Source:

https://scmp.com/business/banking-finance/article/2083809/employees-win-providers-lose-hong-kong-mpfs-low-fee-reform Banking & Finance

Employees win, providers lose in Hong Kong MPF’s low-fee reform

Introduction of a compulsory Default Investment Strategy fund could force out small providers by cutting income from fees by up to 40 per cent

The reform, which comes into effect on April 1, represents the biggest shake-up of the MPF scheme since its inception in 2000. Photo: AFP

Hong Kong’s Mandatory Provident Fund market may see more consolidation as reforms taking effect on April 1 slash income from fees by up to 40 per cent, forcing smaller providers out of the market.

From Saturday onwards, all 18 MPF providers are required to introduce a Default Investment Strategy fund, which has a management fee capped at 0.95 per cent. That compares with the 1.56 per cent average fee across the 435 MPF investment funds.

The reform will benefit the 2.8 million members under the MPF, Hong Kong’s compulsory retirement pension scheme, as they will pay less if they choose to shift their investment to the new fund. The HK$8.2 billion (US$1.06 billion) in assets of the 600,000 employees who do not choose how to invest their MPF contributions will be automatically moved into the default fund.

The other members also have the option of diverting their contributions to the default fund, putting additional pressure on other funds to cut their fees.

It is the largest shake-up of the MPF scheme since it was launched in 2000 and is intended to address years of fierce criticism about high management fees and low returns.

“With a total fee cap of 0.95 per cent, as opposed to the current average fee of 1.73 per cent for other mixed-asset MPF products, the introduction of DIS is a step in the right direction because it will help MPF members save more over time,” said Jackson Loi, managing director for institutional business of Vanguard Hong Kong.

“Vanguard supports the MPF reforms, including the DIS initiative, and we believe MPF members will be the biggest winners.”

“The MPF’s [default fund] reform will definitely cut fee income for the providers. Some providers have already opted to leave the market and some of the smallest players may follow,” said Chan Kin-por, lawmaker for the insurance sector.

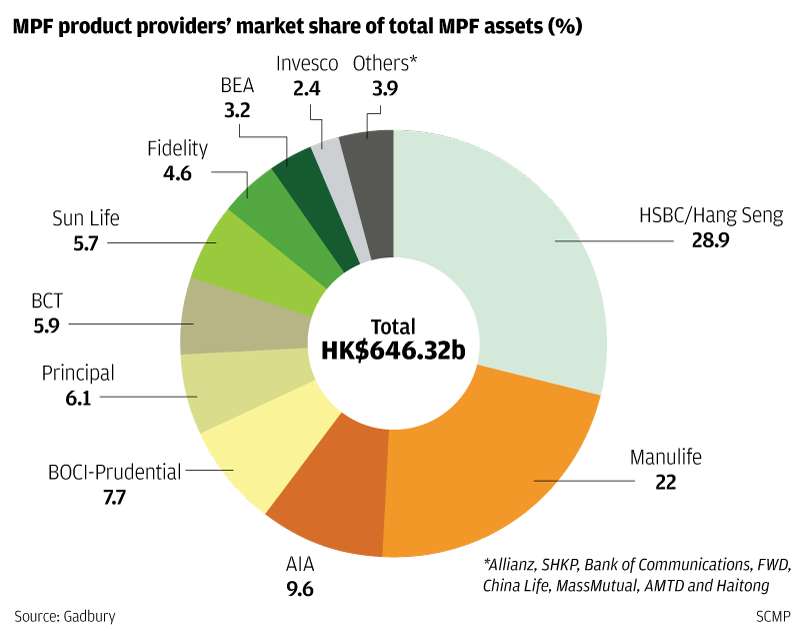

The top five MPF providers have a 75 per cent market share between them while the top 10 have 96 per cent. This leaves the eight smallest players to share 4 per cent of the pie while the smallest provider, Haitong, has just 0.07 per cent, according to Gadbury, which tracks the performance of the MPF scheme.

The impact of the reform will depend very much on whether the 2.8 million members decide to shift some or all of their HK$650 billion contributions to enjoy the low fees offered by the default fund.

In overseas markets, up to 80 per cent of the members chose to put their new contributions into the default fund as it provided a simple investment solution, Darren McShane, former chief regulation and policy officer and executive director of the MPF Authority, said in an interview before his retirement last week.

Darren McShane, outgoing executive director of the MPFA, expects 30 to 40 per cent of MPF members to opt for the default fund. Photo: Jonathan Wong

McShane said he personally invested in stock funds, also the most popular choice in Hong Kong’s MPF scheme.

“Many Hong Kong members like to make their own investment choice. Some prefer to invest in funds that charge a higher fee and offer a higher return. At the end of the day, the fee is only one of the many considerations for members to choose how to invest their MPF,” he said.

Kenrick Chung Kin-keung, director of MPF business development at Convoy Financial, said members would spend two to three years monitoring the performance of the default funds before deciding whether to shift their MPF contribution.

“If the default funds could achieve a similar or better performance than the other MPF funds in two to three years’ time, people would wonder why they should pay more for other investment funds,” he said.

Stephen Fung, chief executive of AIA MPF, says the default fund scheme is tailor-made for those not interested in managing their MPF investments. Photo: Handout

“It depends on how in-depth investor education provided by MPF companies is,” said Terry Pan, chief executive for Greater China, Korea and Singapore at Invesco. “For Invesco, the majority of our MPF members know their MPF investments well and, as a result, only a small proportion of them, about 3.5 per cent, haven’t made any investment decision for their contribution accounts.”

Stephen Fung Yu-kay, chief executive of AIA’s MPF scheme, said the default fund scheme was tailor-made for those not interested in managing their MPF investments.

“Members should note that the default fund is made up of two mixed-assets funds, which may involve higher risk than that of existing default funds. The returns may vary with market performance and investment returns are not guaranteed,” Fung added.