World leaders attend a working session at the Group of 20 Summit in Bali, Indonesia, on November 15. Attendees wrestled with a wide range of topics during the summit, but the state of the global economy appears to have been overlooked. Photo: AP

Opinion

Macroscope

by Anthony Rowley

Macroscope

by Anthony Rowley

Global economy’s frightful state gives world leaders reason to bury their heads in the sand

The world’s leaders had so many topics demanding their attention at recent summits that the parlous state of the global economy was overshadowed

Summit attendees could be forgiven for keeping quiet given the likelihood of continued monetary tightening and a 2023 of contraction and recession

From the Olympian heights they scaled to attend recent summits, national leaders had a clear view of the state of the world. As a result, the United States and China raised their sights on nuclear conflict and climate change, but on the global economy leaders failed to see through gathering dark clouds.

This was unfortunate because rarely has the global economy faced such a barrage of daunting challenges as it does now. Primarily, the war on inflation can be won only at the expense of economic recession and corporate distress, and even then not before we come down the debt mountain.

There was so much to occupy the attention of leaders from advanced and emerging economies at the Group of 20 (G20), UN climate change, Asean, East Asia and other summits – the Ukraine conflict, global warming, food and energy crises and so on – that the state of the global economy and financial system was largely overshadowed.

It will not remain in the shade for long, however. Charles Dallara, who could be described as an elder statesman of international finance, and others have warned that underlying reality will force its way into the open with rising unemployment, falling asset values and financial system problems.

Dallara, a veteran US Treasury and International Monetary Fund (IMF) senior official who also headed the Institute of International Finance in Washington for many years, is one of a shrinking number of people with the individual and institutional memory to realise that fighting inflation is a drawn-out, painful process.

His analysis in this regard, given during a recent event I moderated at the Foreign Correspondents’ Club of Japan, is that US Federal Reserve chair Jerome Powell “cannot afford to take his foot off the brake” on inflation. This, he said, is “not something that markets want to hear”.

06:12

Soaring inflation, Ukraine and Myanmar top Asia summit agendas

Soaring inflation, Ukraine and Myanmar top Asia summit agendas

They clearly do not. What markets – overvalued equity markets in particular – do wish to hear is even the slightest hint that the Fed and other leading central banks are thinking of easing up on the brakes so that stock market investors can push on the accelerator again.

Dallara, who was around when former Fed chair Paul Volcker was battling US inflation in the early 1980s, recalled that the moment Volcker paused in his giant-killing fight, inflation roared back. He then had to brake harder and raise rates even more aggressively. Recession and debt crises ensued.

Inflation in the US and Europe is likewise “monumentally persistent today”, Dallara said. “Do not underestimate the durability of inflationary pressures given the damage that has been done to inflation expectations.” In other words, the inflation genie is out of the bottle and into wage psychology.

The implication is that, at least until recession spreads from Europe to the US and maybe to the global economy, the corporate sector will need to battle rising wage and other cost-push inflation along with rising interest rates and perhaps falling sales.

As economist Richard Katz suggests, this implies the end of myriad “zombie” firms that survive only by virtue of low interest rates. Or, as venture capitalist Par-Jorgen Parson of Northzone told CNBC, multibillion-dollar unicorn companies could collapse in “spectacular failures”.

Queues of shoppers make their way through the Wednesday Market past a clothing stall in Istanbul, Turkey on November 16. Turkey is contending with the worst cost-of-living crisis for decades, with food prices up 99 per cent and energy bills rising by another 20 per cent, all in a country where half the population has to survive on the minimum wage. Photo: Bloomberg

The economic and social distress all this could cause is not something that summit attendees appeared to have grasped fully, or at least were eager to discuss. It is an inevitable consequence of rapidly rising interest rates trying to counter rapidly rising inflation.

Things likely will have to get worse across the board before they get better, and 2023 is likely to be a year of global economic contraction rather than expansion. We can count out the possibility of monetary stimulus, and fiscal stimulus will be limited. It will be a “grin and bear it” year.

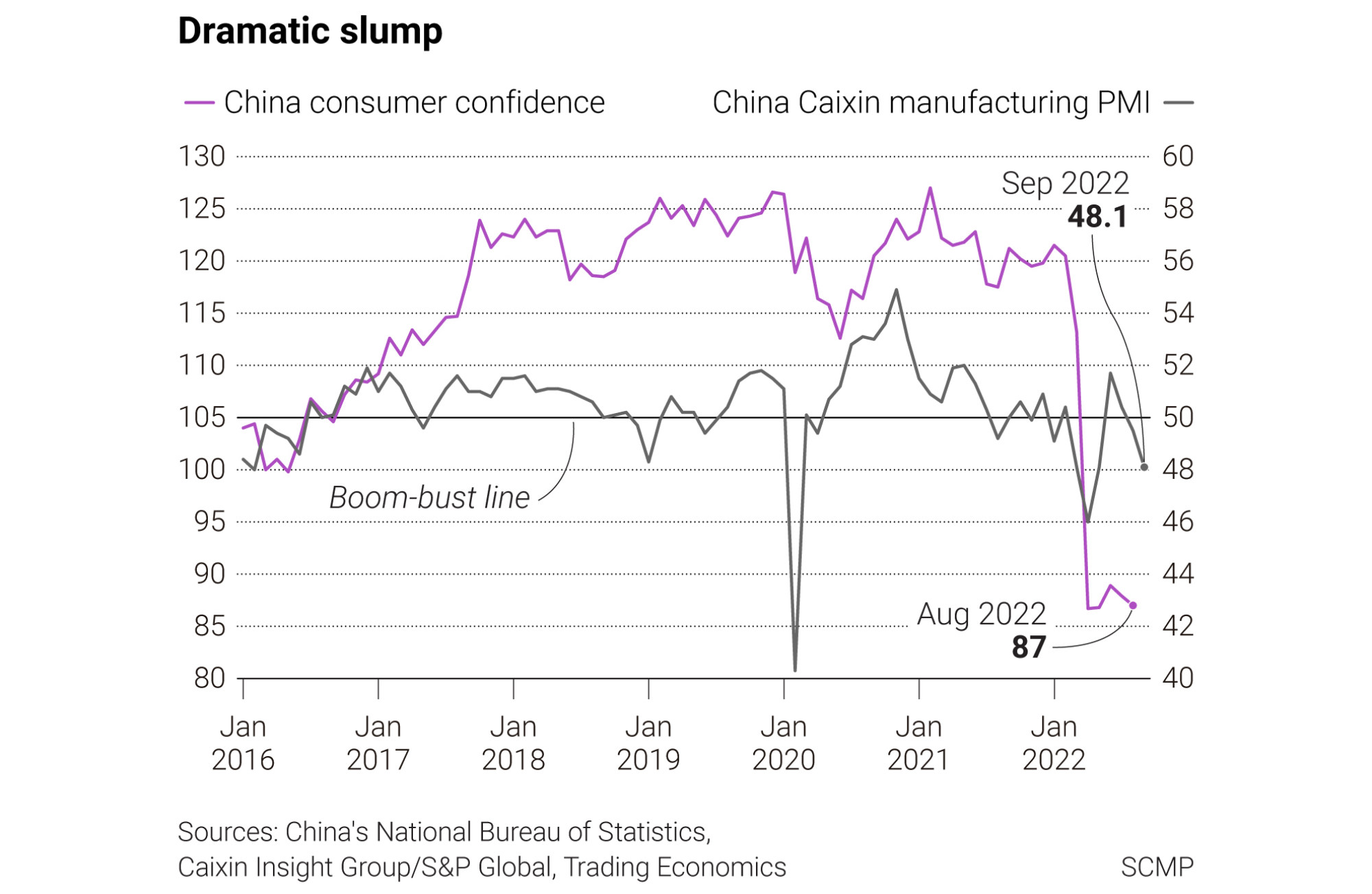

As the IMF noted in a report before the G20 summit, global economic growth prospects are confronting a unique mix of headwinds. These include Russia’s invasion of Ukraine, interest rate increases to contain inflation and lingering pandemic effects such as China’s lockdowns and supply chain disruptions.

There has been a steady worsening in recent months for purchasing managers’ indices in G20 economies. These gauge the momentum of manufacturing and services activity, and they are signalling contraction in both advanced and emerging economies, underscoring the slowdown’s global nature.

Yet, despite this, the message the IMF is sending out is that continued fiscal and monetary tightening is likely needed in many countries to bring down inflation and address debt vulnerabilities. “We do expect further tightening in many G20 economies in the months ahead,” it said in a blog post last week.

Perhaps the biggest unanswered question is when the debt crunch will really bite. Monetary policy, as economist Milton Friedman famously said, operates with a lagged effect. We certainly have not felt the full lash yet of interest rate increases and the more recent monetary tightening.

These can only have a nasty impact at a time of high global debt, and we will be lucky to avoid some kind of financial system crisis. Maybe summit leaders were wise after all to keep relatively quiet about such threats for fear of creating a financial panic.

Anthony Rowley is a veteran journalist specialising in Asian economic and financial affairs