Why the Fed should go easy on the world economy in 2023

- It is consumers who pay for the cost of the pandemic and the energy price spike. It is also consumers who drive economic growth

- With the world economy headed for tough times and US mortgage rates hitting a high, the Fed shouldn’t inflict higher rates and greater pain

The problem is that central banks have lost patience with inflation and the cupboard is bare in terms of what governments can afford to spend on reflation.

There are worries about job security too as companies seek cost savings, adding extra pressure as unemployment levels start to creep higher. The Organisation for Economic Co-operation and Development reports that the unemployment rate in the OECD area was stable at 4.9 per cent for September, slightly above its low point of 4.8 per cent recorded in July 2022, but the odds are that the jobless rate will rise a lot more as global headwinds intensify and business confidence dives.

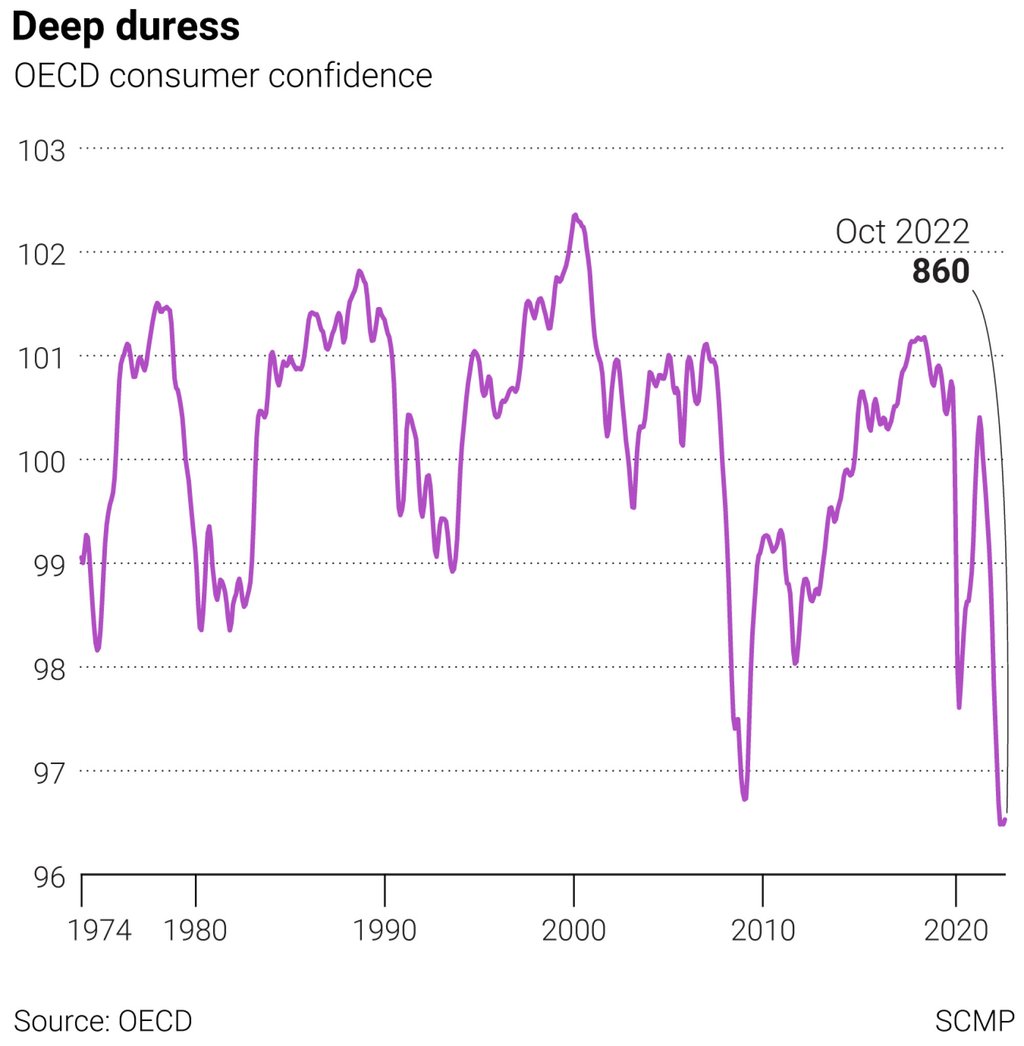

It’s no surprise to see consumer confidence levels showing signs of deep duress. For the 38 OECD member states, consumer optimism is close to an all-time low. It’s even weaker than the lowest points reached during the 2020 pandemic and after the 2008 crash.