SCMP Graphics. Source: Gadbury

“We will proactively follow up various measures to optimise the MPF system.”

Chief Executive Carrie Lam Cheng Yuet-ngor

Election manifesto

One of the strangest things about the structure of Hong Kong’s Mandatory Provident Fund is that your employer, not you, picks the fund manager who will manage your MPF investments.

Think about this. Your employer has no interest in how well it is invested. He pays in his monthly MPF contribution and this is the last he sees of it. Now it’s all yours but you cannot invest it yourself and you have no say in who is chosen to do it.

Thus if they charge an extraordinarily high fee for managing your MPF money, he is unlikely to say anything about it. Why should he? He would do himself no favours.

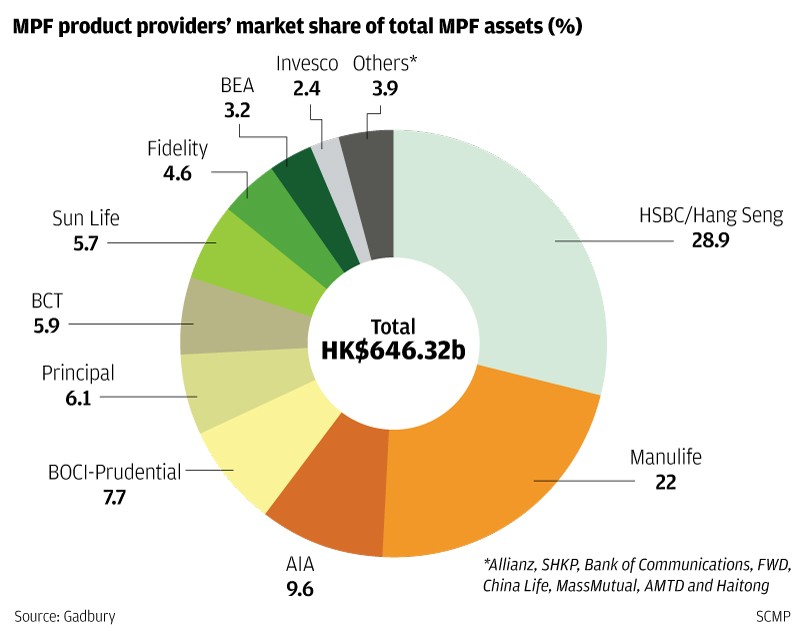

This is why you hear no complaints from employers about the average MPF management fee of 1.56 per cent a year.

It does not seem very high, but it is. Over the course of your career it could easily result in your losing half of your potential retirement benefits. That 1.56 per cent just keeps draining away your wealth, year after year. Remember that it does not include brokerage commissions, stock exchange levies and other such costs. The real hit is higher than 1.56 per cent.

And don’t let your MPF manager tell you that he does more work. Vanguard has marketing expenses that MPF managers do not incur and must stand ready to return you your money at any time.

Your MPF manager does not face this risk. You cannot lay your hands on the money until you retire and he knows it.

Every month on schedule, he gets his contributions and can tell his assistant: “Stick it in our usual line. Where am I having lunch today?”

It gets even worse. This ridiculous system of employer choice means you will have as many MPF plans as you have employers over your working career, all of them requiring separate filing and reporting. Instead of one unified plan carried from one employer to another, you have an administrative nightmare.

Our bureaucrats know it, and so they made a change. You can apply to have your own plan for your own contributions to the MPF, but you must apply every year if you want to put your employer’s contribution in it and it can only be for that year’s contribution.

They called this a reform. It’s beyond laughter.

Why was it all done this absurd way?

It all hangs, officially at least, on this thing they call the “offset”, which has been much in the news recently.

And they argue, at the behest of the fund management cabal, that to give you the choice of fund manager would encourage you to pick a risky one because if he wiped out your MPF savings, you would still have your employer on the hook for severance and long service payments.

It’s nonsense and always was. Employees are if anything more conservative than their employers and would have to choose from the same list of approved managers given by their employers.

But let’s leave all this aside. The crucial point here is that if we are now to eliminate this offset, then the sole argument vanishes for employers to decide the choice of fund manager.

Then the way is open for you to have your own choice of fund manager. Then we could have competition at last in this market and a real retirement service.

I hope it is what Carrie Lam means by “various measures to optimise”. I think it is the only one that really matters.