Germany may want to rein in its push for monetary tightening as its own economy shows signs of cooling

David Brown says Germany has been arguing for a tightening of monetary policy in the euro zone. However, with business indicators in the country dipping, the European Central Bank’s gradual approach may be warranted after all

German Chancellor Angela Merkel walks past electricity-powered vehicles at the booth of the German car manufacturer BMW during her visit to the Frankfurt Auto Show in September 2017. Recent indicators show that German manufacturing growth is slowing in 2018. Photo: AP

Germany embarked on its economic recovery long ago. Ramped up by a steady stream of super-stimulus, German expansion has surged and domestic employment soared in a self-reinforcing revival since the 2008 crash.

It is no wonder Europe’s monetary leaders face a judgment of Solomon between reining Germany in and pumping up recovery for Europe’s slower economies. Who would want to be in the European Central Bank’s shoes as decision day looms closer?

German leaders know full well they have had too much of a good thing in recent years. An overload of cheap and easy money and a relatively weak euro have raised the lid on inflation fears in recent years and the national mindset remains adamant about normalising ECB monetary policy as soon as possible. Inflation has always been the big bogeyman for German policymakers and they are not going to give in easily on putting their own domestic monetary priorities first.

Greek Prime Minister Alexis Tsipras (right) speaks during a roundtable discussion with French President Emmanuel Macron and business leaders in Athens in September2017. France's president has called for greater European investment in Greece to help offset the cash-strapped country's increasing reliance on non-European countries, notably China. Photo: AP

With German gross domestic product expanding at a 3 per cent annual rate, it provides a vital step-up for the rest of Europe. So the last thing Europe needs is any risk of a slowdown in economic activity or trade flows as a consequence of Germany throttling back.

Germany boasts the world’s second-largest trade surplus, is the third-largest exporting nation and enjoys extremely strong government finances. Germany is blessed with so much good fortune it has plenty of spare to share around.

The indicators raise questions over whether expectations for stronger recovery might have been exaggerated

But there may be trouble ahead that could turn the tide in the ECB’s favour for extending the stimulus longer than expected, against German demands to curb the monetary overkill as soon as possible. For the last few months, leading indicators have been pointing to Germany’s manufacturing powerhouse losing steam, possibly suggesting growth momentum could soon start to flounder.

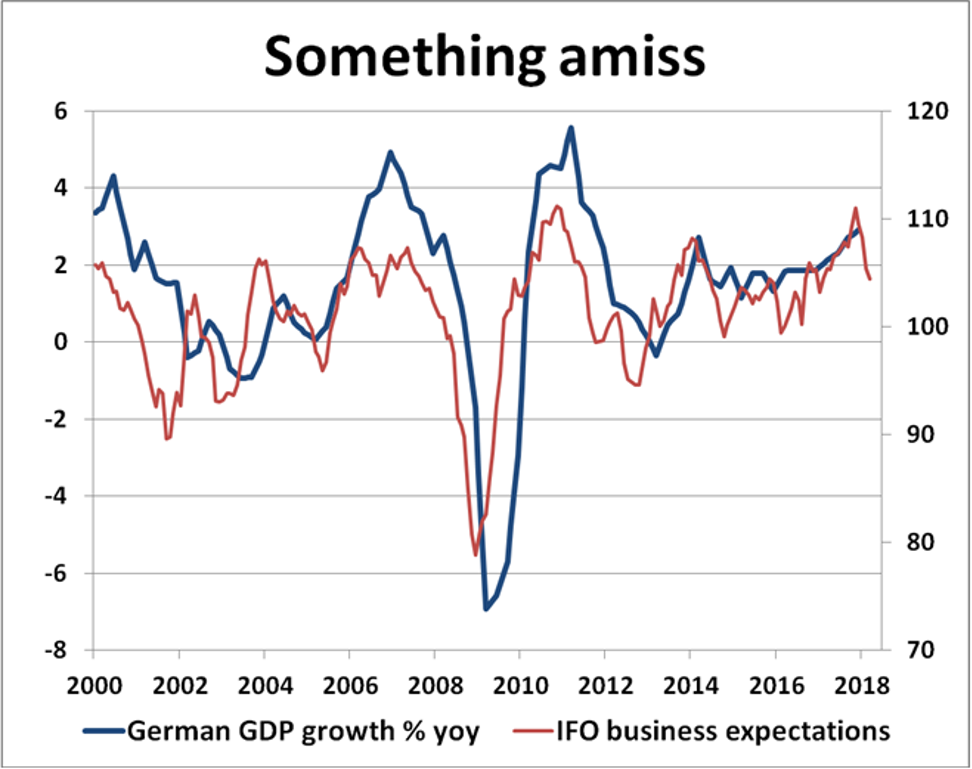

So far this year, a number of benchmark German business indicators have seemed in retreat. Important economic yardsticks such as Germany’s Ifo business climate index, the ZEW economic conditions indicator and purchasing managers’ reports have suggested economic demand might have hit a soft spot in the first quarter.

There may be no signs of a deeper rout just yet, but the indicators raise questions over whether expectations for stronger recovery might have been exaggerated.

The indicators not only raise the possibility of a consolidation in German economic activity, but also whether Europe and the global economy might be entering a cooler phase. After all, the driving force for Germany’s growth locomotive is the export sector and if German manufacturers see weaker trends emerging in the bigger picture, it means global recovery may be heading into a soggy patch too. It could spell bigger problems ahead for global equities.

If German manufacturers see weaker trends emerging, it means global recovery may be heading into a soggy patch too

Germany’s monetary policymakers will be scouring this week’s clutch of German business indicators for telltale signs of steeper slippage.

Recent Ifo surveys reveal crucial clues that business expectations for future export orders have ebbed away quite sharply in recent months. For all the bravado about Germany’s robust rebound, it suggests something is amiss and global export demand for German manufactured goods might have peaked and already begun tailing away.

Background risks in the global economy seem pretty formidable right now. German industry has every right to feel gloomier about the threat of an all-out trade war and the fallout from global monetary tightening as the US Federal Reserve ploughs ahead with higher rates while long-term borrowing costs drift up on the back of the continuing bond market sell-off.

European recovery risks and Brexit uncertainties still overshadow the outlook closer to home.

Anti-Brexit protesters demonstrate in front of the Houses of Parliament in London on April 16. Photo: Reuters

The domestic picture is not that great either, with the German car industry feeling the heat from the recent diesel emissions scandal and the dramatic drop in demand for diesel cars, given a considerable consumer backlash. Germany’s auto industry is heading into crisis, with new diesel car registrations in March plunging 25.4 per cent from a year earlier. It is turning into a worldwide problem that looks set to hurt global demand for German cars in a bigger way.

This is food for thought when the ECB meets this week to ponder the outlook for monetary policy and interest rates ahead. While Germany expects everyone else to dance to a tougher monetary tune, maybe it needs more honest German self-reflection for all Europe’s sake. ECB gradualism may be the best way forward after all.

David Brown is chief executive of New View Economics