Advertisement

MacroscopeAsian equities could see a rebound in 2019 – if three cogs in the wheel fall into place

- Tai Hui says a weaker US dollar, resumption of dialogue between the US and China on trade, and more stimulus from the Chinese government could turn around the gloomy sentiment on Asian equities

3-MIN READ3-MIN

Following a spectacular 2017, expectations were high for Asian equities at the start of 2018. However, a combination of a strong US dollar and uncertainties from the trade war between the US and China have brought a disappointing year so far for them. The MSCI Asia ex-Japan index has declined by 15.9 per cent year-to-date, versus a 3.5 per cent gain for the S&P 500. What factors could turn this around as we approach 2019?

First, the US dollar will need to get weaker. While Asian currencies have suffered less, relative to other emerging markets like Turkey, Argentina and South Africa, higher interest rates in the US and US dollar strength are still sucking international capital out of our region. Even as the Federal Reserve is expected to continue to raise interest rates going into 2019, rising current account and fiscal deficits, the US dollar’s rich valuation and the Trump administration’s desire to improve US export competitiveness could all potentially push the greenback lower.

Second, the trade war between the US and China needs to stabilise, given the sensitivity of Asian corporate earnings to Asian export performance. It is difficult to expect Beijing and Washington to end their trade war any time soon, but a resumption of dialogue between the two to prevent further escalation should help reduce uncertainties for businesses and investors. The time up to the G20 Summit in Buenos Aires at the end of November could offer an opportunity for the two sides to work out their differences.

Advertisement

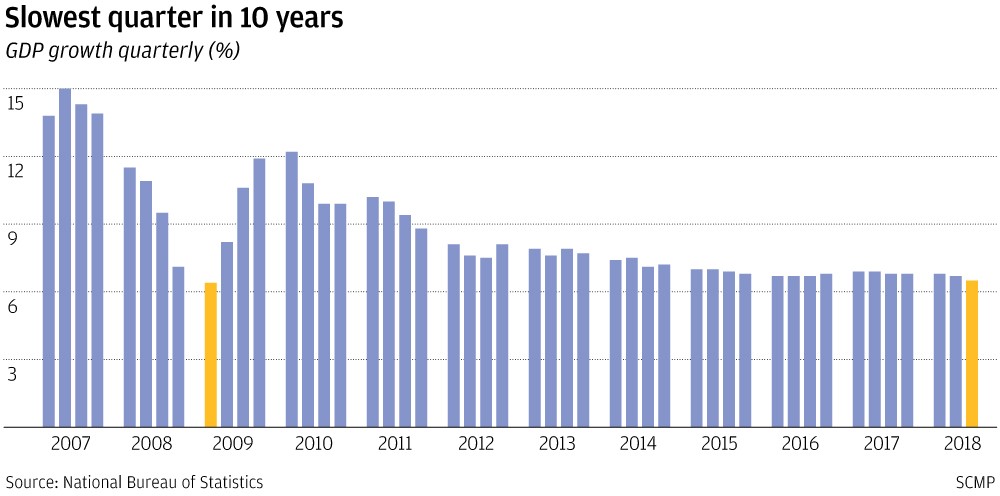

Third, China’s shift in policy priority from deleveraging to growth could also boost sentiment. China’s economic growth has softened in recent months due to the authorities’ efforts to reduce debt and manage financial-sector risks, as well as the rise in uncertainties from its trade relationship with the US. GDP growth in the third quarter fell to 6.5 per cent and the manufacturing Purchasing Managers’ Index fell to 50 in September, right on the watershed at which manufacturing could swing from growth to weakness. This indicator last fell below 50 in 2015, and Beijing then boosted government spending and cut interest rates to protect growth.

Advertisement

The People’s Bank of China has already announced a reduction of 100 basis points in the reserve requirement ratio for banks after the National Day holiday, and more easing could be on its way. Local governments are encouraged to kick-start any “shovel ready” infrastructure projects. Export rebates have been raised for almost 400 types of products to support businesses affected by the trade war. We could see further discussion of tax cuts to boost corporate earnings.

Advertisement

Select Voice

Select Speed

1.00x