefully assess potential cost pressures. As a result, demand for fully fitted and managed solutions is expected to strengthen, especially among occupiers with limited CapEx budgets.

Why Infrastructure Decides Everything

Infrastructure-led decentralisation is not a new real estate strategy, but the evidence on what works is now clear. Infrastructure is the single determining variable in moving occupiers from established CBDs to emerging ones. Without it, even well-intentioned government-backed clusters fail to achieve critical mass.

Amid new occupier needs, West Kowloon is a great example that marks a confluence of what is required as a new CBD in Asia. In addition to a robust web of transportation networks, the West Kowloon Cultural District — encompassing the M+, the Hong Kong Palace Museum, and Xiqu Centre — provides the experiential layer that has become increasingly important to occupier decisions, and that resonates strongly with the mainland Chinese and international ultra-high-net-worth clients who define the target market for many of the district's anchor tenants.