Who might be hurt by fallout from the US-China trade war? Singapore, Taiwan, Malaysia, to name a few

Aidan Yao says a sizeable amount of Chinese exports consist of components made elsewhere, which means the trade dispute with the US will hit China’s partners in the global supply chain

Economists have generally put out solid work on the first aspect – involving the US and China – but good analysis on the contagion impact has been harder to find. Which could be the worst-hit countries, outside the US and China? What is the nature, scale and breadth of the spillover? And does everyone stand to lose?

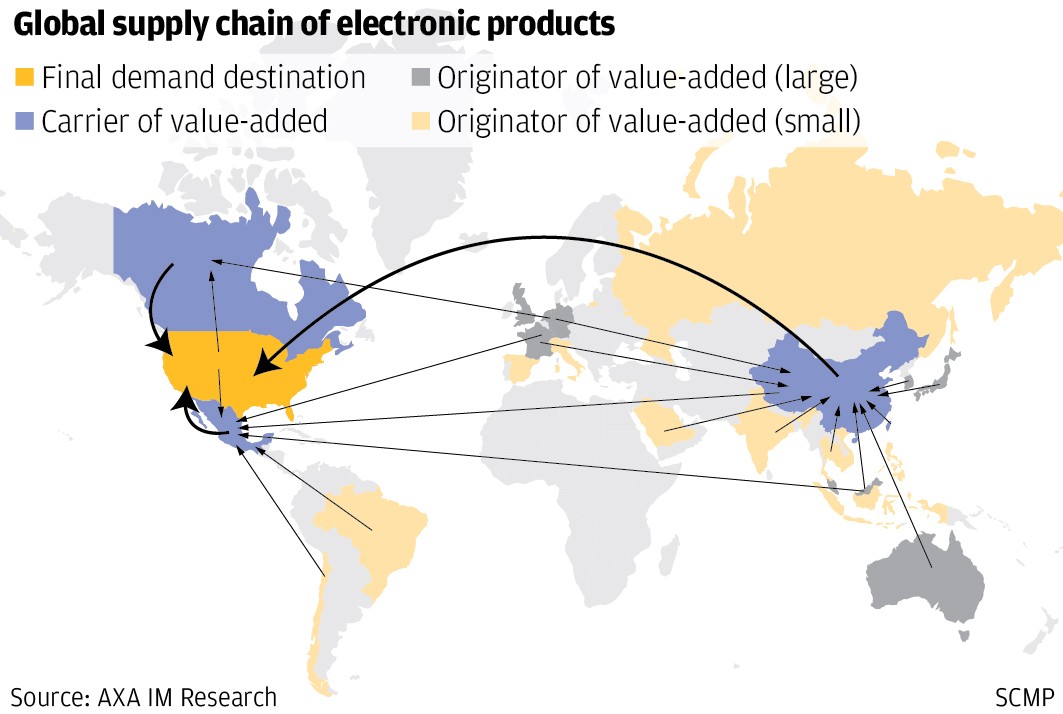

Let’s start by recognising China’s important position in the global supply chain, which is linked to the manufacturing of many products that have been, or will be, hit by the US tariffs. According to China’s customs, over 30 per cent of the country’s total exports in 2017 were processed and assembled products that incorporated other countries’ inputs and components. This means that even though the final goods were labelled “made in China”, the profits were not made by Chinese producers alone.