MacroscopeUkraine crisis on top of Covid-19 pandemic is one shock too many for the global economy

- Covid-19, US-China decoupling and sanctions on Russia have dealt a collective blow to globalisation, most of all at the expense of developing economies

- Supranational agencies like the IMF and World Bank must fulfil their role not only in offering development assistance but also in preserving peace and stability

It is not just global confidence which has taken a hard knock, but also the perception that political, economic and financial stability will bounce back soon. The world may be on the verge of a new phase of potential market strife where output, trade and price stability will be less certain and subject to greater volatility. The key question is whether the global economy can withstand another shock so soon after the Covid-19 crisis.

On the positive side, if raw material prices stay strong, commodity producers and cartels like the Organisation of the Petroleum Exporting Countries will hold the whip hand again, with a return to 1980s-style oil surpluses being recycled back into global financial markets, providing continuing support for investor exuberance. Stagflation may dominate, but with global liquidity levels riding high, stock markets will still flourish, albeit in a much more volatile environment.

02:11

Oil prices skyrocket around the world as result of Russia-Ukraine conflict, sanctions

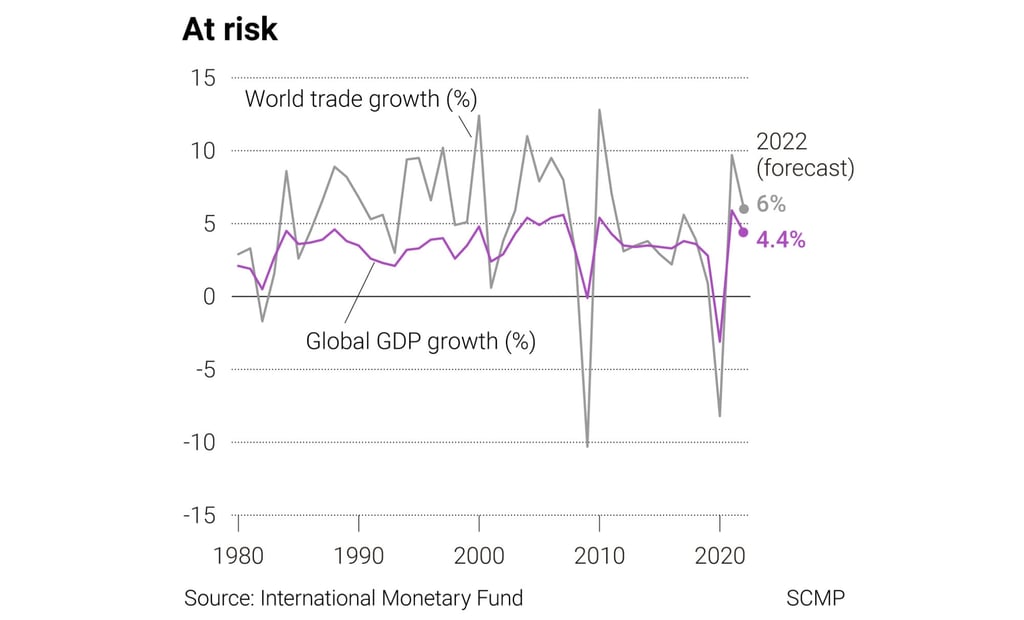

As the US-China trade war intensified, world trade growth in goods and services slowed dramatically from 3.9 per cent in 2018 to 0.9 per cent in 2019, before the Covid-19 crisis sparked an 8.2 per cent collapse in global trade flows in 2020. World trade growth subsequently recovered to 9.7 per cent last year, but the Ukraine crisis casts a dark shadow over the outlook for sustainable recovery over the next few years. It’s safe to say growth expectations will be severely downgraded this year as economic optimism fades.